Workplace Benefits: It’s Not a Communication Gap. It’s a Translation Opportunity.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWorkplace benefits: It’s not a communication gap. It’s a translation opportunity.

For years, the retirement industry has framed the challenge the same way: Participants aren’t engaged enough. Employers need better communication. Advisors need to educate more.

But the latest Voice of the American Workplace research suggests something more nuanced—and actionable:

The partnership already exists. It just needs to be activated.

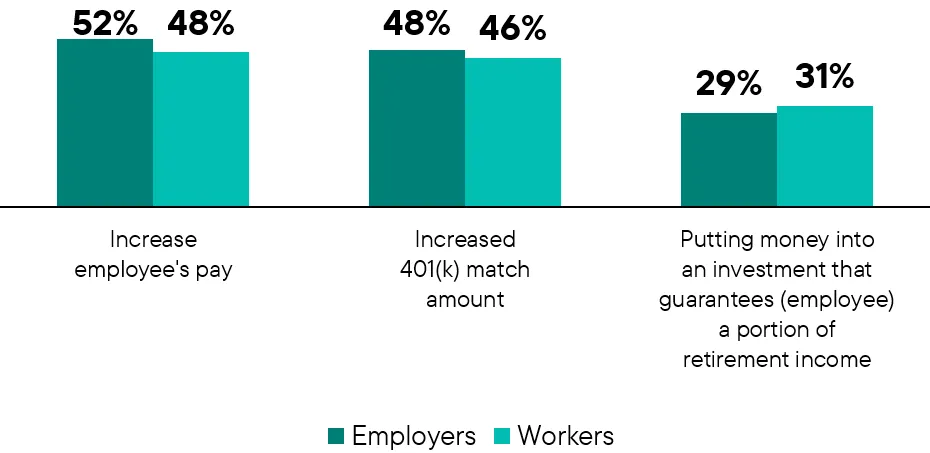

Employers and employees are not misaligned on retirement readiness. In fact, they’re remarkably aligned on what matters most:

- Competitive pay

- Strong 401(k) match

- Long-term financial security

At the same time, 93% of employers say retirement planning is a shared responsibility, not a handoff. And employees are signaling they’re open to that partnership—many rely on employer programs to guide financial decisions and value proactive support. This alignment creates the opportunity for defined contribution advisors to reinforce what is working well.

Exhibit 1: Employers and Workers Align on Financial Priorities

Similar Percentages of Each Group Agree on Pay, Match and Retirement Income

From information delivery to outcome design

Here’s the tension:

- 81% of workers say benefits communication is strong

- Yet more than half feel overwhelmed and unsure how to act

At the same time:

- 88% want benefits explained in plain language

- 73% of employers report employees asking the same questions repeatedly

This is not a failure of effort. It’s a failure of translation.

Participants aren’t asking for more information. They’re asking for clearer direction—what to do next, how to improve, and where they stand.

This is where high-value advisors can differentiate themselves.

The real market dynamic: financial stress + receptivity

Workers today are navigating real pressure:

- 80% turn to their employer for help with financial worries

- Retirement timelines are extending, and financial milestones are moving out

At the same time, engagement signals are strong:

- 91% want to learn more about financial benefits

- Many say they might not be saving at all without features like auto-enrollment

This combination—pressure + openness—creates one of the most compelling advisory opportunities in years.

Where advisors can lead (five calls to action)

If the relationship between employer and employee is already collaborative, the advisor’s role becomes clear:

Turn alignment into action.

Here are five ways to do exactly that:

1. Simplify the path to the match

Focus your participant engagement on one essential behavior:

- Contribute enough to capture the full employer match

The research is clear: Small actions compound. And employees respond best when the message is simple, direct and actionable—not educational for education’s sake.

2. Reframe communication around “next best step”

Move away from:

- Plan features

- Investment menus

- Technical education

Move toward:

- “Here’s what to do this quarter”

- “You’re on track / off track”

- “Increase by 1% today”

Advisors who translate complexity into clear, repeatable actions will drive measurable engagement.

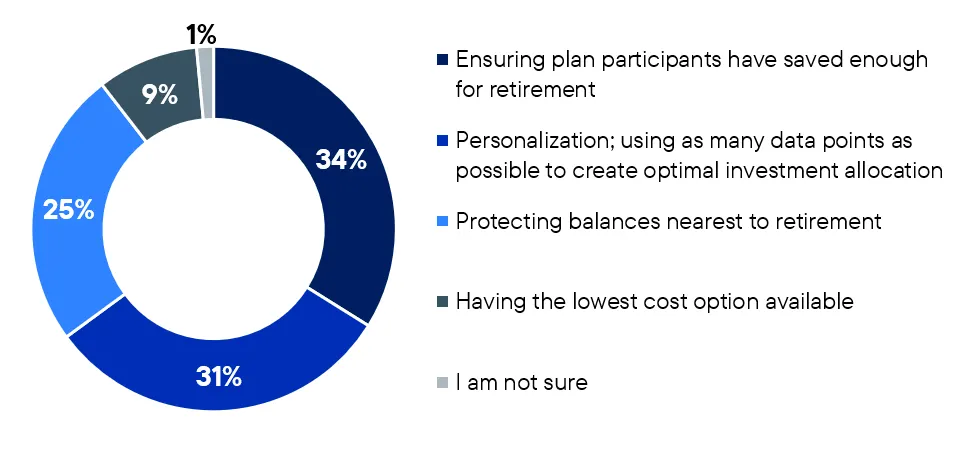

3. Conduct a QDIA1 review with purpose

The data shows:

- Retirement readiness and personalization are nearly equal priorities in QDIA selection

This is a critical moment to revisit:

- Glidepath alignment with participant behavior

- Balance between growth, protection and personalization

- Role of guaranteed income or evolving target date fund (TDF) structures

Call to action:

Re-engage sponsors in a formal QDIA review focused on outcomes—not just benchmarking. Ask “is the average participant using this QDIA on track to meaningfully replace their income?”

Exhibit 2: The Prominence of TDFs as QDIA Heightens the Need for a Defined TDF Selection Process

Retirement readiness (34%) and personalization (31%) are nearly equal priorities for plan decision makers.

![]()

4. Reassess capital preservation in a new rate environment

-

75% of employers are re-evaluating their capital preservation option

- 68% expect to make changes in the next 12 months

With interest rates and participant behavior shifting, capital preservation is not a “set it and forget it” decision.

Call to action:

Lead a capital preservation review conversation with plan sponsors:

- Stable value vs. money market

- Participant utilization trends

- Role in near-retirement confidence

This is an underutilized but highly visible area to deliver value.

5. Connect today’s financial stress to tomorrow’s retirement outcomes

Participants are prioritizing:

- Emergency savings

- Job security

- Near-term financial stability

Ignoring this reality weakens retirement engagement.

Call to action:

Help sponsors integrate:

- Financial wellness tools

- Emergency savings strategies

- Behavioral nudges

Position the retirement plan not as a silo, but as part of a broader financial ecosystem.

A partnership worth building on

The most encouraging takeaway from this year’s research is not the challenges—it’s the foundation.

Employees trust their employers.

Employers are committed to supporting employees.

Both are aligned on financial security.

This level of alignment is rare—and valuable.

The advisors who win in this environment will not be those who provide more information.

They will be those who translate alignment into action, complexity into clarity and plans into outcomes.

How Franklin Templeton can help

At Franklin Templeton, we see this moment as an opportunity to support advisors in three ways:

- Translating research into practical plan design insights

- Delivering solutions across target date, capital preservation and income

- Supporting advisors in building stronger employer-participant engagement models

Because the future of retirement success isn’t about choosing between employer or employee responsibility.

It’s about helping both sides succeed—together.

Please visit Voice of the American Workplace Survey to access this year’s survey results.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Endnote

1A Qualified Default Investment Alternative (QDIA) is a default investment option in a workplace retirement plan, in which money is invested if plan participants do not choose a different option.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Any information, statement or opinion set forth herein is general in nature, is not directed to or based on the financial situation or needs of any particular investor, and does not constitute, and should not be construed as investment advice, forecast of future events, a guarantee of future results, or a recommendation with respect to any particular security or investment strategy or type of retirement account. Investors seeking financial advice regarding the appropriateness of investing in any securities or investment strategies should consult their financial professional.

Franklin Templeton, its affiliated companies, and its employees are not in the business of providing tax or legal advice to taxpayers. These materials and any tax-related statements are not intended or written to be used, and cannot be used or relied upon by any such taxpayer for the purpose of avoiding tax penalties or complying with any applicable tax laws or regulations. Tax-related statements, if any, may have been written in connection with the “promotion or marketing” of the transaction(s) or matter(s) addressed by these materials, to the extent allowed by applicable law. Any such taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor.

The allocation of assets among different strategies, asset classes and investments may not prove beneficial or produce the desired results.

Equity securities are subject to price fluctuation and possible loss of principal.

Funds that invest in bonds are subject to certain risks including interest-rate risk, credit risk, and inflation risk. As interest rates rise, the prices of bonds fall. Long-term bonds are more exposed to interest-rate risk than short-term bonds. Unlike bonds, bond funds have ongoing fees and expenses.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG” as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe's website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All