The Evolution of Emerging Market Corporate Bonds for U.S. High-Grade Fixed-Income Investors

Key Points:

Emerging market (EM) investment-grade corporate bonds are an important and growing segment of the core fixed-income universe

These bonds have evolved to be more like U.S. investment-grade corporate bonds than high-yield or traditional emerging market debt (EMD) securities

This sector has demonstrated favorable risk, return, and diversification benefits in the context of a broad market fixed-income portfolio

Today’s fixed-income investors must have a framework for evaluating new opportunities subject to prudent risk management

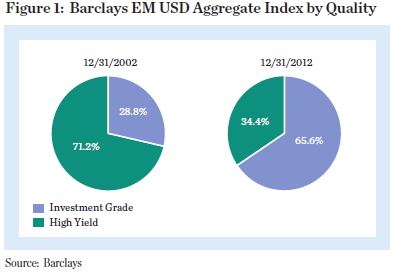

![]() Emerging market debt instruments have evolved rapidly over the past 15 years. In 1997, the Asian financial crisis sparked fears of global contagion, and in 1998 the Russian financial crisis and subsequent blowup of Long-Term Capital Management rattled the markets. In 2002,Argentina defaulted on its debt obligations. To a U.S. high-grade (USHG) fixed-income investor, these events further segmented the capital markets between developed and emerging markets. At the end of 2002, 71% of the EM universe was rated below investment grade.

Emerging market debt instruments have evolved rapidly over the past 15 years. In 1997, the Asian financial crisis sparked fears of global contagion, and in 1998 the Russian financial crisis and subsequent blowup of Long-Term Capital Management rattled the markets. In 2002,Argentina defaulted on its debt obligations. To a U.S. high-grade (USHG) fixed-income investor, these events further segmented the capital markets between developed and emerging markets. At the end of 2002, 71% of the EM universe was rated below investment grade.

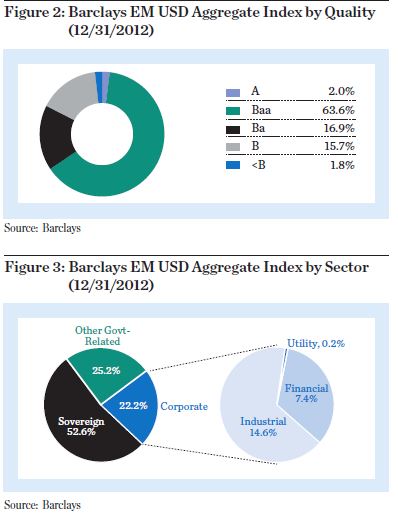

Since then, the improvement in the fundamentals of EM countries has been remarkable. At the end of 2012, only34% of the universe was rated below investment grade. As countries achieved investment-grade ratings, opportunities to invest in EMD credit instruments became more prevalent and corporations domiciled in those countries were able to issue bonds to a global investor base. In the early to mid-2000s, some quasi-sovereign and mega-capitalization companies issued U.S.-dollar-denominated bonds. EM corporate issuance continued to increase through the late 2000s and early 2010s, and a significant portion of the universe consisted of investment-grade credits. These issues were represented in U.S. investment-grade indexes such as the Barclays Credit Index and the Barclays Aggregate Index. Despite this increased integration into the U.S. investment-grade market, the segmentation of the developed and emerging markets remains, albeit to a lesser degree every day.

In this paper, we focus on investment-grade EM corporate bonds. We discuss the investment merits of this increasingly important asset class in the context of a U.S. broad market fixed-income portfolio. We also discuss an approach for implementing these opportunities into a broad market fixed-income portfolio.

Background

In the late 1990s, EM crises seemed commonplace. The Asian financial crisis hit the capital markets in July 1997and provoked fears of global contagion. Originating in Thailand, the crisis spread throughout most of the Southeast Asian financial markets. The following August, the Russian financial crisis hit the markets. As a result, the Russian government devalued the ruble and defaulted on its debt. The impact from the Russian default was felt in the United States, as it sparked the bailout of Long-Term Capital Management (LTCM), a hedge fund management firm founded by John W. Meriwether, the former vice chairman of Salomon Brothers. Fearing a systemic collapse of the U.S. capital markets, the Federal Reserve Bank of New York organized a $3.625 billion bailout of the hedge fund by a consortium of financial institutions.

In 2002, Argentina experienced a financial crisis and ultimately defaulted on its debt obligations. At the time,EMD bond spreads were persistently higher than those of U.S. high-yield bonds, as the recent past had weighed heavily on investors’ minds. If EM bonds were placed into a U.S. high-grade fixed-income portfolio, it was likely a limited amount of sovereign or quasi-sovereign bonds represented in the “plus” component of a core-plus assignment.

As the global capital markets improved from 2003 to 2006, many EM countries exercised the discipline to repair their fiscal and monetary finances. Countries such as Brazil,Mexico, Chile, and Colombia ultimately earned investment-grade ratings by the rating agencies. This resulted in representation in the credit component of popular U.S. investment-grade bond indexes, the most notable of which was the Barclays Aggregate. Inclusion in the broad indexes allowed them to become a larger part of high-grade fixed-income portfolios. The exhibit below illustrates the difference in the EMD landscape at the end of 2012 versus a decade prior. As shown in Figure 1, the EMD landscape is now 66%investment-grade, versus just 29% 10 years ago.

While all of this was happening to sovereign bonds, EM corporate securities followed a similar evolution in fixed-in-come portfolios. In the mid-2000s, most U.S. fixed-income investors bought exclusively U.S-domiciled credits in their corporate portfolio.

This changed somewhat as quasi-sovereign issuers such as United Mexican States, America Movil, Codelco, and others became more frequent USD bond issuers. In addition, large-capitalization companies such as BHP Billiton, Teva Pharmaceuticals, and Vale Overseas had high-quality ratings in the United States, so they were well-known to U.S. investors.

U.S. investors bought bonds from these companies as a means of adding incremental yield versus comparable U.S. issuers and to add a bit of diversification in their portfolios. Recognizing the liquidity benefits, more issuers registered their securities, increasing their availability beyond just the institutional market base. As these issuers became frequent issuers with clearly defined credit curves, these companies enjoyed access to the U.S. capital market. This access improved their cost of funding and added diversification benefits to their own risk-management process.

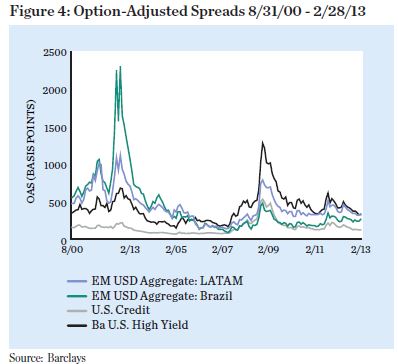

Valuation levels of EMD securities also evolved over the past decade. Risk premiums for these large-capitalization,quasi-sovereign issuers compressed to levels comparable to some U.S. issuers. Figure 4 shows the option-adjusted spread (OAS) of the Barclays Capital U.S. Credit Index, U.S. High Yield Ba Index, Barclays EM USD Aggregate: LATAM Index, and Barclays EM USD Aggregate: Brazil Index. Before 2006, the OAS (risk premium) is higher in LATAM and Brazil than it is for U.S. High Yield. In 2006, spreads compressed to levels between that of U.S. High Yield and U.S. Investment Grade Credit. With spreads in between U.S. High Yield and Investment Grade Credit, we believe that EMD still offers attractive return opportunities on a risk-adjusted basis.

Liquidity

As mentioned above, the EM countries that improved their fiscal finances happened to be domiciled mostly in Latin America, so the discussion turns to the dynamics of Latin America. Since the global financial crisis of 2008, Latin American companies focused on strengthening their balance sheets and issuing debt for asset-liability purposes (to increase their liability duration) while decreasing their overall indebtedness.

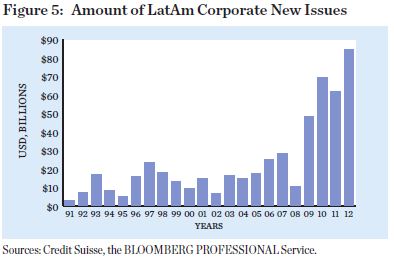

Increased supply of USD-denominated Latin American debt has been met with robust demand as U.S. investors such as pension funds, insurance companies, and mutual fund managers continued to see strong flows into fixed-income assets. Figure 5 shows the growth in annual issuance of USD-denominated Latin American debt.

Over the last three years (2010-2012), there has been consistent USD issuance in excess of $60 billion from companies domiciled in Brazil, Mexico, Colombia, Peru, and others. Before 2009, USD issuance by Latin American companies exceeded $20 billion just three times in 20 years (1997, 2006, and 2007).

The size and liquidity of the U.S. market are attractive to non-U.S. issuers. Most of the issuers favor long-maturity debt (for asset-liability management). Because of the recent experience with hyper-inflation, however, some of these countries (such as Brazil) do not have strong local demand for long-maturity debt, so the U.S. market has been a valuable alternative to debt-issuing companies. Issuing companies have largely accepted the cost of hedging the currency risk by issuing in USD, insulating USHG investors from this volatility.

By sector, issuance has been diversified; banks and finance- related companies, basic materials/commodity-related, and energy companies have led in volume. Demand for bonds has been fueled by total-return investors as well as yield-oriented investors. In addition, low yields across the global capital markets are increasing demand from Europe, the Middle East, and Asia.

Many companies in Latin America have adopted U.S. standards for accounting and reporting and in many cases have investor relations departments that are more fixed-income friendly than their U.S. counterparts. Many of these companies are privately owned so can only issue in the United States via SEC Rule 144A, which requires investors to be qualified institutional buyers (QIBs). Companies have tried to ensure liquidity in their bonds via larger deal sizes, through more open communication with investors, and by building relationships with more primary market dealers.

Over time, more EM companies have achieved investment-grade ratings (at least Baa3 by Moody’s and/or BBB- by S&P and/or Fitch). Issuing companies also now have a longer rating history with the nationally recognized ratings services. More-stable ratings and longer history help further broaden the investor base as more credits meet various investor screens. Increased USD issuance over the last few years has been met with increased demand by U.S. investors. While yields have compressed in all markets over this period, savvy investors have been able to stay in front of the bull market by adding new names and new markets to their portfolios.

Portfolio Implications

Thus far, we have demonstrated that the fundamentals, valuation, and technicals of EM investment-grade corporate bonds have evolved to the point that we consider this segment to be an important part of a U.S. high-grade investor’s opportunity set. We now turn to a framework for evaluating these bonds in the context of a high-quality fixed-income portfolio.

Risk and Return Characteristics

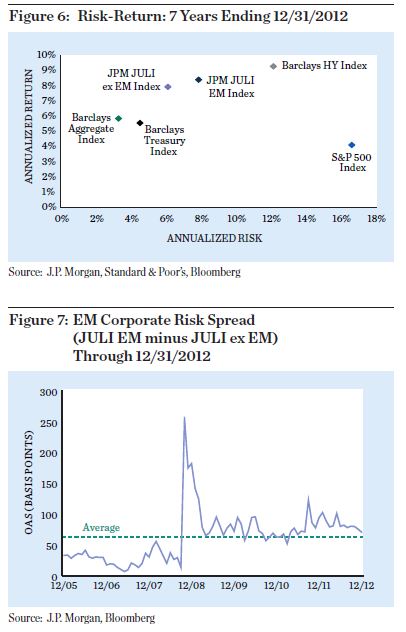

EM corporate bonds offer incremental yield over similar-quality, similar-duration domestic bonds. Historically, EM issuers have outperformed issuers in developed markets while exhibiting slightly higher volatility. The volatility exhibited has been more consistent with segments of the investment-grade market than that of the high-yield market, as Figure 6 shows. The EM corporate issuer index offered 71 basis points of yield over domestic corporate issuers, and that level is in line with the historical average (as of December 31, 2012).

We believe that the return enhancement opportunity will persist. We believe that some of the additional return offered by these bonds is compensation for investors’ biases. Investors remain biased against issuers in emerging markets, because of past crises that plagued EMD, home-country bias, or the costs of monitoring and surveillance. For example, many plan sponsors continue to have restrictions against investments in EM issuers (or even non-U.S. issuers), and that precludes a potential investor base from evaluating such investments.

Portfolio Diversification

Recent time periods capture a fascinating data set in which to assess the benefits of diversification. We have three distinct periods that should be of interest to any investor: pre-crisis (2006–2007), global financial crisis (2008–2009), and recovery (2010–2012). Using this data, we can measure the risk and return merits of this segment over a period that includes both remarkable volatility and a more stable state.

Our analysis shows us that this segment of the market offers important diversification benefits relative to three important segments of the investment-grade market: developed market corporate bonds, U.S. fixed-rate Treasuries, and U.S. TIPS. This is illustrated in Figure 8,and the highlighted points represent those with the highest Sharpe Ratio (return per unit of risk) on those efficient frontiers.

Credit Diversification

In the context of an all-corporate bond portfolio, our analysis shows that a 15% allocation to EM corporate bonds and 85% to developed market corporate bonds leads to improved risk/return characteristics. This allocation to EM bonds is slightly greater than most benchmarks’ weighting (typically closer to 10% EM).

Adding an allocation of 15% to TIPS to the 85/15 corporate bond portfolio further enhances the portfolio’s Sharpe Ratio. The diversification benefits are most pronounced with fixed-rate Treasuries; a 45% Treasury/55% corporate

portfolio provides the highest Sharpe Ratio.

We believe these securities offer another type of diversification benefit: EM companies are more likely to be privately owned or closely held (with little or no public float of shares). This requires investors to gain comfort incorporate governance issues and ownership structure in addition to the strength of management. We believe these characteristics offer investors built-in protection against excessive shareholder-friendly activities and, more specifically, LBO risk. This has become a meaningful benefit for EM investors as such activity has increased in the United States in recent months with Heinz, Dell, and others involved in transactions.

Lower Correlation to U.S. Interest Rates

With interest rates near historically low levels, investors are challenged to find novel approaches to investing in higher-quality fixed-income instruments that will also help protect against a rise in interest rates. Investment-grade EM corporate bonds may help provide some protection against the inevitable rise in interest rates.

Figure 9 shows the correlation that both developed and EM corporate issuers exhibited against the Barclays U.S. Treasury Index. The EM component of the index has consistently exhibited lower levels of correlation than developed market issuers, and that difference has increased significantly over the past few years. This suggests that investors who want to mitigate the effects of a rise in interest rates may be well served to consider an allocation to EM investment-grade corporate bonds.

William Blair’s Approach to EM Bonds

We believe that with a disciplined process and adequate resources, a skillful manager can add meaningful alpha even by investing in long-only, cash bonds. The active manager’s opportunity set should afford the manager flexibility to diversify into bonds issued by companies in various countries, consistent with their representation in indexes, for total-return and yield-oriented investors alike. Furthermore, issuance in USD has increased the opportunity set so that the U.S.-based investor can achieve incremental alpha without assuming currency risk as companies continue to tap the U.S. bond market

for funding.

EM corporate bonds require at least the same level of credit research and monitoring as their counterparts in developed markets. We believe there are opportunities in companies with globally oriented operations and sound management teams that can add attractive returns on a risk-adjusted basis.

In addition to the standard credit monitoring and surveillance employed in USHG bonds, we believe that personal meetings with management teams are important for credit investors to gain a full understanding of the teams’ goals and company strategy. We believe that active monitoring, disciplined risk controls, and an intermediate- to long-term time horizon are all important components to investing in this segment of the market.

We adhere to several risk controls in the management of our clients’ fixed-income portfolios. For EM corporate bonds, we employ two risk controls that we believe are critical for successfully integrating this segment of the market. First, we apply a more stringent position size limit for these bonds than we do for a domestic issuer. Our typical position size for a domestic issuer is 1.00%, and we employ a lower position size of 0.75% for an issuer domiciled in the emerging markets.

Second, we limit our total exposure to this segment to how it is represented in our strategies’ benchmarks. This has two implications. From the standpoint of the broad market indexes, EM issuers are a small but significant part of the Indexes. EM issues were 1.9% of the Barclays Aggregate Index and 2.0% of the Barclays Intermediate Government/Credit Index as of December 31, 2012. From a credit-only standpoint, EM issuers represent 10% of the credit Index, so a 2x overweight would equate to 20% of the portfolio’s total credit exposure. The by product of these two risk controls is that the exposure will be a meaningful part of the portfolio and is large enough to adequately diversify.

Conclusion

Investors would be wise to understand which strategies their fixed-income manager employs in an effort to enhance a portfolio’s yield and/or total return. Furthermore, prudent investors should understand the risks that the managers

are assuming with their underlying strategy. This is particularly important in times of low yields as investors look to supplement their traditional fixed-income portfolios with risk-taking strategies that may include increasing credit risk,the use of leverage, or the use of derivatives—which may implicitly add leverage to a portfolio.

Many pundits agree that we are in a period of “subnormal”expected returns across all major asset classes. The challenge for plan sponsors is to properly diversify their overall plan assets in a way that adequately protects from idiosyncratic risks while ensuring total return sufficient to meet the plan’s obligations. Plan sponsors have increased allocations to alternative asset classes, such as commodities, hedge funds, real estate, etc. This increased

reliance on less liquid alternative assets increases the need for fixed-income portfolios to provide liquidity, stability and income.

Even in a low-interest-rate environment, the prudent bond manager should be able to provide reasonable return while maintaining appropriate liquidity and risk controls. Plan sponsors should seek to ensure that their managers have adequate latitude to invest in such opportunities so long as it is done in a risk-controlled manner.

Lastly, EM corporate bonds are one of the newer segments of the U.S. high-grade market and continue to offer a value opportunity. There will certainly be other types of securities that offer value in the future—some may be new types of securities in the index, and some may not be. We believe that a successful

fixed-income manager must be prepared to constantly evaluate relative value opportunities and develop a framework for evaluating such opportunities as a segment of a broad market fixed-income portfolio.

Important Disclosure

This material is provided for general information purposes only and is not intended as investment advice or a recommendation to purchase or sell any security. Any discussion of particular topics is not meant to be comprehensive and may be subject to change. Any investment or strategy mentioned herein may not be suitable for every investor. Factual information has been taken from sources we believe to be reliable, but its accuracy, completeness or interpretation cannot be guaranteed. Information and opinions expressed are those of the presenter. Information is current as of the date appearing in this material only and subject to change without notice. Past performance is not

indicative of future results. For more information, please visit williamblair.com. Forward looking statements and outlook for investment returns are for illustrative purposes only and may not reflect actual results achieved.

© William Blair