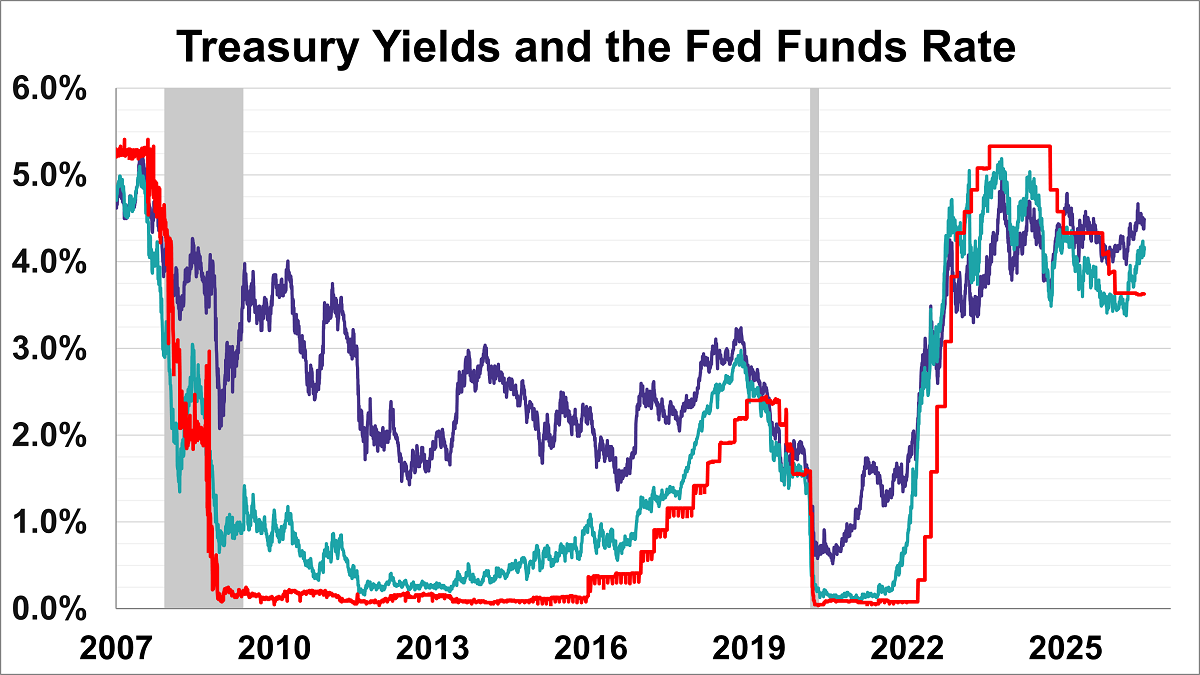

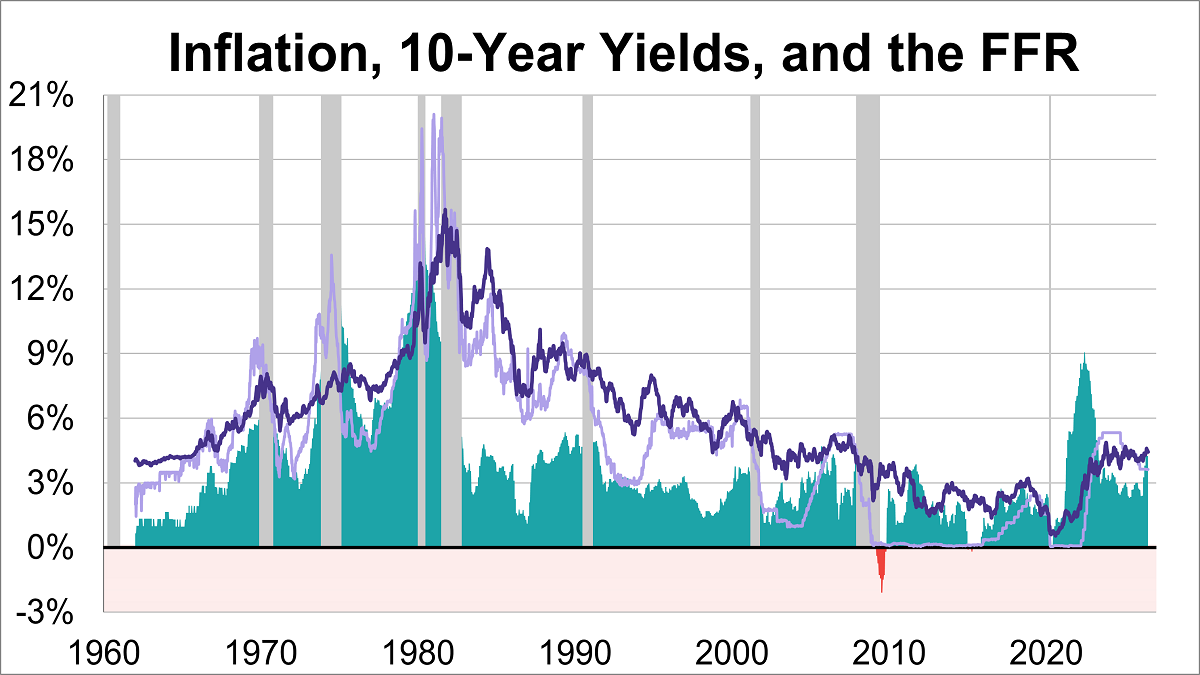

The yield on the 10-year note finished July 2, 2026 at 4.49% while the 2-year note ended at 4.14%.

The S&P 500 experienced its best week in two months, finishing up 1.7% from last Friday.

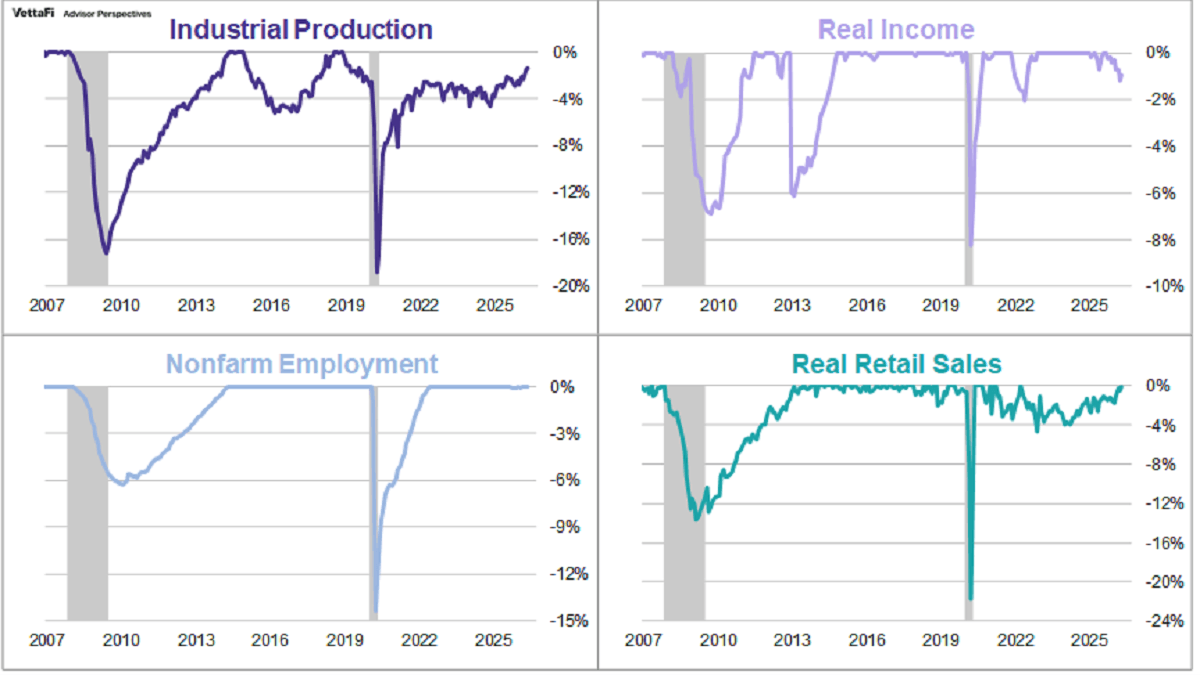

Official recession calls are the responsibility of the NBER Business Cycle Dating Committee, which is understandably vague about the specific indicators on which they base their decisions. There is, however, a general belief that there are four big indicators that the committee weighs heavily in their cycle identification process.

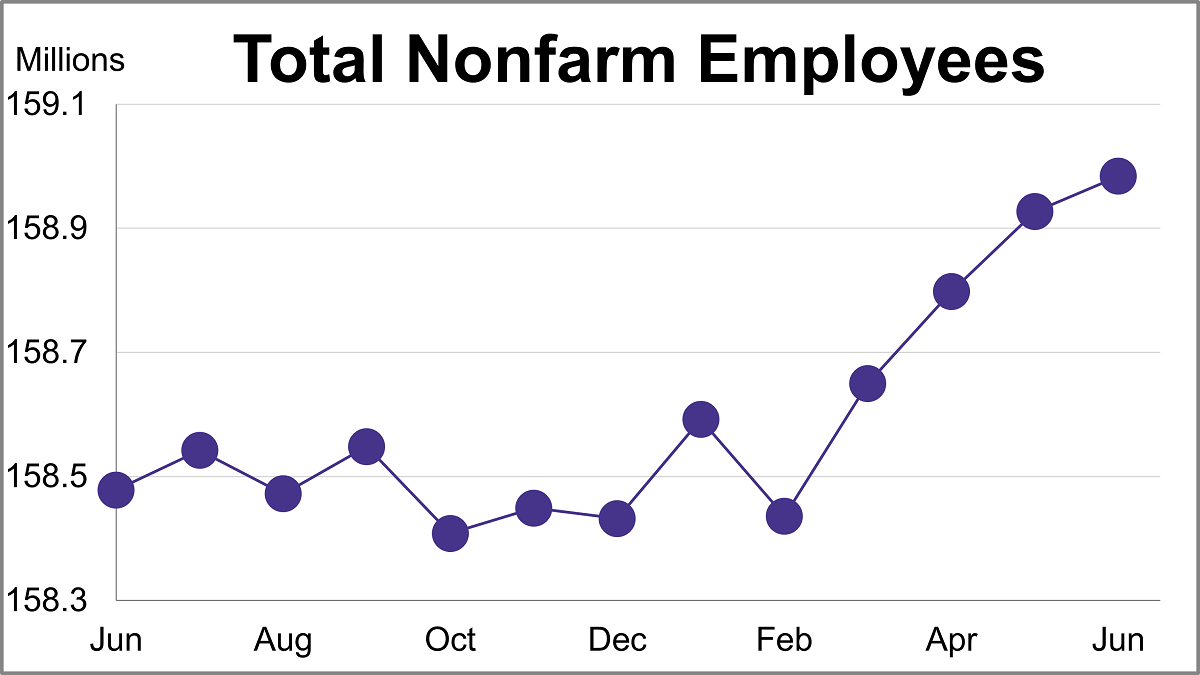

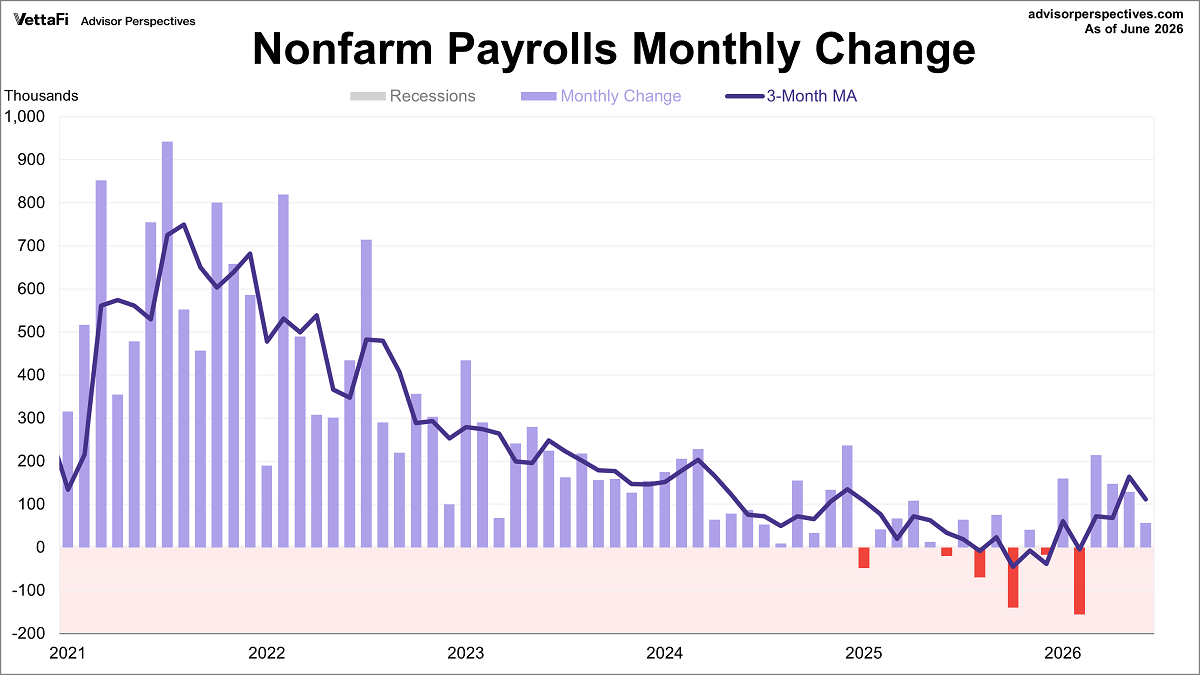

There is a general belief that there are four big indicators that the NBER Business Cycle Dating Committee weighs heavily in their cycle identification process. This commentary focuses on one of these indicators: nonfarm employment. In June, total nonfarm payrolls increased by 57,000 while the unemployment rate ticked down to 4.2%.

U.S.-listed ETFs locked in a record-breaking first half of the year. Read the analysis on active ETFs, fixed income shifts, and equity flows.

Former Fed Chair Alan Greenspan’s passing has brought a stream of retrospectives on his approaches to managing the economy. He erred on the side of parsimony, favoring short public statements. Greenspan’s vague communication style offered little clarity over the future path of interest rates.

The latest employment report showed that 57,000 jobs were added in June, down from May's 129,000 gain. This figure was significantly lower than the projected addition of 114,000 jobs. Meanwhile, the unemployment rate unexpectedly ticked down to 4.2%.

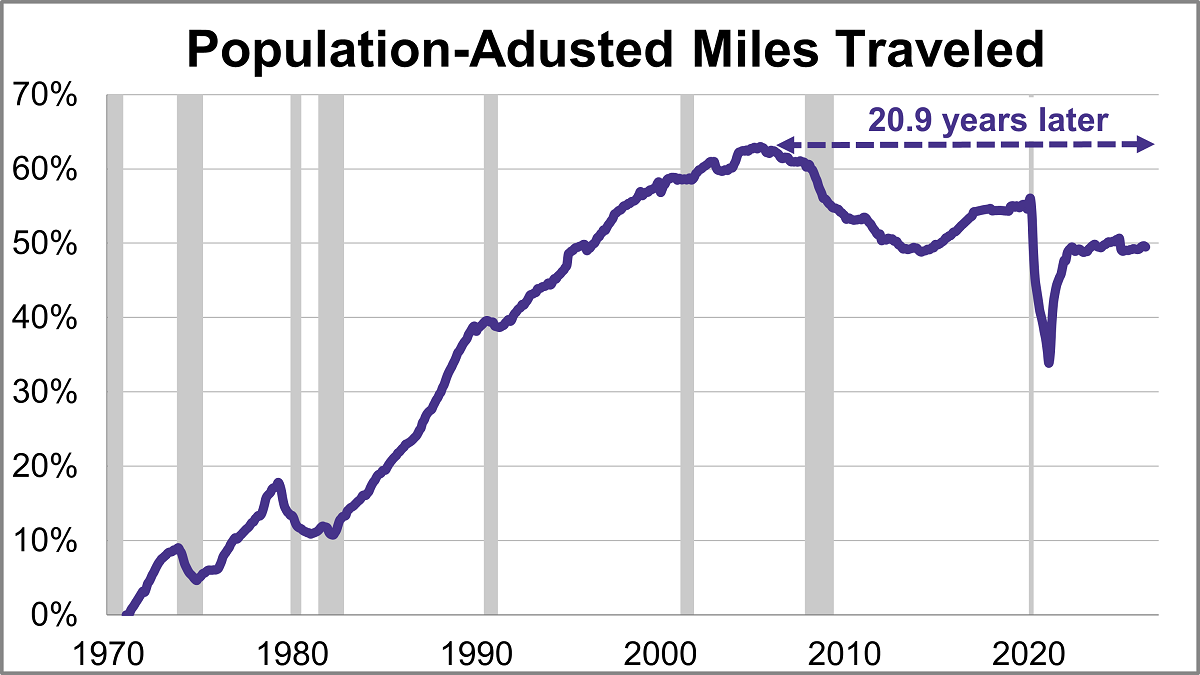

Travel on all roads and streets decreased in May. The 12-month moving average was down 0.06% month-over-month but was up 0.93% year-over-year. However, if we factor in population growth, the 12-month MA of the civilian population-adjusted data (age 16-and-over) was down 0.10% month-over-month and up 0.32% year-over-year.

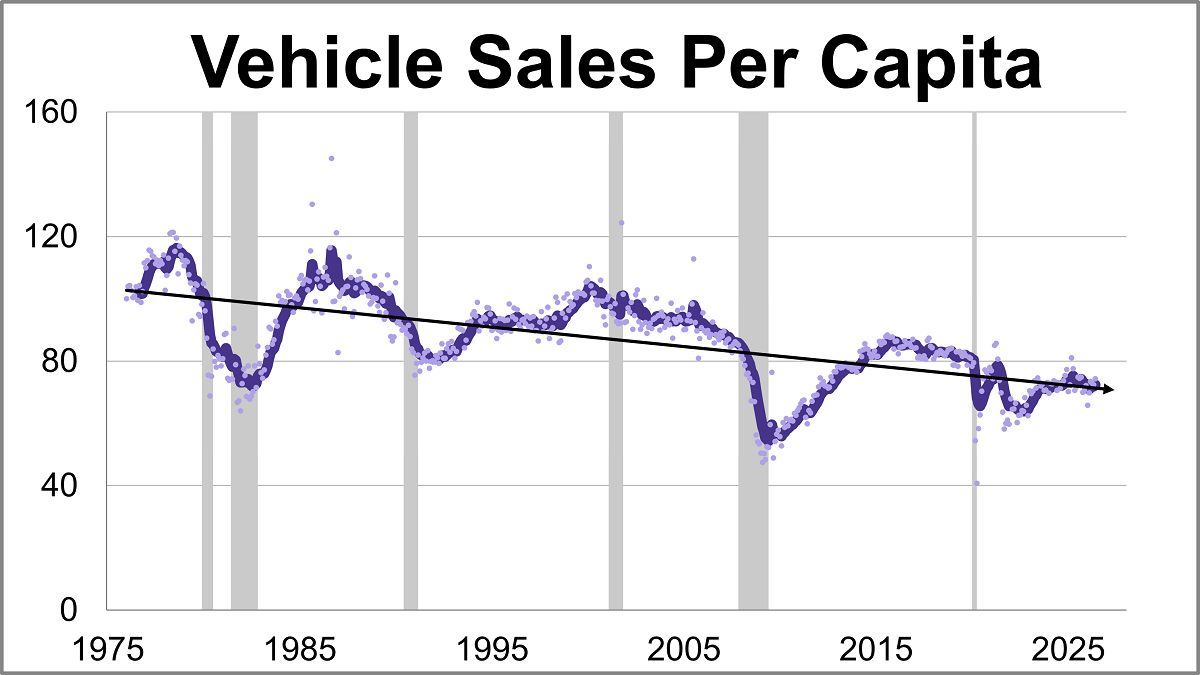

Vehicle sales rose to their highest level in nine months in June, coming in at a seasonally adjusted annual rate of 16.523 million units. This represents a 2.8% increase from the previous month and a 4.4% rise from one year ago.

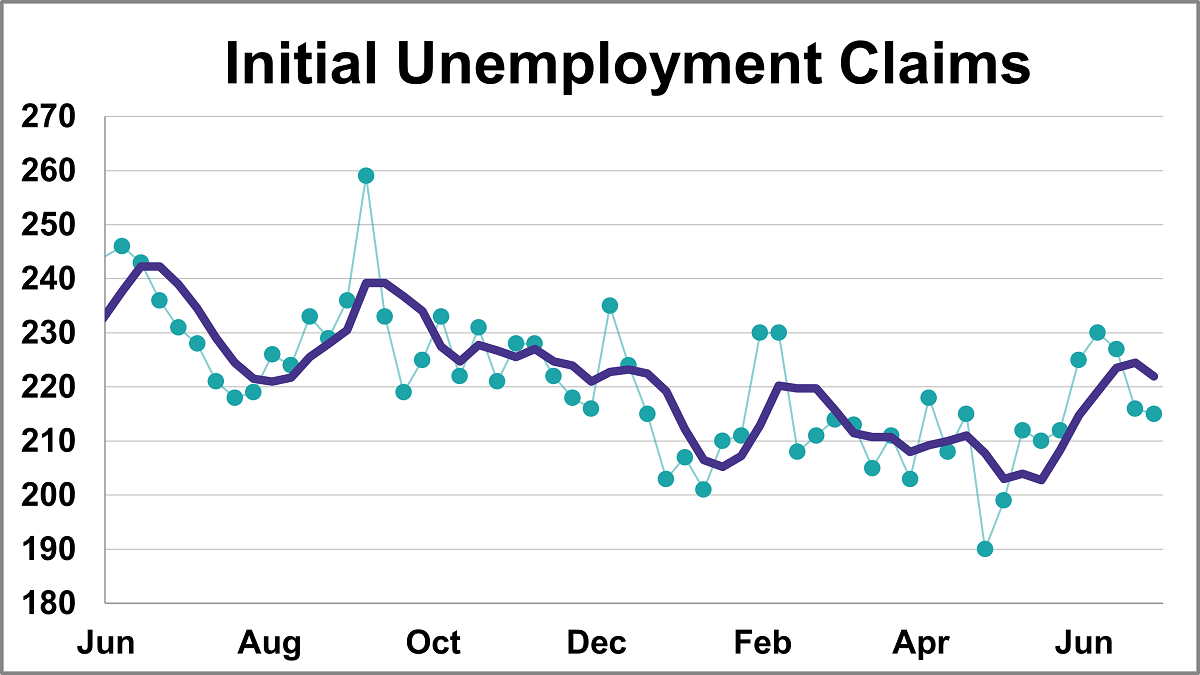

In the week ending June 27th, initial jobless claims were at a seasonally adjusted level of 215,000. This represents a decrease of 1,000 from the previous week's figure and was lower than the forecast of 219,000.

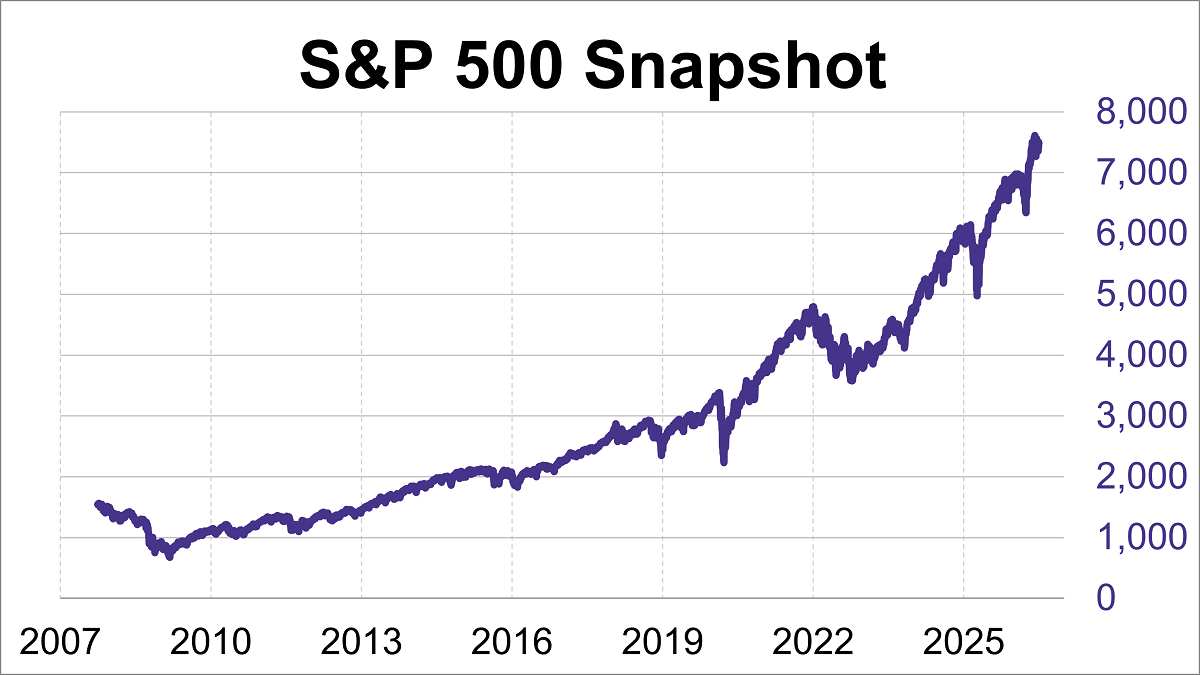

The second quarter wraps up today, and it was a good one. With the S&P 500 having returned more than 14% (including dividends) with just one trading day left, it will almost certainly end up being the best quarter for the index since the second quarter of 2020. Technology was the leader despite the June weakness.

The Mag 7 has been the single largest driver of the stock market’s performance three straight years, accounting for over 20% of the S&P 500’s performance. However, there is a performance divergence happening in 2026 as the S&P 500 continues to go up, while the Mag7 go down.

The artificial intelligence boom has a power problem, and Wall Street is betting billions on companies that promise to solve it — even if some of the technology hasn’t been fully developed yet.

A look at the resilient global economy, evolving market opportunities, and key risks shaping the investment outlook.

At first glance, allocating to emerging markets appears to add diversification to a portfolio. Look more closely, and the reality is more nuanced. In the late 1990s, the MSCI EM index was dominated by materials and telecoms, driven by the growth of mobile telephony and the internet bubble.

Markets weathered turmoil in the first half, helped by solid earnings with signs of broadening beyond a few AI beneficiaries. If the war in Iran eases, oil prices could normalize, reducing inflation pressure. Still, growth, inflation and policy risks may be underestimated.

The head of BlackRock Inc.’s beleaguered private credit fund is in the process of leaving the firm, a move that follows months of losses on soured loans and revelations of a US regulatory probe into the unit’s valuation practices.

Global stocks surged during the second quarter as oversold conditions in March and de-escalation in the Middle East created ripe conditions for a rally. In the United States, the large-cap S&P 500 index climbed by 13%, while the small-cap Russell 2000 index increased by nearly 25% (yCharts).

There’s no doubt the most important aspect to the June FOMC meeting was the fact that policymakers kept the Fed funds rate unchanged and removed its prior easing bias. But, this was not just your normal, run-of-the-mill policy gathering. It was Kevin Warsh’s first meeting as Fed Chair and instead of being a ‘rubber stamp’ for rate cuts, as some market observers were opining, the new FOMC leader put his stamp on the Fed in a different way.

The business of overseeing individually tailored municipal-bond portfolios has continued to grow rapidly, turning those money managers into the biggest holders of state and local government debt, according to JPMorgan Chase & Co.

June saw strong market fundamentals once again in conflict with macroeconomic uncertainties, creating a choppy market. While a durable peace plan with Iran is seemingly underway, investors have regarded the negotiations with caution, pricing in potential setbacks.

With the artificial intelligence race moving so rapidly, even a momentary lag can be costly. Alphabet Inc.’s Google is learning this the hard way: The search giant rapidly caught up with

Federal Reserve Chairman Kevin Warsh said price risks have come down in recent weeks, while repeating his determination to bring inflation back to the US central bank’s 2% target.

Markets may have ended the first quarter with a thud, but stocks put another record run in the books to close out the first half of 2026. The U.S. ETF market had already shattered records, crossing the $15 trillion threshold and cruising past $1 trillion in net inflows right before summer officially began.

It’s been a long time coming for the asset management world, but ETF share classes are now a reality. Fidelity Investments has joined that movement, with the launch of its first ETF share classes for some of its mutual funds.

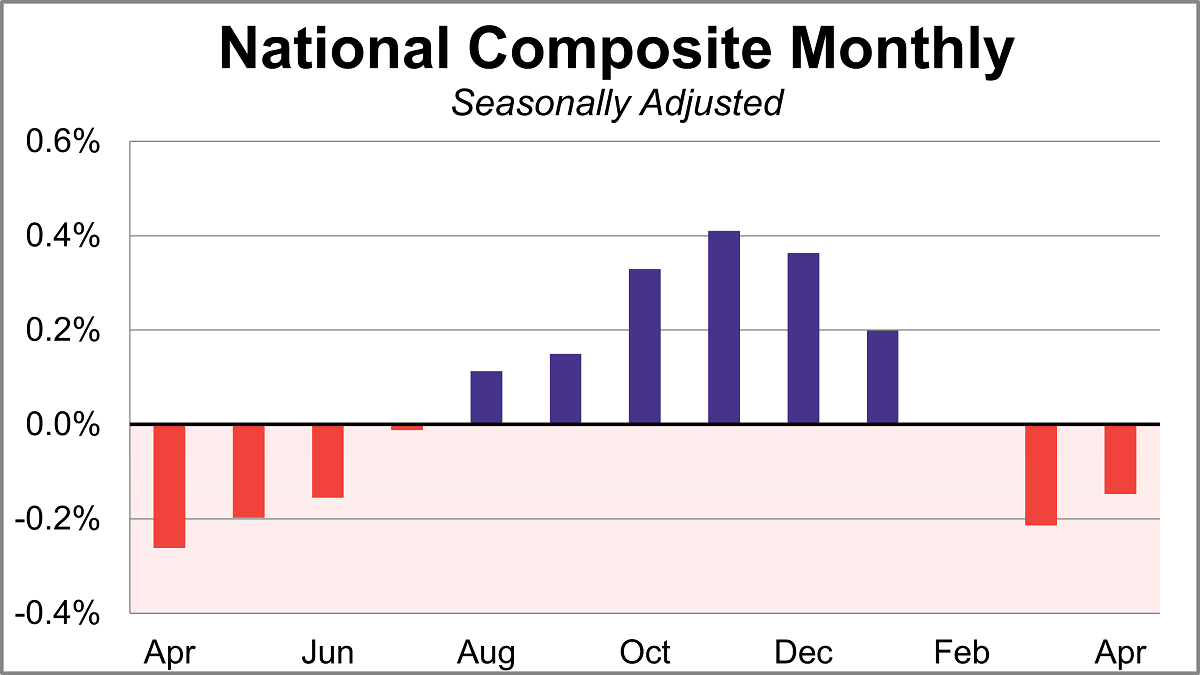

Home prices fell for a second straight month in April according to the S&P Cotality Case-Shiller index, as the housing slowdown intensifies. On a seasonally adjusted basis, the national index dropped 0.1% month-over-month and was up 0.8% year-over-year.

The 10-year Treasury yield has experienced dramatic fluctuations, ranging from a peak of 15.68% in October 1981, during the height of the Volcker era, to a historic low of 0.55% in August 2020, amidst the economic uncertainty of the pandemic. At the end of June 2026, the weekly average stood at 4.44%.

As growth stumbled, the S&P 500 Momentum Index captures a 7.5% gain in June and a 44% gain in the second quarter.

This debate also highlights a broader challenge facing markets today — balancing the desire for transparency with the need to encourage long-term thinking. Despite how often companies report results, investors will still need to discern short-term noise from long-term value.

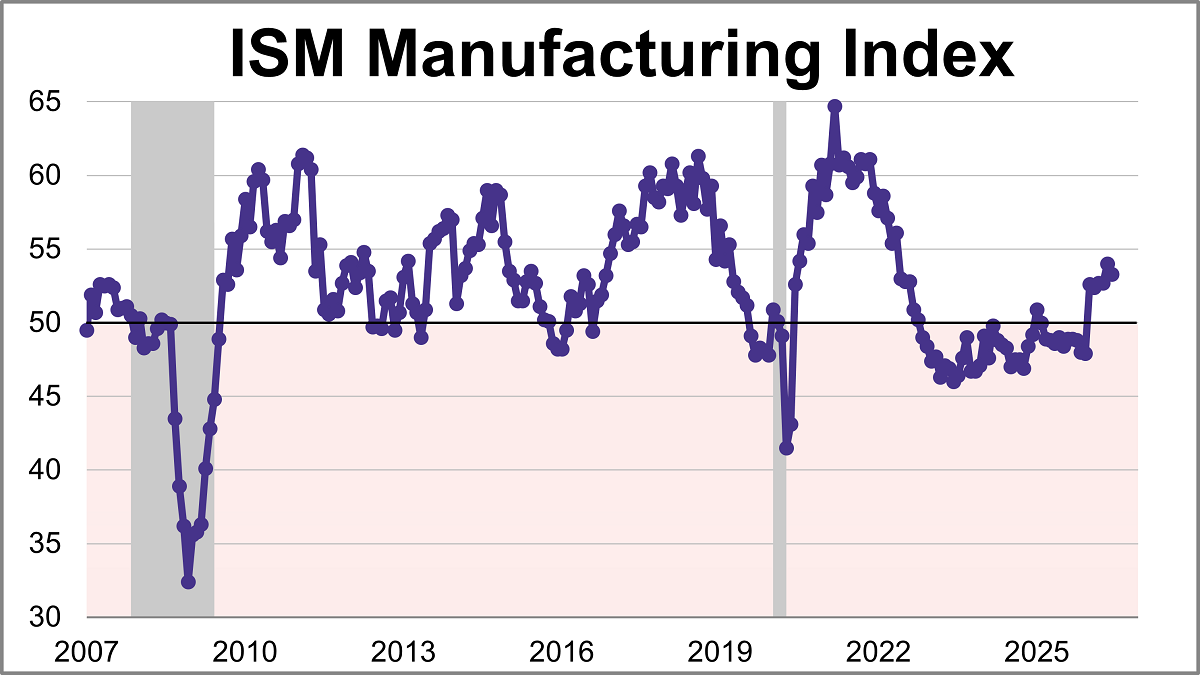

The Institute for Supply Management (ISM) manufacturing purchasing managers index (PMI) came in at 53.3 in June, down from 54.0 in May, marking slightly slower growth. The latest reading was just below the 53.8 forecast and is the index's sixth straight month in expansion territory.

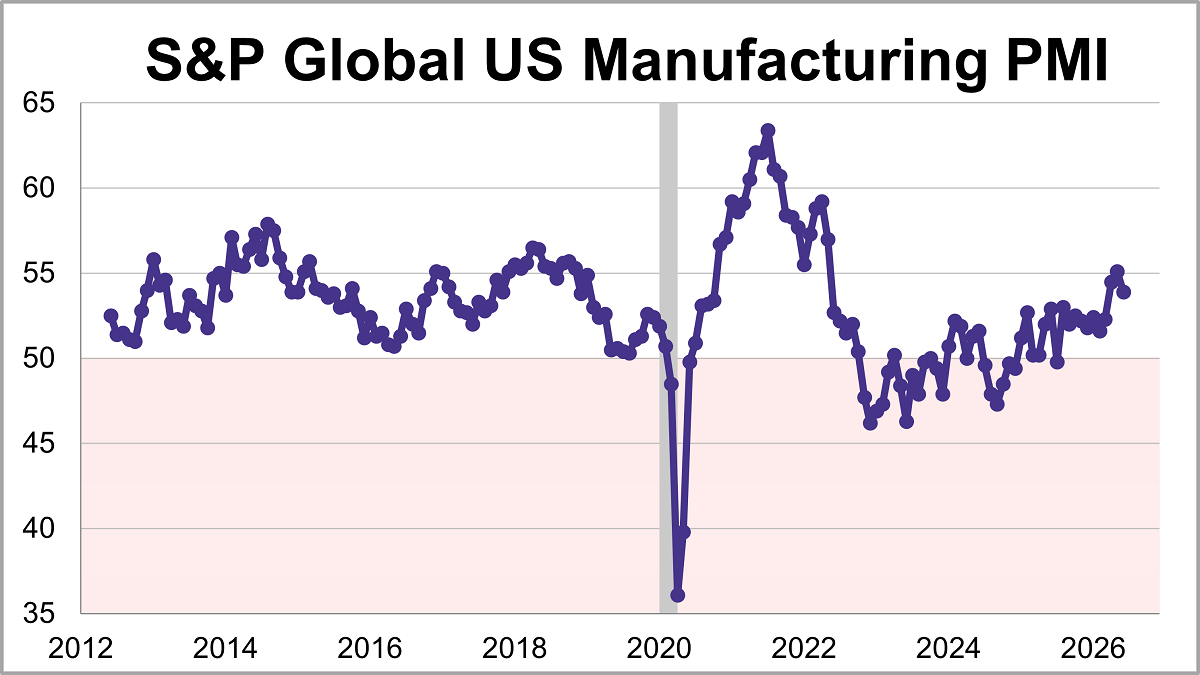

U.S. manufacturing expanded for an eleventh straight month in June but the growth eased to its lowest level in three months. The S&P Global PMI fell 1.2 points to 53.9 last month, falling short of the 55.7 forecast.

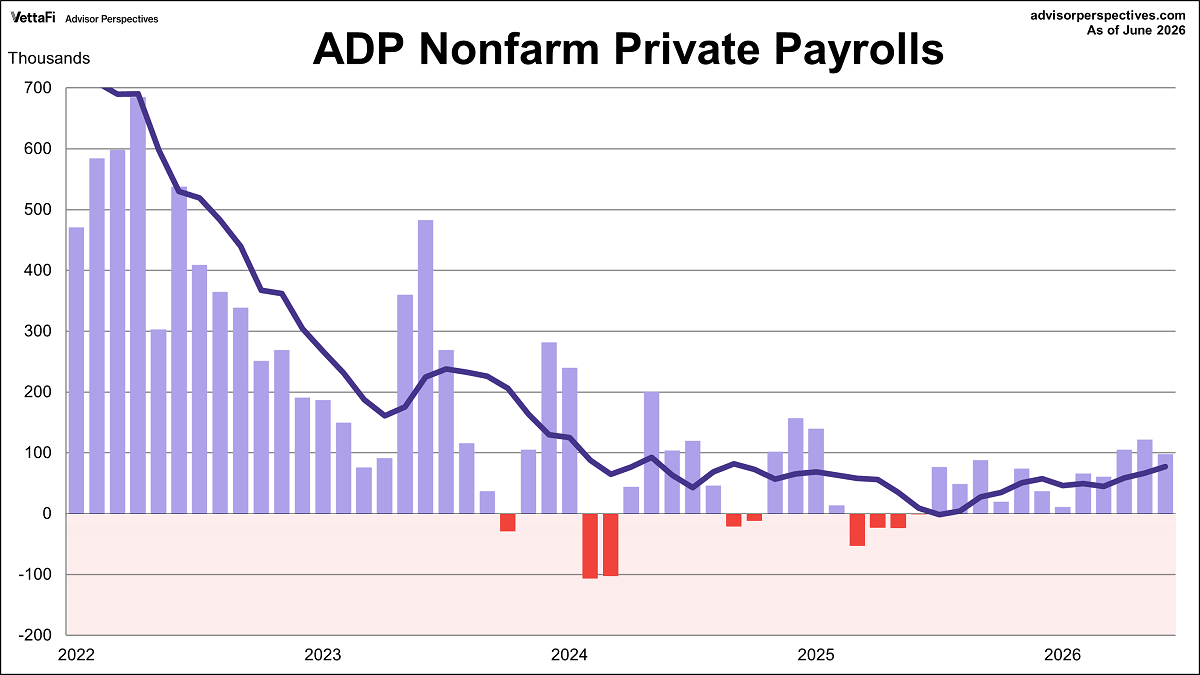

The ADP employment report revealed that 98,000 nonfarm private jobs were added in June, the twelfth straight month of growth. However, the latest figure was below the projected 118,000 addition.

The firms that operate rigorous vendor evaluation will compound two advantages simultaneously: They buy the right tools now, and their advisors trust them when the next generation of AI arrives. In a decade that will be defined by the industry's capacity to do more with fewer people, that trust is a strategic asset.

Acquiring a book of business is one of the fastest ways an independent advisor can grow AUM, expand a client base, and build long-term enterprise value. It is also one of the most financially consequential decisions you will ever make — and most advisors approach it underprepared.

A private bond market dating back more than a century is opening a new front in the trillion-dollar AI funding boom, allowing tech borrowers to sell debt directly to deep-pocketed insurance firms.

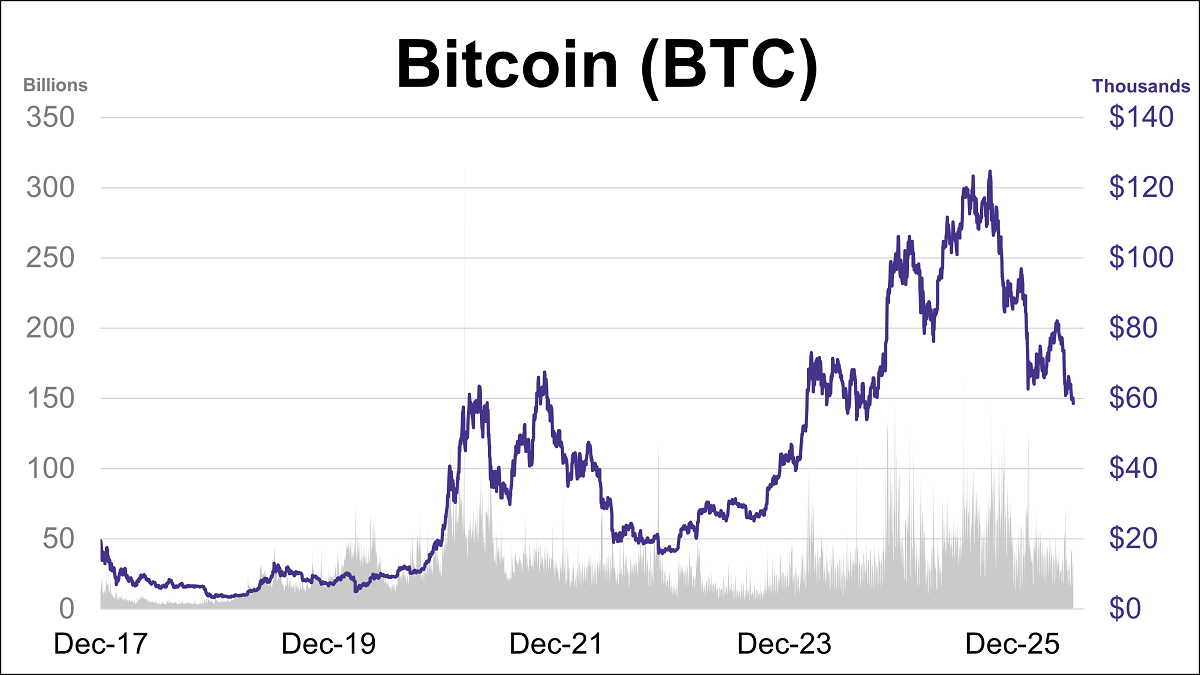

Bitcoin's struggles continued this week as it reached its lowest level since September 2024. BTC is currently down approximately 33% midway through the year and sits about 53% below its October 2025 record high.

July is a great time to buy stocks. In fact, it’s been the best month for the S&P 500 Index in the past two decades. Bulls are finding comfort in that history ahead of what stands to be an eventful stretch.

At the start of the regional war in February, Wall Street banks were grappling with the prospect of a protracted slowdown in the Middle East. Three months in, many firms are rushing to add bankers after local investors largely looked past the conflict and doubled down on dealmaking.

Meta Platforms Inc. is developing plans for a cloud infrastructure business that will sell access to AI computing power and models, setting up a new vector of competition with industry leaders like Amazon Web Services, Microsoft Azure and Google Cloud.

If your heart and mind tell you to go looking for someone older because that’s going to fit your culture more effectively, by all means search in that direction. Just don’t give up on younger, next-generation team members without making sure you have given them every opportunity to succeed.

While the Middle East is still far from calm, it does appear the worst of the volatility in the region is in the past. The U.S.-Iran ceasefire is in place, with negotiations underway for a more durable peace.

A strong quarter across major indexes. The second quarter is winding down and what a quarter it has been with the S&P 500 up 12.6% quarter to date, while the Nasdaq-100 and Russell 2000 are both up over 20%. Despite some twists and turns, the path of least resistance for stocks broadly remained up and to the right for much of the last three months.

Startup equity decisions often happen before a founder has a full advisory team in place. Formation documents get signed, vesting schedules are approved, and the tax consequences may not feel urgent because the company is still young.

In our view, this divergence continues to reflect how the buildout of artificial intelligence (AI) is influencing both the economy and markets as it progresses across the value chain, even as the associated costs continue to climb.

The sharp retreat in oil prices has dramatically altered the market narrative. Just weeks ago, investors feared a renewed inflation shock from the conflict with Iran. Instead, crude has fallen back toward pre-conflict levels, Treasury yields have declined, and markets have begun rotating aggressively away from the large tech hyperscaler, the Magnificent Seven, that dominated recently and toward more cyclical and value-oriented sectors.

Benchmarks are broken. That was the premise established in a conversation with Samarth Sanghavi, head of fixed income index product at TMX VettaFi, when the problem was first addressed in a previous article. TMX VettaFi creates innovative index solutions, and with the premise established that benchmarks are indeed broken, here is the fix.

Geopolitics, artificial intelligence, and inflation each took their turn commanding market attention last week. U.S. equities were mixed, as a pullback in technology names masked broadening performance beneath the surface.

The US Securities and Exchange Commission is signaling a potential rethink of how it oversees exchange-traded funds after a recent wave of filings for prediction-market ETFs prompted fresh scrutiny of the existing regulatory framework.

Insurance investors face a broader opportunity set than ever across public and private credit—from corporate lending to asset-based finance. But those investments come in many forms. In our view, a all-encompassing approach can better assess relative value, pivot to new avenues and align investments with portfolio, liability and regulatory considerations.

For decades, financial advisors have built strong relationships by helping clients manage IRAs, taxable accounts, and rollover assets after they leave an employer. Meanwhile, a significant, often the largest pool, of client wealth has quietly remained out of reach: assets inside workplace retirement plans.