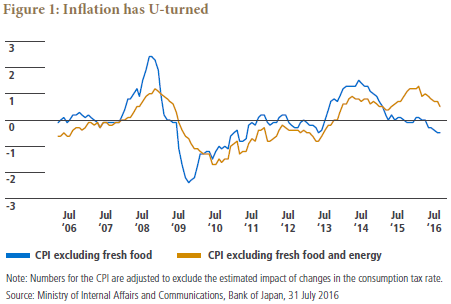

Another fundamental challenge for the BOJ is very low – or persistently negative – “neutral rates,” meaning the real equilibrium rates that are neither expansionary nor contractionary for the economy. In 2014, PIMCO developed a secular thesis we call The New Neutral. We have argued that neutral rates should be substantially lower in this post-Lehman-crisis economy than in the past, and that central banks should remain substantially accommodative and be rather patient in any policy normalization. The New Neutral was in fact “new” for most countries, but not for Japan: The country’s neutral rates were depressed even before the global financial crisis, due to its own secular dynamics, such as a rapid decline in productive ages of the population. According to the Japan Center for Economic Research, for instance, neutral rates have been negative in Japan since 1997. Worse, neutral rates will likely remain depressed in Japan unless they receive a significant lift from some positive shock, given the country’s ongoing demographic deterioration.

What do unanchored inflation expectations and low (and negative) neutral rates mean to the BOJ in fulfilling its price stability mandate?

The war against deflation will be a long one, most likely lasting beyond the end of Kuroda's term in April 2018. The BOJ needs to prepare for this. The bank will have to remain significantly accommodative for at least several years and patiently hope that supply-side improvements led by either the public or private sector (or a combination of both) spur a substantial rise in neutral rates some day in the future. Future external inflationary shocks, such as higher oil prices, may assist the BOJ in reanchoring inflation expectations while the bank remains in the game of monetary accommodation.

Hitting the limit

The question then becomes: Can the BOJ continue to do what it’s doing now, or even do more, within its current framework? The BOJ has said that it can, and in all three dimensions – quantity (JGB purchase amount), quality (types of risk assets to purchase) and negative rates. We don’t think so. In our view, the central bank appears to have hit its limit (or at least is approaching it) and therefore needs to make some adjustments to its policy toolkit to ensure its longevity.

First, there is a practical limit to how much more JGB debt the BOJ can buy. At the current ¥80 trillion pace of net increases per year, the central bank will own 48% of the JGBs outstanding a year from now. One could argue that this leaves 52% of the JGBs outstanding available for the BOJ to purchase. But this argument misses a key point. Banks need to hold some JGBs for collateral purposes, and life insurers also need to own long-dated JGBs (with 30-year maturities or longer) to reduce duration mismatches versus their liabilities. Considering these financial institutions’ needs for domestic “safe assets,” an International Monetary Fund (IMF) staff report in August 2015, for instance, estimated that the BOJ would hit its JGB purchase limit “sometime in 2017 or 2018.”

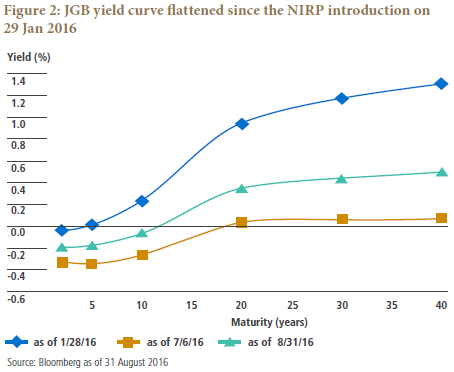

Second, there is a limit to how flat the yield curve can become before it begins to hurt rather than help the economy. Since the BOJ’s surprise introduction of NIRP at the end of January, the JGB curve has flattened dramatically (see Figure 2). While the BOJ cut the rate of interest on excess reserves (IOER) by only 20 basis points (bps), 40-year JGB yields fell by almost 100 bps to 0.06% in early July. Theoretically, of course, the lower rates at longer maturities are more stimulative for the economy. But we think the extent to which extraordinarily low rates have stimulated new productive investments (as opposed to refinancing of existing debt) is highly questionable. Also, practically speaking, excessively low rates and a flatter yield curve will weaken financial intermediation for the economy as they persist: Lower reinvestment yields and higher liability valuations will cost banks, insurance companies and pensions, and thus reduce their risk-taking capacity. Kuroda, in his most recent speech, finally admitted this side effect of his current policy.

The New Neutral yield curve

The BOJ faces a complex challenge: It needs to optimize its policy toolkit such that it can maintain extraordinary monetary accommodation for many years (and add more accommodation when appropriate), while also considering the practical limit on JGB purchases and the effective lower bound of the long end of the yield curve. How can it solve this puzzle?

We’ve talked about neutral interest rates, which are often equated to central bank policy rates. Discussing neutral rates in terms of policy rates is appropriate for a central bank – such as the Federal Reserve – that has already concluded a quantitative easing (QE) program and is operating in a policy rate regime. But for a central bank such as the BOJ, which is trying to influence the yield curve directly (rather than indirectly through its policy rates), it may be more appropriate to discuss the neutral rate concept in the context of the yield curve. Conceptually, a neutral yield curve is a real yield curve that is neither expansionary nor contractionary for the economy. If the central bank can keep the actual (real) curve below the hypothetical neutral curve with its policy toolkit, it may help stimulate the economy (although beyond a certain level, decline of the entire yield curve could become more costly).

Applying The New Neutral yield curve

Estimating the neutral curve helps us identify which part of the yield curve is more or less effective in stimulating the economy. According to a paper by BOJ staff, Japan’s economy is stimulated by cuts in the short-to-intermediate portions of the curve, and at 10 years or more, the results begin to diminish. In Japan, the corporate sector borrows predominantly in the short-to-intermediate part of the yield curve, presumably because of longer-term economic uncertainty. The BOJ staff’s findings suggest that the economic benefit of Japan’s flatter curve is likely to diminish as the flattening becomes excessive.

Furthermore, if we also take into account the potential side effects of a lower and flatter curve on financial institutions, which the BOJ staff’s model does not incorporate, Japan’s neutral curve should look steeper than otherwise would occur. Again, excessive yield declines and curve flattening would negatively affect the economy through weaker financial intermediation.

This may be good news for the BOJ, which faces a practical limit on JGB purchases. The central bank does not need to, or even should not, lower the longer end of the actual curve (particularly 30 years or more) too much. The bank could safely reduce long-end JGB purchases without harming the economy.

The BOJ needs to prepare for the longer war against deflation. As the BOJ hits the limits of its innovative policy framework, the central bank may need to make some adjustments to it. And we think The New Neutral yield curve concept plays a critical role here. Under its current policy, the BOJ has been trying to lower the whole yield curve. However, we believe Japan’s New Neutral yield curve is probably steeper than the BOJ would have estimated. In our view, the bank could scale back JGB purchases – particularly on the long end – without damaging the economy, which would help preserve ammunition for the longer war. Cutting interest rates a bit further negative, on the other hand, could still be an option to lower the shorter end of the yield curve.

As former Governor Masaaki Shirakawa used to say, the BOJ has been a front-runner in unconventional policies. Targeting the yield curve against The New Neutral yield curve could mark a new chapter for the BOJ and for global central banking.

All investments contain risk and may lose value. This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. THE NEW NEUTRAL is a trademark of Pacific Investment Management Company LLC in the United States and throughout the world.

©2016, PIMCO.