- The unemployment rate may not be a reliable indicator of output slack in the U.S. economy.

- We’ll know (with a lag) if the economy has reached the end of the cyclical downturn when inflation picks up.

- The Fed will have to choose between risking a hawkish mistake or being behind the curve, waiting to see inflation actually increase. We expect it will choose the latter.

In order to fulfill its dual mandate of price stability and full employment, the Federal Reserve has been guided by the Taylor rule since the 1990s. The Taylor rule goes something like this: The appropriate short-term interest rate (set by the central bank) is a function of the slack in the labor market and the difference between actual inflation and the inflation target. Until the Great Recession of 2008, the unemployment rate was a good enough indicator of the labor slack. Hence, the Fed could set interest rates simply based on core inflation and the unemployment rate. Thanks to this framework, the Fed managed to be successful on the employment front but even more so on the price stability front.

But the situation has changed recently. On one hand, inflation was painfully low in 2013, and on the other, the unemployment rate has dropped sharply. Which part of the dual mandate should the Fed favor?

Gordon versus Yellen

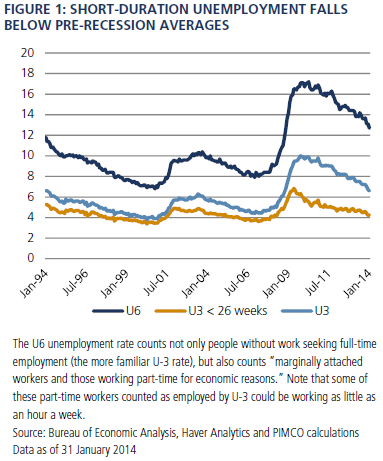

Some observers are arguing that the drop in the unemployment rate should result in earlier rate hikes. Writers of a few Fed blogs are citing a recent study from Robert Gordon of Northwestern University. They claim that short-duration unemployment (less than 26 weeks) is the best indicator of labor slack, and that since it has already fallen below pre-recession averages (Figure 1), the economy is at risk of overheating.

Meanwhile, in her testimony to U.S. Congress, freshly appointed Fed Chair Janet Yellen went in the opposite direction, saying there was probably more slack in the economy than what a naïve look at the unemployment rate would indicate: “Those out of a job for more than six months continue to make up an unusually large fraction of the unemployed, and the number of people who are working part time but would prefer a full-time job remains very high. These observations underscore the importance of considering more than the unemployment rate when evaluating the condition of the U.S. labor market.”

Both sides have a legitimate point of view, but “Gordon versus Yellen” is a bit like “Ali versus Frazier.” They’re both seasoned heavyweights. That the two can have such a stark difference of opinion about the unemployment rate underscores its questionable nature as an indicator. Most likely Yellen will have the last word, but she might also have her own agenda. Would she really be concerned by a bit too much inflation due to a tighter labor market?

Based on PIMCO’s bottom-up analysis, our outlook for 2014 inflation has core personal consumption expenditures (PCE) moving up to 1.6% year-over-year at the end of 2014, compared with the current 1.2% rate. Longer term, it really depends on what the Fed does.

The Fed’s choice

Since the unemployment rate may or may not be the right measure of output slack, it is not a reliable indicator for conducting monetary policy. We’ll know (with a lag) if the economy has reached the end of the cyclical downturn when inflation picks up. Hence the Fed will have to choose between being behind the curve, waiting to see inflation actually pick up, and risking a hawkish mistake. The last time it chose to ignore weak inflation prints and started to discuss monetary policy tightening, Mihir Worah and I warned that the Fed would end up doing more quantitative easing to compensate for its hawkish mistake (Viewpoint, “Promise to Be Irresponsible,” June 2013). That same month, Chairman Bernanke announced that when “asset purchases ultimately come to an end, the unemployment rate would likely be in the vicinity of 7 percent.” Now, the Fed is still expanding its balance sheet while the unemployment rate is well below 7%.

PIMCO expects that, balancing the risks between a hawkish mistake and some inflation overshoot, Yellen will choose the latter, especially since inflation has undershot the Fed’s mandate by so much in recent years. Since 2009, inflation as measured by PCE has averaged 1.4%. Given a medium-term inflation target of 2.0%, inflation could average 2.6% for the next five years to catch up. Basically, we believe Yellen could wait for core PCE to move back to a solid 2% before she hikes the rate. Since the unemployment rate is an unreliable measure, we believe inflation should guide monetary policy. But it’s up to the inflation jury to decide.

In the meantime, investors can position their portfolios to benefit from this monetary policy framework. Shorter duration assets should be “safer” than longer duration assets because they benefit from the low-for-longer policy rate stance, while longer duration will likely suffer from inflation uncertainties. We expect that strategies seeking carry from curve steepeners will perform well. The inflation premium should rise and, importantly, inflation uncertainties mean real assets should be less volatile than nominal ones.

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed.

This material contains the opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world.

© 2014, PIMCO.

© PIMCO