Recent tax reform has increased the dialogue around state preference municipal portfolios, and some municipal investors are inquiring whether state-specific or state preference portfolios are a good fit in the current environment. We have found that although state-specific municipal bond separately managed accounts may offer tax benefits at the state and local level, investors often are better off allocating at least a portion of their portfolios to out-of-state (national) securities to improve diversification, credit quality and after-tax yields. The question is which solution or blend is best for a given investor, and a number of factors inform whether a state-specific portfolio may make sense.

Weighing state-specific municipal bond separately managed account solutions

PIMCO offers many state-specific and state preference municipal bond separately managed account strategies, including muni bond ladders, and can customize investor portfolios across a number of parameters. When determining the appropriate allocation to in-state versus national bonds, we consider several key factors:

- The investor’s effective tax rate

- The state’s credit outlook

- In-state supply/demand dynamics

- After-state-tax yields on out-of-state (national) bonds

We review these factors quarterly, updating our in-state offerings as needed to ensure the right balance of diversification, liquidity, capital preservation and attractive after-tax return potential for each investor.

High state tax rates don’t always favor state-specific portfolios

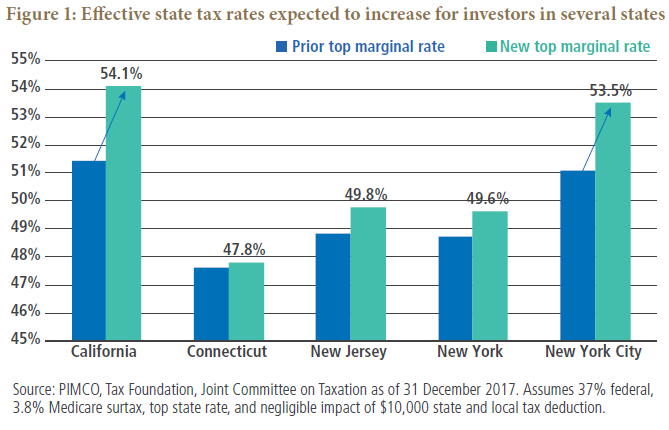

Though top marginal tax rates declined under federal tax reform, the new $10,000 cap on deductions for property, income and sales taxes paid locally is expected to raise effective tax rates in some states (see Figure 1). These include California, Connecticut, New York (especially New York City) and New Jersey, where state and local tax deductions average $18,000–$20,000 – well above the new limit.

Does this mean investors in those states should seek 100% in-state allocations to offset the impact? Not necessarily, given differences in issuance volumes and credit quality among these states. PIMCO’s forward-looking credit outlooks at both the state and issuer level are a key pillar of our municipal investment process and a critical element in how we assess our in-state offerings. We caution against a 100% allocation to states with negative credit trajectories and limited opportunities to diversify away from state credit exposure.

Given these considerations, PIMCO currently favors a 100% allocation to in-state municipal bonds for investors in California and New York (including New York City) – typically among the largest issuers of municipal debt annually. The tax advantage in these states can make in-state allocations desirable. Furthermore, ample in-state issuance provides opportunities to effectively diversify a 100% in-state municipal portfolio without sacrificing yield or credit quality.

The same is not true for investors in New Jersey and Connecticut. While effective tax rates are poised to go modestly higher in both states, we believe clients should weigh this against state credit risks and budget issues, along with low in-state issuance, which limits in-state diversification. New Jersey and Connecticut credit outlooks, in our opinion, are negative due to large unfunded pension liabilities and growing structural deficits. Many credits within these states are vulnerable to budgetary pressures due to appropriation risks, which further limit investors’ ability to diversify away from state credit risk. PIMCO suggests New Jersey and Connecticut residents consider investing at least a portion of their municipal allocations in national bonds for better diversification and, in some instances, higher after-state-tax yields.

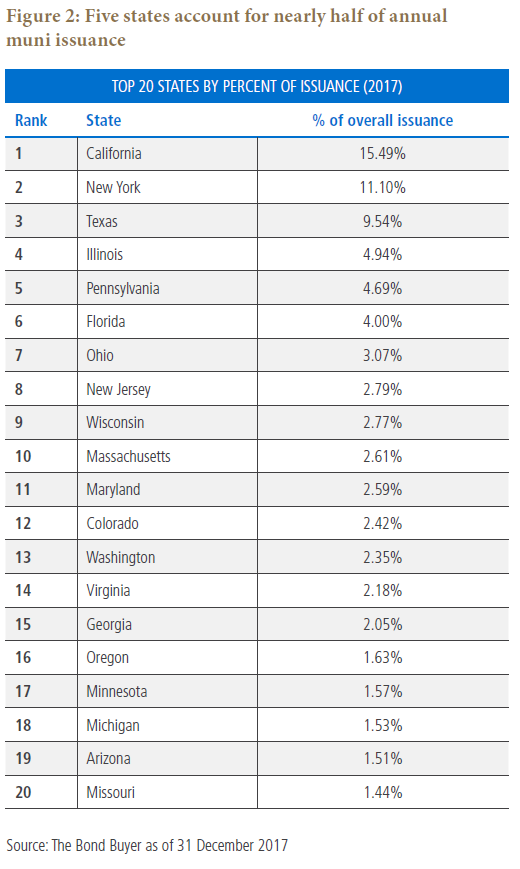

A handful of states issue the lion’s share of bonds, creating supply/demand imbalances

Municipal market supply/demand dynamics are another key consideration when evaluating the appropriate allocation to in-state bonds. While the municipal market is large, with more than 55,000 active issuers across 50 states and five territories, a handful of states account for the bulk of issuance annually. The top five issuers represented nearly half of issuance in 2017, while those ranked sixth or lower each issued no more than 4% of annual issuance (see Figure 2).

SUBSCRIBE NOW TO LEVERAGE PIMCO’S MUNI MARKET EXPERTISE.

The resulting imbalance of supply and demand, particularly in states with strong demand but limited high quality supply, may lead to higher prices (or lower yields) on in-state municipals versus comparably rated national municipal bonds. In these instances, investors may be able to achieve higher after-state-tax yields and better diversification by allocating at least a portion of their portfolio to out-of-state bonds.

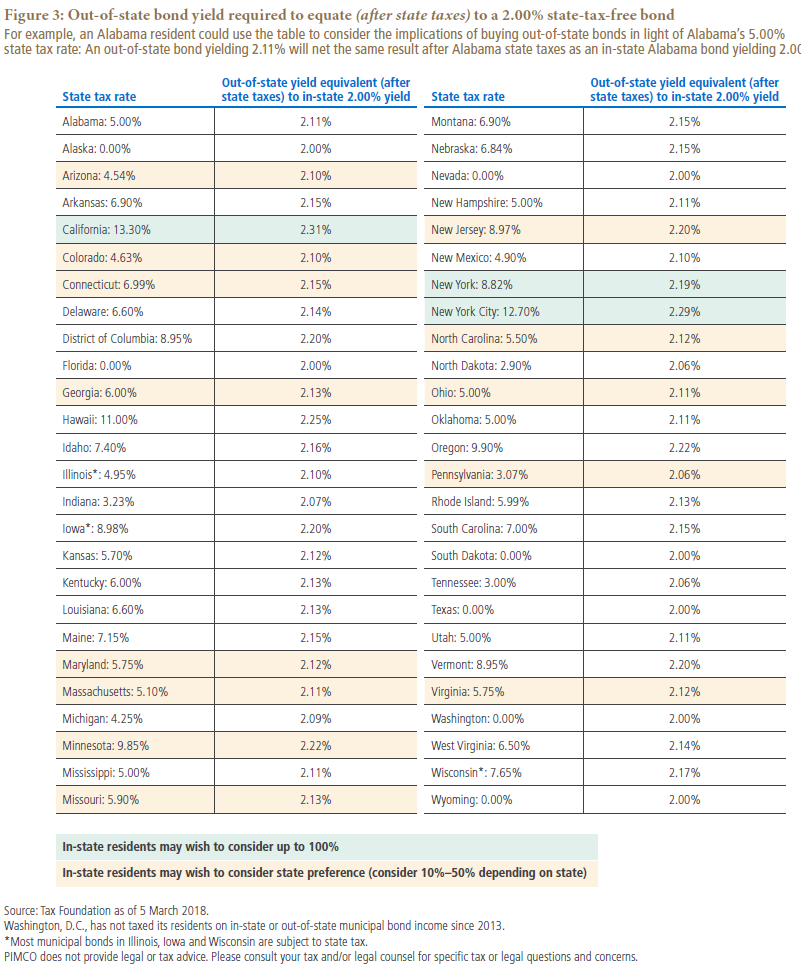

Equivalent after-state-tax yields should inform allocations

Consider the following example: AAA rated Texas issuers with 10-year maturities currently trade at roughly 0.20% higher yields than many in-state AAA bonds in high tax areas. This means some out-of-state investors may be better off investing in national securities like these when considering after-state-tax yield, diversification and credit quality.

As Figure 3 shows, clients often need only achieve 0.10 to 0.15 percentage points (bps) of yield pickup in the national market versus comparable in-state bonds to achieve the same after-state-tax yield as an in-state bond yielding 2%. This is generally achievable given current supply/demand dynamics in the municipal market and reinforces our view that investors may potentially be better off with fully national portfolios or a blend of in-state and national bonds.

Navigating a changing landscape

PIMCO’s flexible, active approach to municipal investing is critical to navigating the evolving tax landscape, the credit outlook at the state level, and supply/demand dynamics as investors seek to optimize after-tax returns. We continue to partner with investors to determine the allocation to in-state versus out-of-state municipal bonds that will work best for their individual circumstances and needs.

© PIMCO

© PIMCO

Read more commentaries by PIMCO