The U.S. economy in late 2025 presents a complex but increasingly coherent picture. Labor market dynamics, trade policy uncertainty, and evolving monetary conditions are each contributing to a recalibration of the economic landscape. While headline jobs growth has clearly decelerated, underlying indicators suggest a maturing business cycle but not a collapsing one. Meanwhile, the increasing probability for rate cuts by the U.S. Federal Reserve (Fed) and positive signals from business credit markets provide a cautiously optimistic foundation heading into 2026.

Tempering our optimism is the trajectory of jobs growth, which has been slowing throughout 2025 but reflects more than just weakening demand for labor. On the demand side, the monthly Job Openings and Labor Turnover Survey (JOLTS) continues to show a decline in job openings, which confirms that employers are moderating their hiring plans. This is consistent with a broad economic cooling of the business cycle.

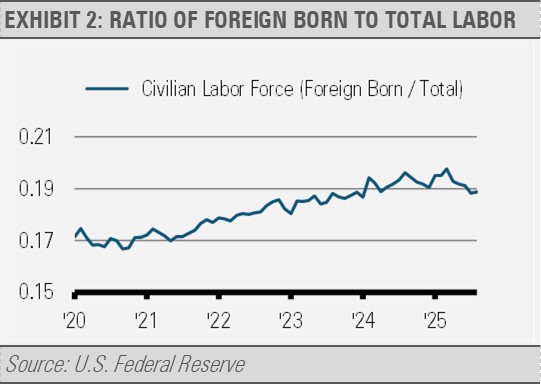

On the supply side, we are seeing a contraction in the labor force largely due to reduced immigration as stricter policies this year have constrained the labor supply.

This jobs growth deceleration has helped keep the unemployment rate low and hovering just above 4% even as net new job creation declined. With labor supply and demand closer to equilibrium, wage growth appears to be stabilizing, which helps offset the effects of inflation.

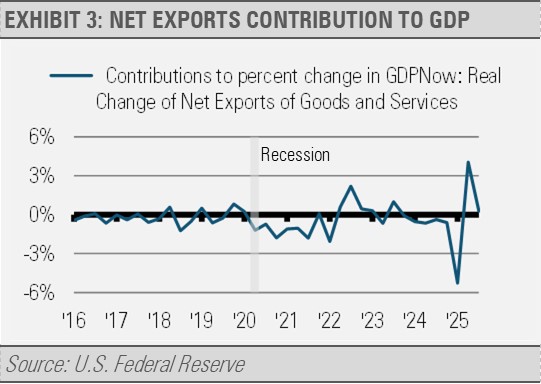

Additionally, the foreign trade environment appears to be stabilizing as evidenced by the muted contribution of net exports to the Atlanta Fed’s GDPNow model in the current quarter.

Meanwhile, policy makers, businesses, and market participants are awaiting a major Supreme Court ruling on the legality of certain executive-imposed tariffs. If upheld, the status quo remains. However, if the court strikes down these tariffs, we could see a notable rebound in the sectors hardest hit, particularly automotive and industrial manufacturing. Investors and policy analysts are watching this ruling closely, as the implications for corporate margins and supply chains could be significant.

Investors are expecting the Fed to cut rates by 25 basis points (0.25%) at each of the next three meetings. This would represent a meaningful step toward normalization, especially after an extended period of restrictive policy. However, it is important to note that even with these cuts, short-term interest rates would remain above the Fed’s estimated long-term neutral rate of approximately 3%. When viewed alongside tepid money supply growth, monetary policy remains tight by historical standards.

This tension is increasingly important given recent labor market data revisions. The Bureau of Labor Statistics recently revised job growth estimates downward by over 900,000 positions for the past year, signaling that the labor market may be weaker than previously believed. These revisions support the case for policy easing sooner rather than later.

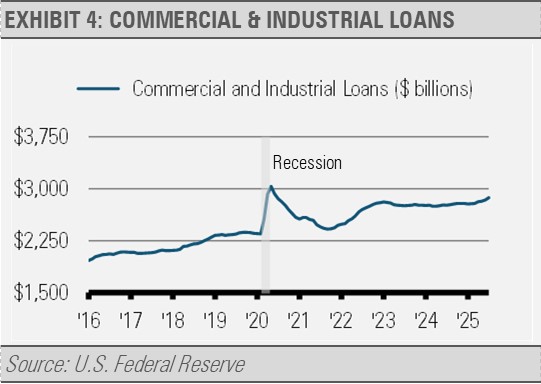

Perhaps the most encouraging economic signal lies in the recent uptick in commercial and industrial (C&I) loans. Business borrowing, after peaking during the pandemic due to aggressive liquidity management, hit a floor in late 2021 and stagnated through much of 2023 and 2024. The recent increase in borrowing suggests that business leaders are once again seeing viable opportunities for investment. This shift implies growing confidence in future demand, which could ultimately drive capital expenditures and productivity growth.

INVESTMENT IMPLICATIONS

The U.S. economy is transitioning but not collapsing. Slower jobs growth, moderating wage inflation, and stable unemployment point to a labor market nearing equilibrium. When the labor market is at equilibrium, the number of jobs employers want to fill closely matches the number of people willing to work at a specific wage rate, which results in a stable market. Additionally, trade policy remains a wild card, with a pending Supreme Court decision holding potentially large implications. Meanwhile, rate cuts are expected, but tight monetary conditions persist. Against this backdrop, a rebound in business lending could become a key catalyst for sustaining economic momentum. We continue to favor quality U.S. businesses as well as investment grade fixed income, such as asset-backed securities, in the belly of the yield curve.

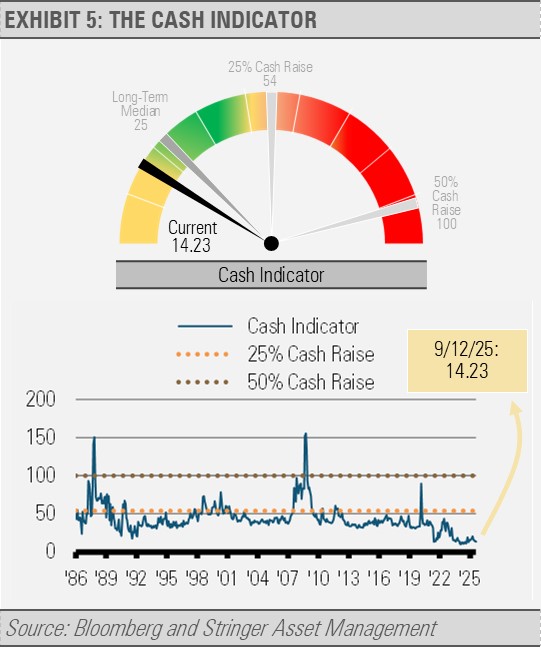

THE CASH INDICATOR

After bouncing off very low levels and jumping with April’s tariff-related uncertainty, the Cash Indicator (CI) has been range bound below its historical norms. These low levels suggest that markets are somewhat complacent and not pricing in much risk, which leaves markets more susceptible to shocks than normal. Still, with a positive economic backdrop, we view bouts of volatility as opportunities to increase allocations to high quality businesses.

For more news, information, and strategy, visit the ETF Strategist Content Hub.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.

A message from Advisor Perspectives and VettaFi: Interested in learning more about how bond ETFs can help diversify your portfolio? Click here to read more.

Read more commentaries by Stringer Asset Management