Key takeaways

- Recent geopolitical events and private credit market concerns have increased bond market volatility, influencing expectations for Federal Reserve policy and Treasury yields while raising questions about credit market spillover risks.

- Contrary to typical safe-haven behavior, 10-year Treasury yields rose sharply after the attacks on Iran, driven by inflation expectations and a shifting federal funds outlook. We expect the 10-year Treasury yield to stay above 4%, supported by inflation and fiscal concerns.

- We suggest that investors not overreact, favor intermediate-term maturities and higher-rated bonds, and prepare for potential short-term volatility amid uncertain economic and geopolitical conditions.

Bond market volatility has picked up following the attacks on Iran, with more questions than answers about the ultimate impact on economic growth and inflation. The attacks come on the heels of a wave of negative headlines around the private credit markets and how that might influence Treasury yields and corporate bond values.

Prior to these events, the U.S. economy appeared to be on solid footing, but the markets are likely to focus on these risks over the short run. Below we'll discuss the market reaction and potential impact on Federal Reserve policy, the direction of Treasury yields, and potential spillover to the publicly traded credit markets.

Federal Reserve policy: One or two rate cuts still likely

Coming into 2026, we expected the Federal Reserve to cut its benchmark interest rate one or two times by the end of the year, with the next rate cut likely not coming until the middle of the year. Despite signs of stabilization in the labor market, sticky inflation suggested that the Fed could take a patient approach to any policy shifts. Our view hasn't changed following the recent events in the Middle East.

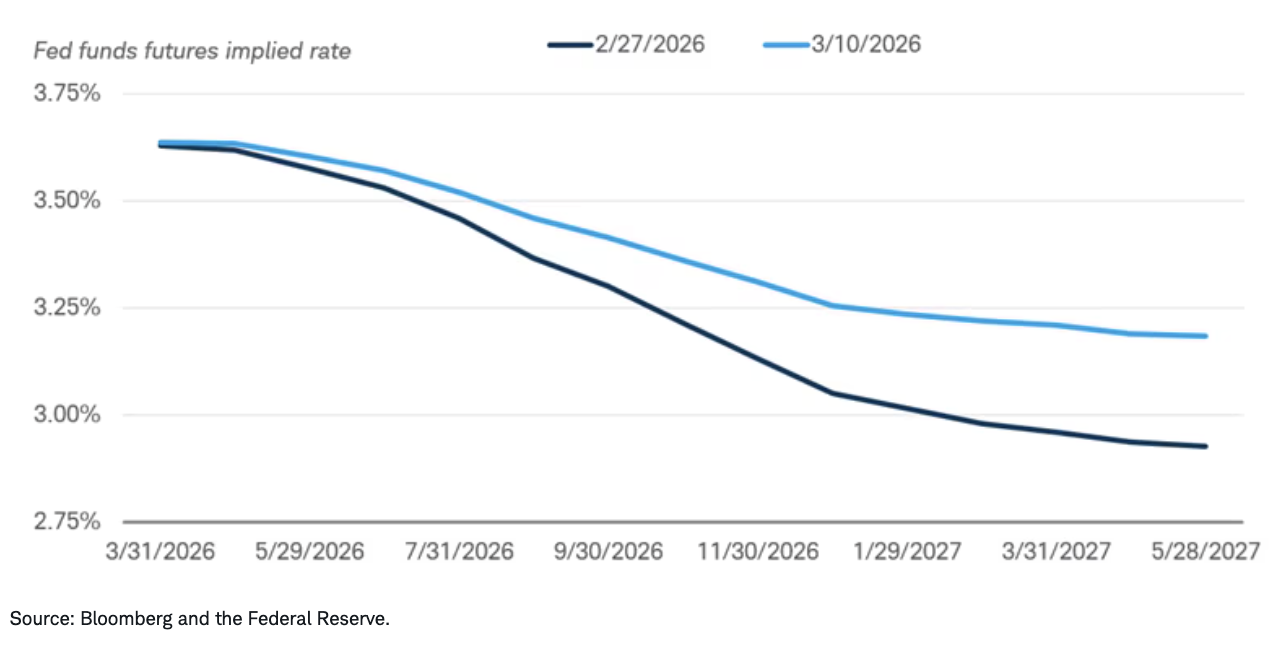

We expect the Fed to continue to take a cautious view before deciding on any change in policy. Although the war in Iran is potentially inflationary, a prolonged conflict and elevated oil prices could also slow economic growth and lead to higher unemployment or tighter financial conditions. For now, elevated inflation is likely to outweigh growth concerns. Several inflation readings are still in the 2.5% to 3% range. The increase in oil prices risks inflation moving further away from the Fed's 2% inflation target. That's the view that investors generally have, as the federal funds futures market isn't fully pricing in a rate cut until the September meeting, and fewer cuts over the next year are currently priced in relative to what was expected at the end of February.

Federal funds futures are now pointing to a higher year-end rate

Long-term Treasury yields are likely to remain elevated

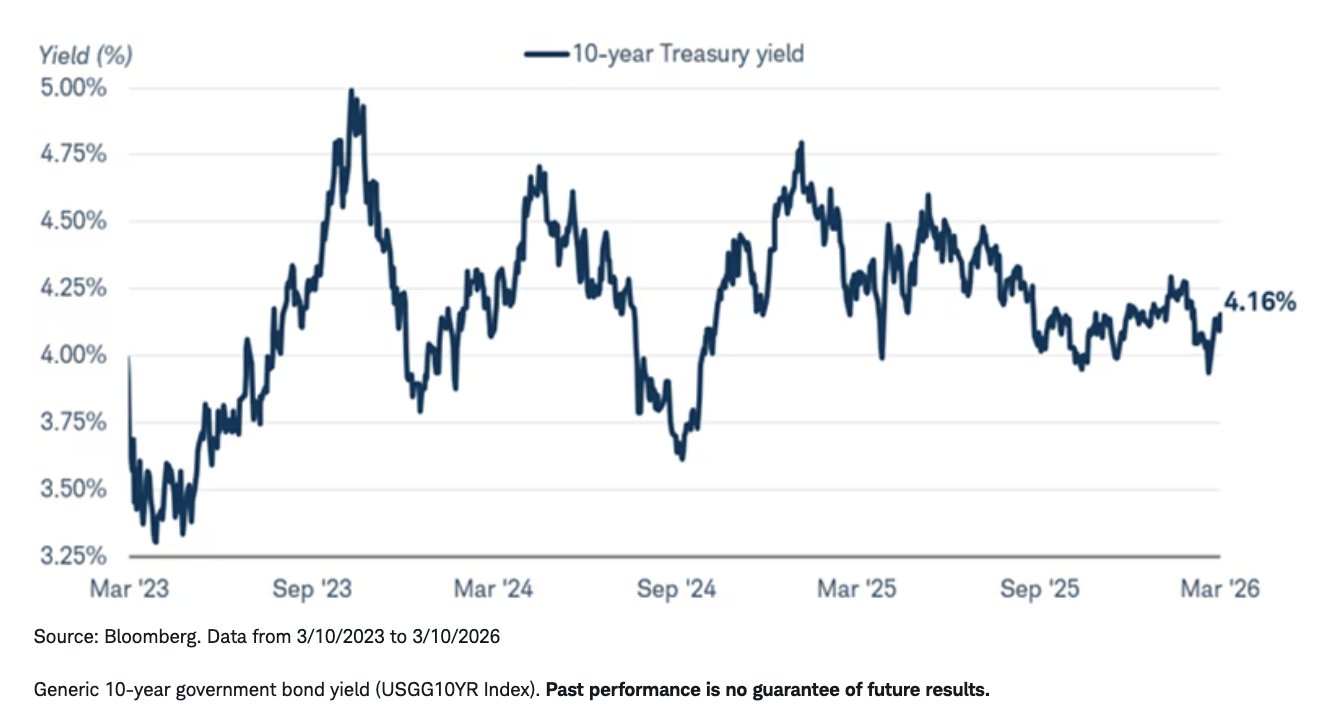

Long-term Treasury yields increased in the days following the attacks, potentially catching some investors off guard. In situations like this, investors tend to focus on perceived safe-haven investments like U.S. Treasuries, pulling their prices up and their yields down.

Instead, the 10-year Treasury yield jumped from a weekend low of 3.93% up to as high as 4.2% on an intraday basis on Monday, March 9th as investors appeared to focus on the potentially inflationary impact of the oil spike, rather than on the potential hit to growth. It closed at 4.16% on March 10th.

We continue to expect the 10-year Treasury yield to trade above 4% but given the fluidity of the situation in the Middle East, a wide range of outcomes could result in elevated volatility. Wars tend to be inflationary over time as supply shocks tend to drive up prices, and they need to be financed by more debt issuance. Budget concerns—the need to finance deficits with more and more debt—pose a risk if demand doesn't keep up with the increased supply. That may become more of a risk if the conflict lasts longer than expected.

We see the downside for the 10-year Treasury yield in the 3.75% region, and we'd likely need to see recession risk rise for it to break below that. In a prolonged conflict, oil prices may rise higher and stay elevated for longer, and a disruption in global energy supplies could slow down economic growth. That would likely be a catalyst for lower yields, but for now inflation risk remains at the forefront.

The 10-year Treasury yield has risen since the end of February

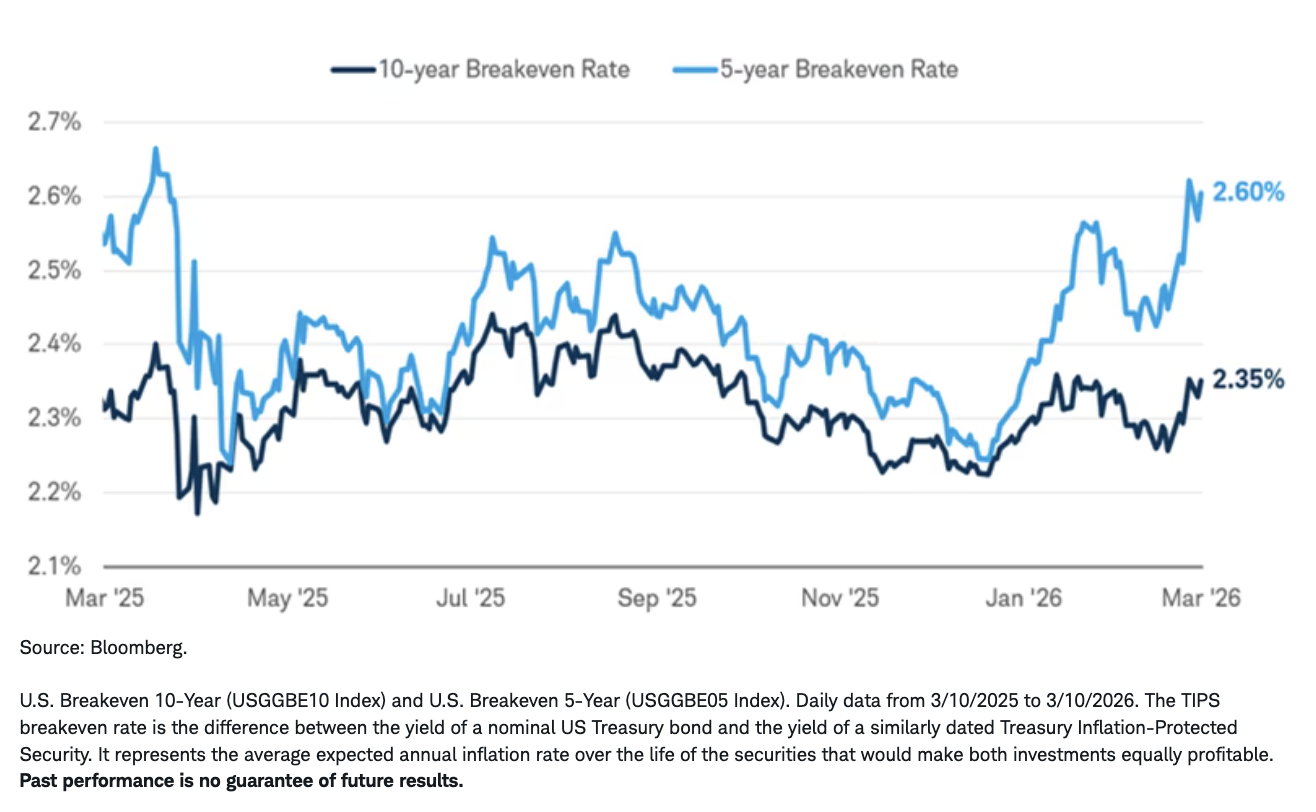

We can break down movements in Treasury yields based on fed funds expectations, inflation expectations, and a "term premium." All three were drivers of higher yields in the first week of March. Inflation expectations, derived from Treasury Inflation‑Protected Securities (TIPS) breakeven rates, rose along with oil prices, with the five-year breakeven rate near its one-year high, and the 10-year breakeven rate near its highest level since September 2025.

TIPS breakeven rates have increased

With inflation expectations still elevated, TIPS may help buffer portfolios against further price increases and can help offer protection if inflationary conditions worsen.

If the oil shock persists, it could contribute additional inflationary pressure. Meanwhile, most inflation measures remain well above the Fed's 2% target, and Treasury yields are expected to stay elevated. As a result, traditional fixed‑income investments may be more vulnerable to the effects of sustained inflation, and adding some inflation protection in the form of TIPS can help protect against the risk of even higher inflation. It's important to remember that TIPS are still bonds, however, and while they can protect against inflation over time, their values can still fluctuate in the secondary market if their yields rise.

Will private credit concerns spill over to the public markets?

The Iran attacks follow a recent wave of negative headlines around the private credit markets. "Private credit" investment strategies can mean many things, but they generally involve financing corporate, physical, or financial assets on a private basis. Headlines lately have revolved around direct lending, or loans to corporations and businesses. These loans are generally made to riskier companies—often those with high leverage, or debt, relative to their earnings—although some private credit strategies involve loans made to what would be considered investment-grade issuers.

It's not an apples-to-apples comparison, but private credit investments can be similar to those of high-yield corporate bonds or bank loans, which generally have sub-investment-grade, or "junk," ratings. With a high-yield bond or bank loan mutual fund or exchange-traded fund (ETF), you can generally see the holdings. With private credit investments, that information isn't widely shared.

The negative headlines regarding private credit have come in a few forms. Some funds have marked down the net asset value of the fund itself or of specific loans held in the fund, but making more headlines are large redemption requests for some funds. Private credit funds are generally illiquid, meaning they can't be bought and sold as easily and quickly as mutual funds or ETFs. Rather, many funds have quarterly redemption limits, like a limit that states the fund may only redeem up to 5% of its assets each quarter. If many investors decide to redeem at the same time, those limits may be reached, and investors may not be able to redeem as much as they wished.

Our concern is the potential spillover to the public markets, which are generally more accessible to a larger swath of investors. So far, the spillover to the high-yield bond market has been relatively small, but we have seen a greater impact on the bank loan market, also known as the leveraged loan market.

Leveraged loans are generally loans made to sub-investment-grade issuers. The loans have floating coupon rates and are backed by a pledge of the issuer's collateral. High-yield bonds are issued by sub-investment-grade companies, tend to have fixed coupon rates, and are unsecured. High-yield bonds tend to be more liquid than leveraged loans.

We see more potential spillover risk to the leveraged loan market than the high-yield bond market, for three reasons. These factors should allow high-yield bonds to potentially outperform leveraged loans, but the spillover risk could still result in volatility and potential price declines in high-yield bonds as well.

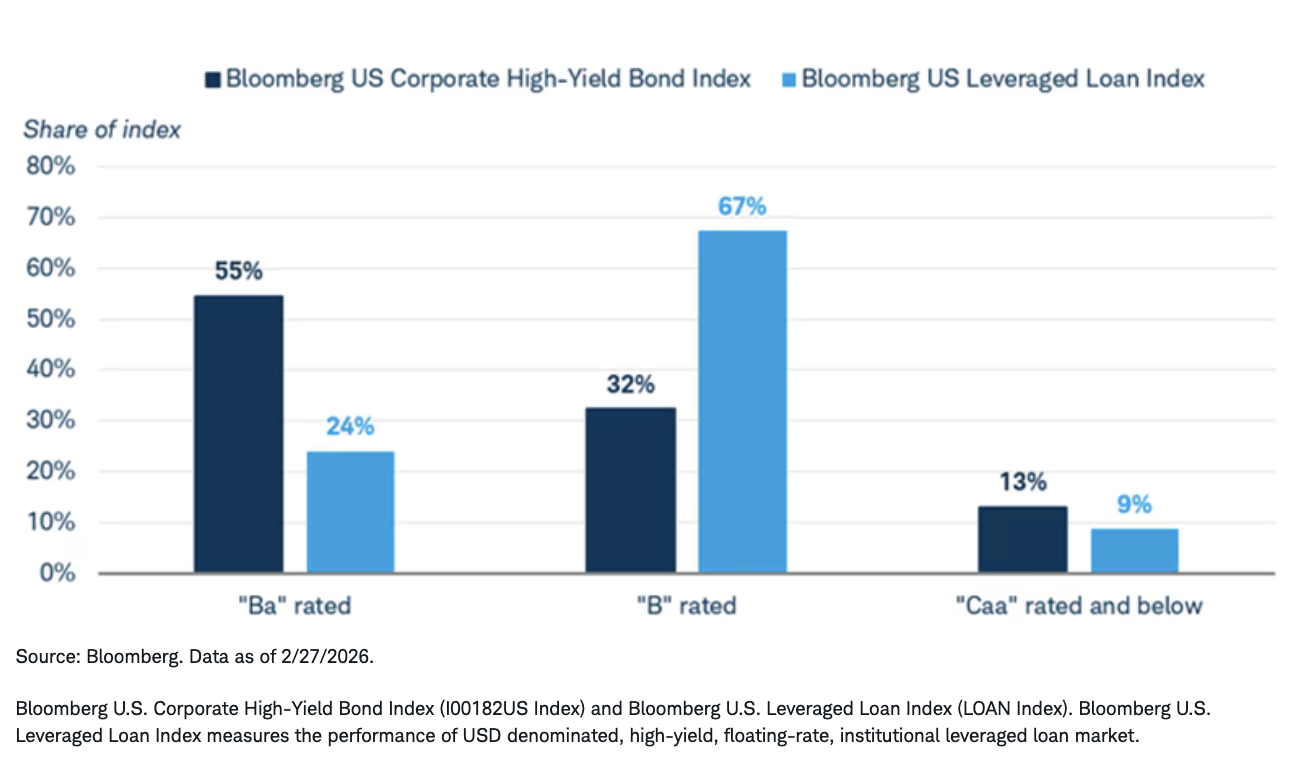

First, high-yield bonds tend to have higher average credit ratings than leveraged loans. Roughly 55% of issues in the Bloomberg U.S. Corporate High-Yield Bond Index have BB ratings, while more than 75% of the issues in the Bloomberg U.S. Leveraged Loan Index have ratings of B or lower.1

The high-yield bond index has higher-rated issues than the leveraged loan index

Second, leveraged loans have more exposure to technology issues given the artificial intelligence-driven capital expenditures than the high-yield bond market. Tech issues make up roughly 20% of the leveraged loan index, compared to just 8% of the high-yield bond index (as of March 5, 2026).

Third, potential Fed rate cuts would likely mean lower coupon payments from leveraged loans down the road given their floating coupon rates. The fixed-rate coupons that high-yield bonds offer can help mitigate the risk of falling short-term yields.

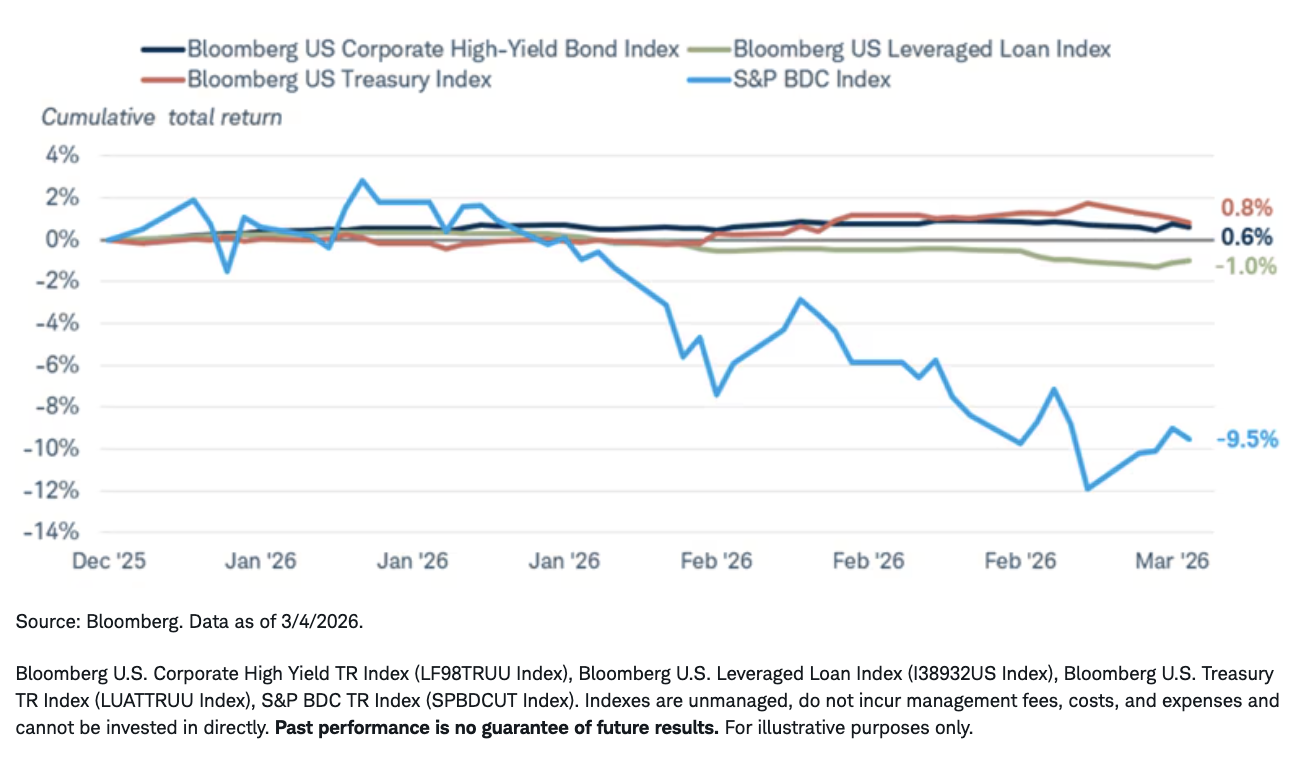

Those benefits have helped high-yield bonds outperform leveraged loans over the last few months, but they have underperformed Treasuries. The chart below also includes the S&P BDC Index, which tracks business development companies (BDCs). A BDC is a special type of investment that combines attributes of publicly traded companies and closed-end (private) investment vehicles; they generally invest in the debt and equity of small to mid-sized U.S. companies. The investments made by BDCs are likely to be somewhat similar to the investments made in private credit funds.

Business development companies have strongly underperformed so far this year

Although we believe the outlook for high-yield bonds is more positive than the outlook for leveraged loans, both are at risk of heightened volatility and potential price declines. The chart above highlights that performance can suffer over shorter holding periods when investors get jittery. With elevated uncertainty given the war in Iran, now is not necessarily the time to be aggressively adding risk to portfolios.

What to consider now

Don't overreact to the news. The outlook is uncertain, and there's a wide range of potential outcomes. Prior to the attacks in the Middle East, we expected the Fed to cut rates gradually later this year, and we expected long-term yields to hold in a range near 4% given sticky inflation and budget concerns. We were cautiously optimistic about taking some credit risk in moderation, but with risks rising, we have tempered that view.

With that outlook, we suggested investors favor intermediate-term maturities—generally meaning average maturities in the four- to 10-year range—to help mitigate reinvestment risk that short-term bonds offer and interest rate risk that longer-term bonds offer. Higher-rated bonds remain attractive, as the yields on Treasuries, agency mortgage-backed securities, and investment-grade corporate and municipal bonds generally offer yields that weren't available from 2009 until early 2022.

Investors willing to take a little credit risk can consider preferred securities, and only consider a high-yield bond allocation that's in line with your long-term goals and objectives. In other words, we don't suggest investors tactically consider taking on more risk with high-yield bonds today. Volatility may pick up over the short term, so investors should be prepared to ride out some ups and downs.

1 The Moody's investment-grade rating scale is Aaa, Aa, A, and Baa, and the sub-investment-grade scale is Ba, B, Caa, Ca, and C. Standard and Poor's investment-grade rating scale is AAA, AA, A, and BBB and the sub-investment-grade scale is BB, B, CCC, CC, and C. Ratings from AA to CCC may be modified by the addition of a plus (+) or minus (-) sign to show relative standing within the major rating categories. Fitch's investment-grade rating scale is AAA, AA, A, and BBB and the sub-investment-grade scale is BB, B, CCC, CC, and C.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

This material is intended for general informational and educational purposes only. This should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned are not suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decisions.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results.

Investing involves risk, including loss of principal.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

Investing in alternative investments is speculative, not suitable for all clients, and generally intended for experienced and sophisticated investors who are willing and able to bear the high economic risks of the investment. Investors should obtain and carefully read the related prospectus or offering memorandum, which will contain the information needed to help evaluate the potential investment and provide important disclosures regarding risks, fees and expenses.

Treasury Inflation Protected Securities (TIPS) are inflation-linked securities issued by the US Government whose principal value is adjusted periodically in accordance with the rise and fall in the inflation rate. Thus, the dividend amount payable is also impacted by variations in the inflation rate, as it is based upon the principal value of the bond. It may fluctuate up or down. Repayment at maturity is guaranteed by the US Government and may be adjusted for inflation to become the greater of the original face amount at issuance or that face amount plus an adjustment for inflation. Treasury Inflation-Protected Securities are guaranteed by the US Government, but inflation-protected bond funds do not provide such a guarantee.

Bank loans typically have below investment-grade credit ratings and may be subject to more credit risk, including the risk of nonpayment of principal or interest. Most bank loans have floating coupon rates that are tied to short-term reference rates like the Secured Overnight Financing Rate (SOFR), so substantial increases in interest rates may make it more difficult for issuers to service their debt and cause an increase in loan defaults. A rise in short-term references rates typically result in higher income payments for investors, however. Bank loans are typically secured by collateral posted by the issuer, or guarantees of its affiliates, the value of which may decline and be insufficient to cover repayment of the loan. Many loans are relatively illiquid or are subject to restrictions on resales, have delayed settlement periods, and may be difficult to value. Bank loans are also subject to maturity extension risk and prepayment risk.

Preferred securities are a type of hybrid investment that share characteristics of both stock and bonds. They are often callable, meaning the issuing company may redeem the security at a certain price after a certain date. Such call features, and the timing of a call, may affect the security’s yield. Preferred securities generally have lower credit ratings and a lower claim to assets than the issuer's individual bonds. Like bonds, prices of preferred securities tend to move inversely with interest rates, so their prices may fall during periods of rising interest rates. Investment value will fluctuate, and preferred securities, when sold before maturity, may be worth more or less than original cost. Preferred securities are subject to various other risks including changes in interest rates and credit quality, default risks, market valuations, liquidity, prepayments, early redemption, deferral risk, corporate events, tax ramifications, and other factors.

Tax-exempt bonds are not necessarily a suitable investment for all persons. Information related to a security's tax-exempt status (federal and in-state) is obtained from third parties, and Charles Schwab & Co., Inc. does not guarantee its accuracy. Tax-exempt income may be subject to the Alternative Minimum Tax (AMT). Capital appreciation from bond funds and discounted bonds may be subject to state or local taxes. Capital gains are not exempt from federal income tax.

Commodity-related products carry a high level of risk and are not suitable for all investors. Commodity-related products may be extremely volatile, may be illiquid, and can be significantly affected by underlying commodity prices, world events, import controls, worldwide competition, government regulations, and economic conditions.

Diversification and asset allocation strategies do not ensure a profit and do not protect against losses in declining markets. All names and market data shown are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

The S&P Business Development Company Index (S&P BDC) is a stock market index designed by S&P Dow Jones Indices to track the performance of leading BDC's that are publicly traded on major U.S. exchanges.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Investment and Insurance Products Are: Not FDIC Insured • Not Insured by Any Federal Government Agency • Not a Deposit or Other Obligation of, or Guaranteed by, the Bank or any of its Affiliates • Subject to Investment Risks, Including Possible Loss of Principal Amount Invested

The Charles Schwab Corporation provides a full range of brokerage, banking and financial advisory services through its operating subsidiaries. Its broker-dealer subsidiary, Charles Schwab & Co. Inc. (Member SIPC), and its affiliates offer investment services and products. Its banking subsidiary, Charles Schwab Bank, SSB (member FDIC and an Equal Housing Lender), provides deposit and lending services and products.

This site is designed for U.S. residents. Non-U.S. residents are subject to country-specific restrictions. Learn more about our services for non-U.S. residents, Charles Schwab Hong Kong clients, Charles Schwab U.K. clients.

© 2026 Charles Schwab & Co., Inc. All rights reserved. Member SIPC

© Charles Schwab

Read more commentaries by Charles Schwab