As interesting and sometimes even amusing as it is to look back in time and reflect, as investors we get paid for looking forward and anticipating what may come. In this respect there’s a few existing trends and themes that will remain front of mind for me this year and will be key to keep on your radar in understanding the risks and opportunities in 2018.

Following is a selection of the key charts and indicators, the themes span inflation, monetary policy, commodities, China, emerging markets, corporate bonds, global equities, volatility, and bond yields. In other words, all the issues and topics that most active asset allocators should be thinking about. I'll be covering these topics in more detail in the coming weeks.

I've said it before and I'll say it again: 2018 is going to be harder and more complex for investors than 2017. The cross currents of rising valuations across asset classes and markets, maturing of the business cycle at a global level, and the turning of the tides in monetary policy could make 2018 a watershed year.

That all said, here's the charts! Best wishes and best of luck for 2018.

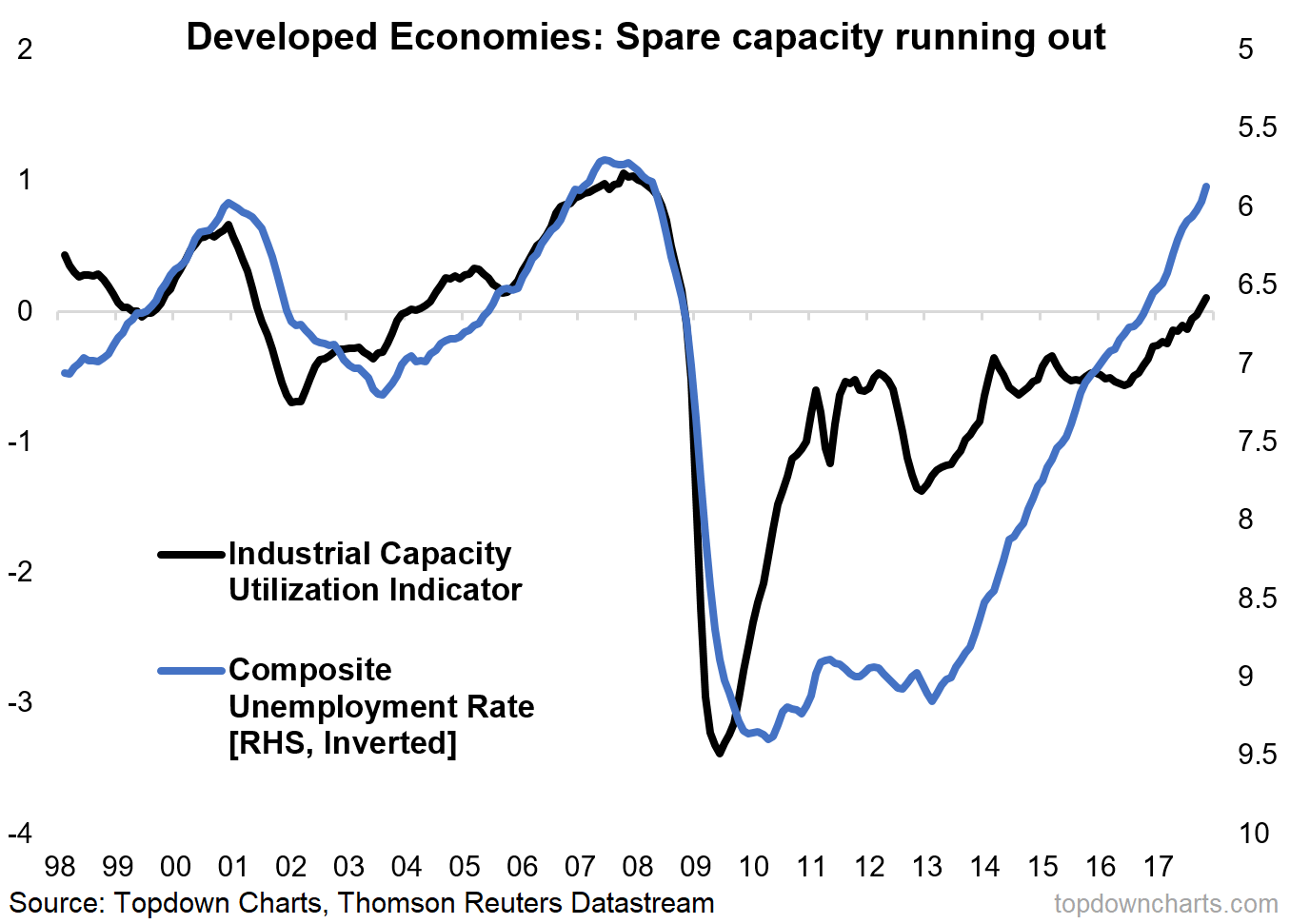

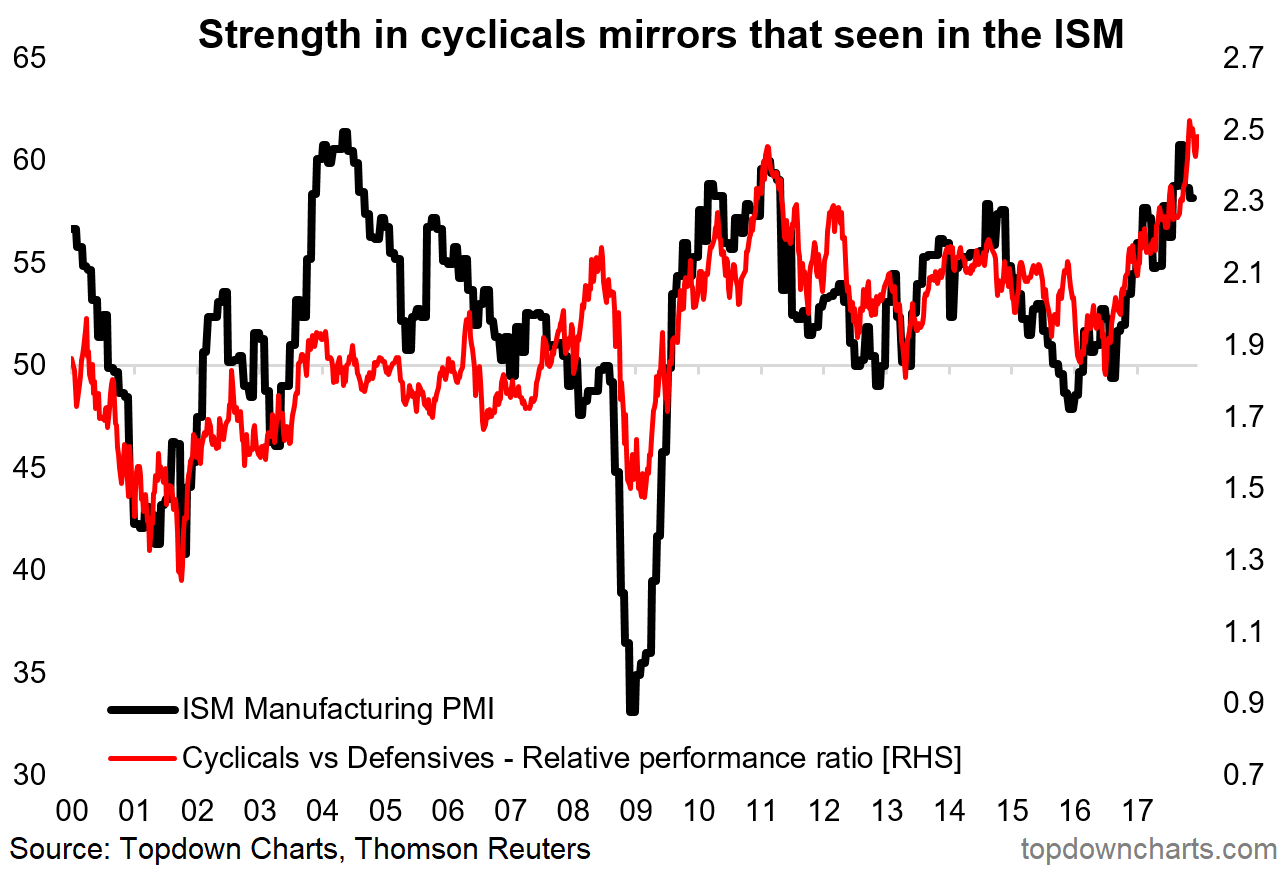

- Much better cyclical economic prospects across developed economies has seen measures of industrial capacity and labor market tightness return to pre-crisis levels. This is probably the best leading indicator of a rise in inflationary pressures and reflects a maturing global business cycle.

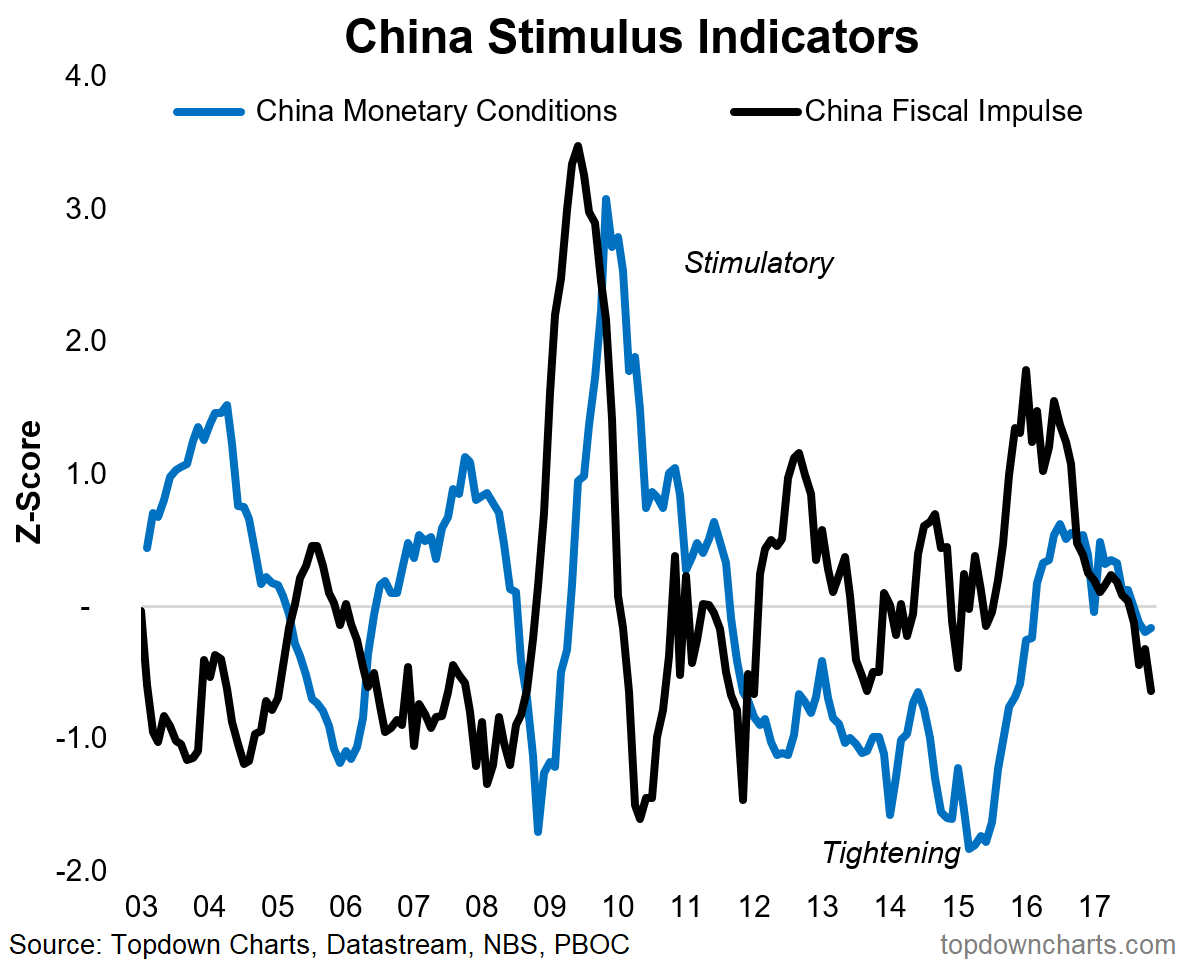

- Last but certainly not least is China. A number of the big tailwinds (property, exports, stimulus) that helped China avoid a recession in 2015/16 are starting to turn. The fiscal/monetary policy stimulus indicators in this chart helped us pick the upturn in China before most others caught on, and I think this will be a key one to monitor when thinking about the outlook for China in 2018 and beyond.

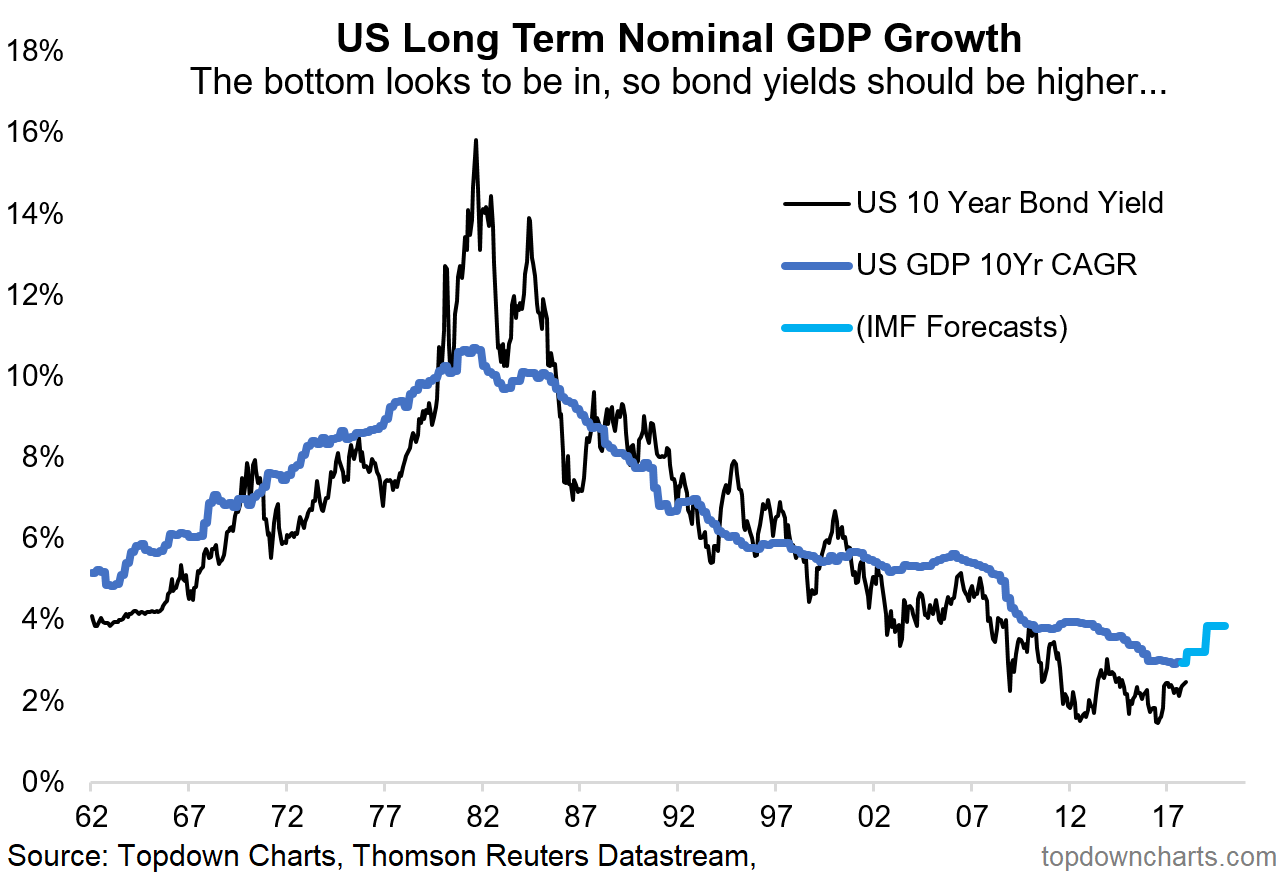

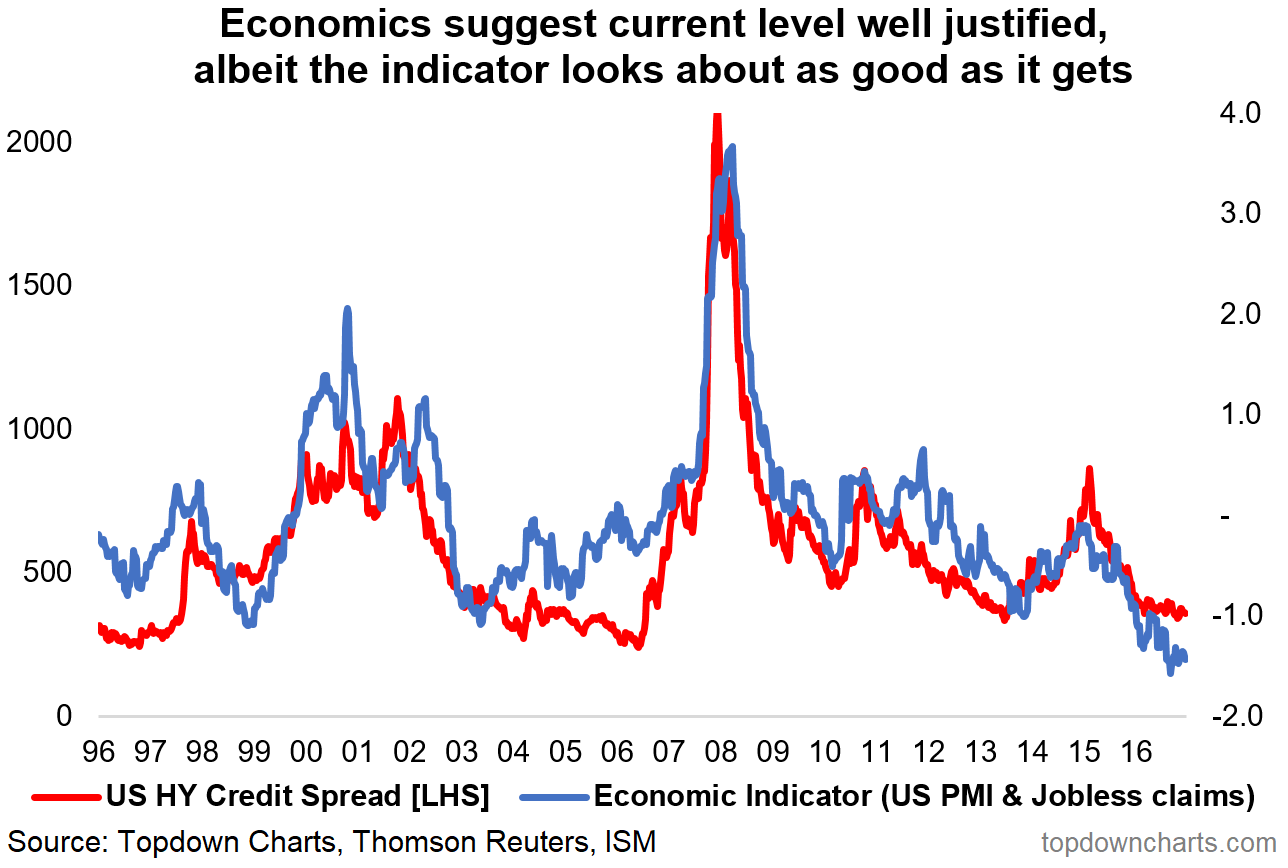

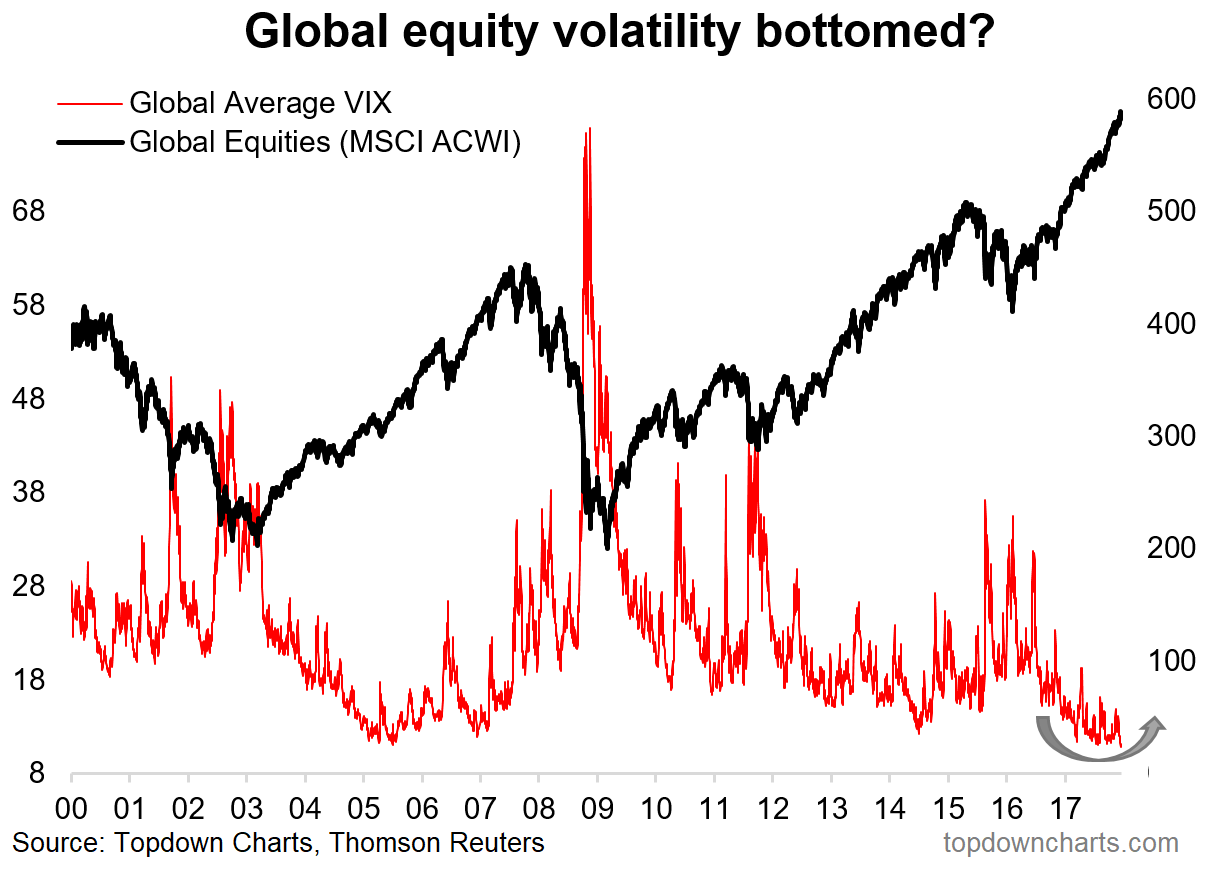

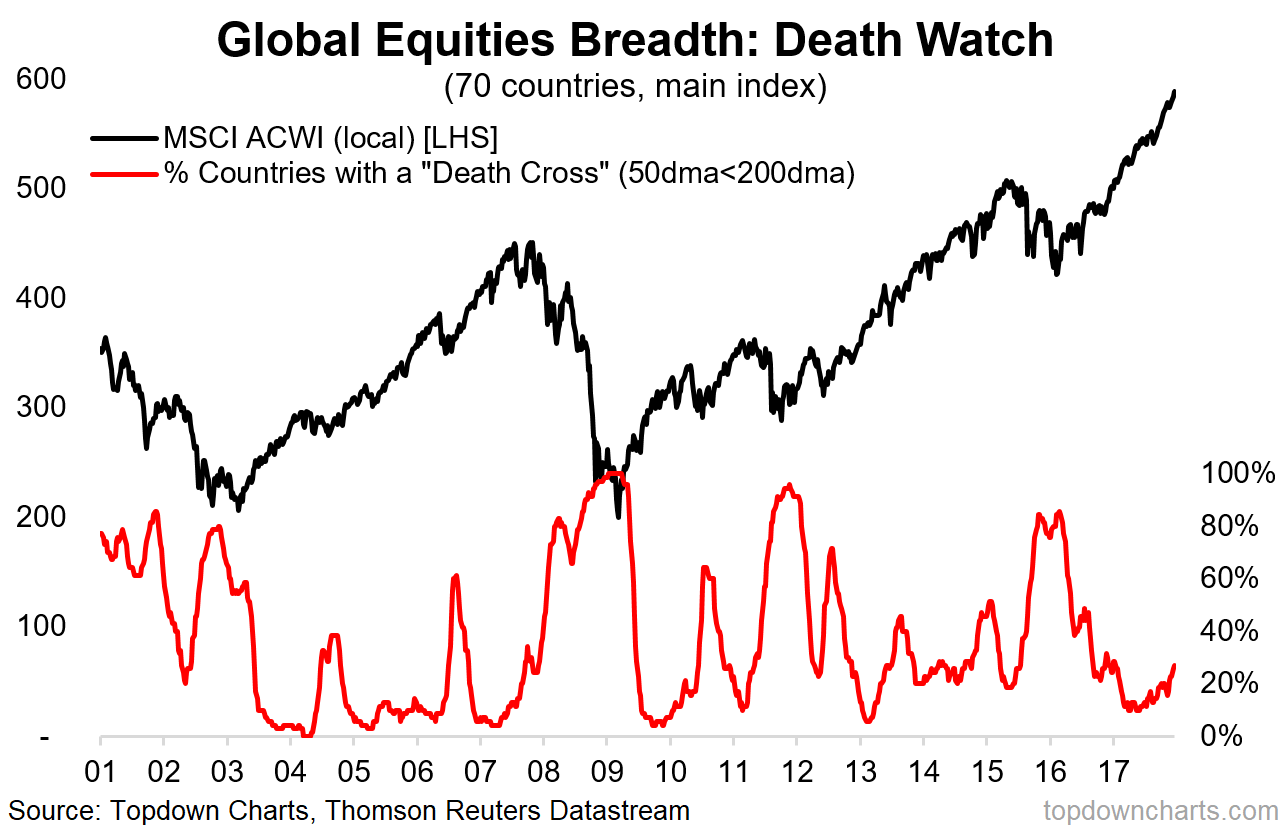

Tying it all together, the main takeaways are that on a macro front, inflation is set to re-emerge this year and will reinforce the global turning of the monetary policy tides, and underpin a bearish-bonds bias. Across a spectrum of risk pricing metrics, all appears calm (complacent?) at this stage, while the economic indicators for now reinforce this second "great moderation".

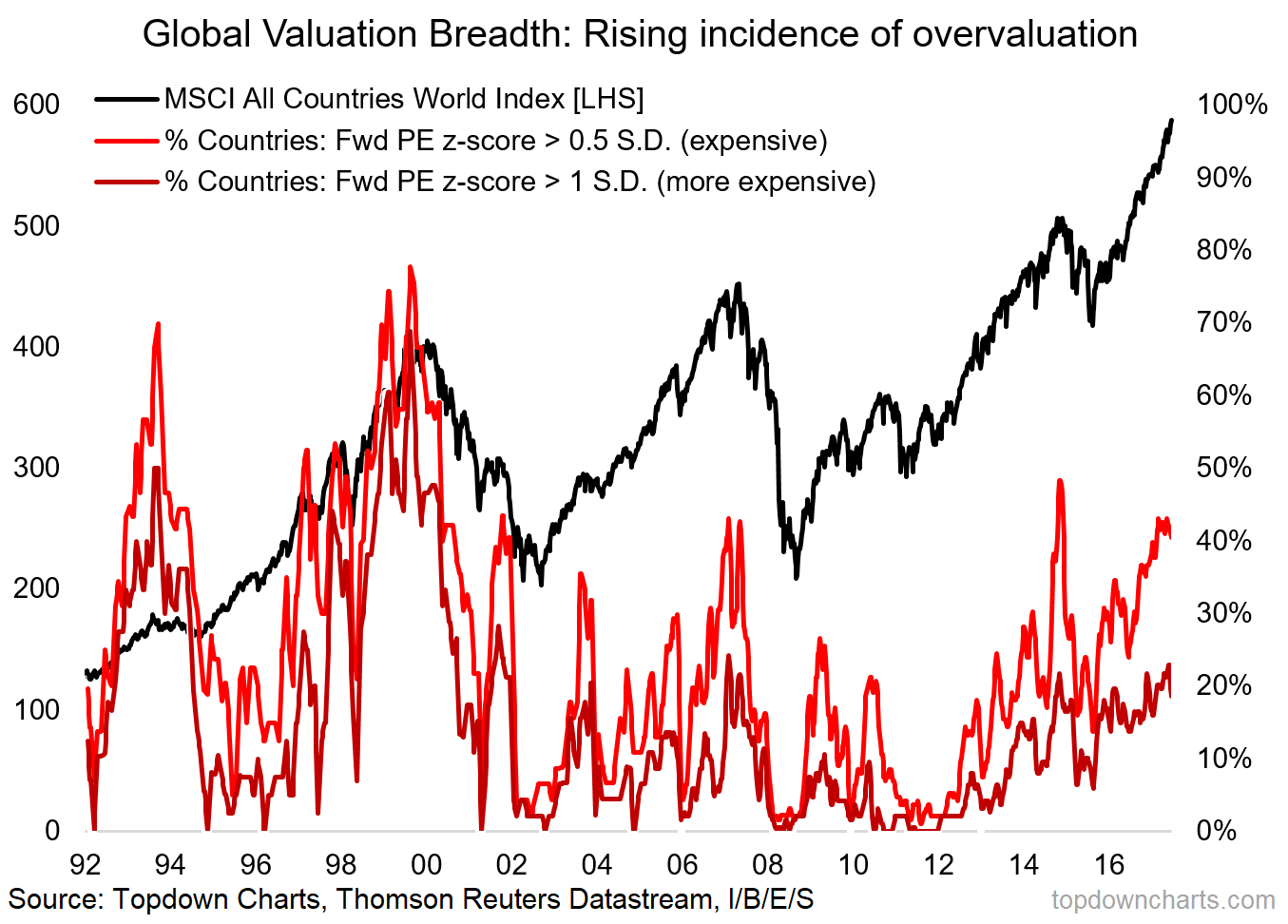

Greater incidence of overvaluation across markets and asset classes mean the stakes are progressively higher as the cycle matures. Along with a turning of tailwinds in China, this all means that 2018 will likely be a more challenging year for investors and a possible watershed moment for global markets.

At this stage we remain selectively bullish on global equities (paying attention to relative value), cautiously bullish emerging markets, and bearish commodities (in aggregate) over the medium term. On the defensive side we remain bearish on bonds (particularly global sovereign), in preference of cash to perform the role of capital preservation.

Overall there is pressure to reduce the time horizon and a greater sense of readiness to shift positioning/views should the data and indicators justify it, particularly as short-term risks build. While 2018 will likely be 'harder', it will most likely be a case of great challenges and great opportunities.

Sincerely,

Callum Thomas

Head of Research

Topdown Charts

www.topdowncharts.com

© Topdown Charts

© Topdown Charts

Read more commentaries by Topdown Charts