LPL Research examines Warsh’s evolving Fed approach, infrastructure-led growth, and the impact of China demand on oil prices.

A hawkish debut. At his first Federal Open Market Committee (FOMC) meeting, Chair Kevin Warsh paired a hawkish, minimalist tone — tersely emphasizing price stability — with the launch of five task forces to review key aspects of Federal Reserve (Fed) policy. Many Fed governors want to follow the Bank of Japan’s lead and hike rates in the near term.

Uncertainty in projections. While officials’ projections show a split on future rate hikes and a higher path for rates, alongside elevated inflation forecasts, uncertainty remains high, underscored by Warsh’s decision not to submit projections. Importantly, with inflation seen as partly supply-driven, the Fed could turn less hawkish if geopolitical tensions ease.

Constructive ambiguity and growth. Overall, the Fed appears to be shifting back toward “constructive ambiguity,” with the outlook hinging on Middle East developments and a steady, near-trend growth backdrop supported by investment and productivity gains. We show that the infrastructure buildout is supporting growth while soft Chinese demand is suppressing oil prices.

To understand the drivers underneath the outlook, reference the newly-released Economic Navigator.

Did He Just Provide the Forward Guidance He Doesn’t Like?

Kevin Warsh, the new chairman of the FOMC, has long been critical of forward guidance, which is the Fed’s practice of explicitly signaling the future path of interest rates (e.g., “rates will stay low for an extended period” or publishing a projected path for policy rates). His concern is that the guidance could give the impression that policymakers might have a high degree of confidence about the future path of the economy and rates. Warsh tends to view this as misleading since macroeconomic conditions, especially inflation shocks, are inherently uncertain, so locking in a path risks being wrong.

If the Fed preps investors for a particular path and conditions change, backing away can damage credibility. Warsh prefers keeping his options open without “pre-committing” to a trajectory.

Heavy forward guidance encourages markets to anchor too tightly to Fed signals instead of underlying data, which can distort financial conditions and create volatility when guidance shifts.

Even though Warsh favors minimalist, “constructive ambiguity”-style communication, releasing a dot plot within the Summary of Economic Projections (SEP) still functions as forward guidance. As of now, the updated dots show a higher median rate (and a split committee) that tells investors rates may need to rise from here or stay higher for longer. Markets interpreted this as directional guidance, which explains the negative reaction in both the equity and bond markets after the meeting.

Read more: Federal Reserve Press Conference: Lots to Unpack, but Inflation Is Not a Choice

Moving Toward a More Implicit Guidance

So, to answer the initial question, Warsh may have given us the version of forward guidance he prefers. Warsh rejects strong, explicit forward guidance, but he is still using a lighter, more conditional version via projections. The shift is toward guidance with less verbal commitment, more data-dependency, and built-in ambiguity.

The Shake-Up: Five New Task Forces

Chair Kevin Warsh announced five task forces aimed at modernizing key pillars of Fed policymaking — covering data collection and usage, AI and productivity, communications (including a potential overhaul of the Summary of Economic Projections), the inflation framework, and balance sheet strategy — reflecting a broad effort to address both structural and credibility challenges facing the institution. These task forces are expected to be composed of a mix of Federal Reserve Board staff, regional Fed bank economists, and outside experts from academia, technology, and financial markets, signaling a more open, cross-disciplinary approach to policy design. This could yield very good fruit. By combining internal institutional knowledge with external perspectives, Warsh appears to be seeking both technical improvements (e.g., better measurement of productivity and inflation dynamics) and a retooling of how the Fed communicates and implements policy.

Despite initially creating some unwelcome volatility, we think these five committees may introduce some real improvements. Some of the methodologies on both data collection and analysis could be improved with the help of modern technologies, and the shake-up may nudge the Fed, our country’s third attempt at central banking, into a more credible and helpful institution.

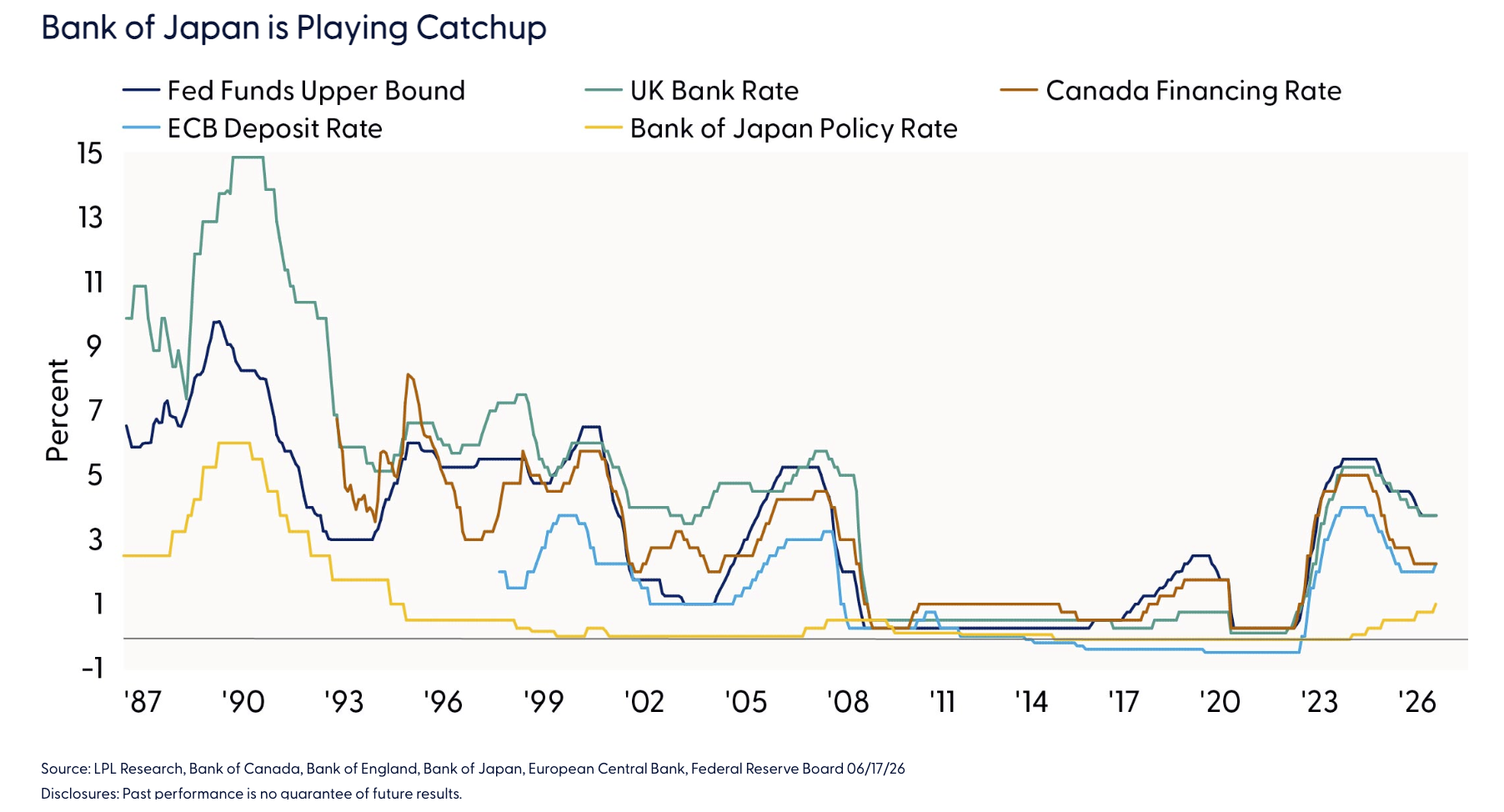

Central Bank Rates Are Slowly Converging

Last week’s attention was mostly on the Fed and its upwardly revised dot plot, but other central banks deserve some attention. The Bank of Japan’s (BOJ) recent decision to hike rates reflects a notable shift after years of ultra‑easy policy, driven by stronger domestic inflation dynamics and rising wage growth, which signal that Japan is finally moving away from persistent deflation. Policymakers are increasingly worried that inflation is becoming more persistent, particularly as firms pass through higher costs and wages begin to support demand, warranting the hike. We expect global central bank policy rates will begin to converge, as the Middle East conflict is creating a shared, supply-driven inflation shock — primarily through higher energy and shipping costs — that is affecting both advanced and emerging economies.

Unlike prior cycles where inflation pressures diverged across regions, this shock is more synchronized, pushing central banks — even those at very different starting points like the BOJ and the Fed — toward a closer policy stance. As long as geopolitical tensions

What Happens After the Iran War Ends?

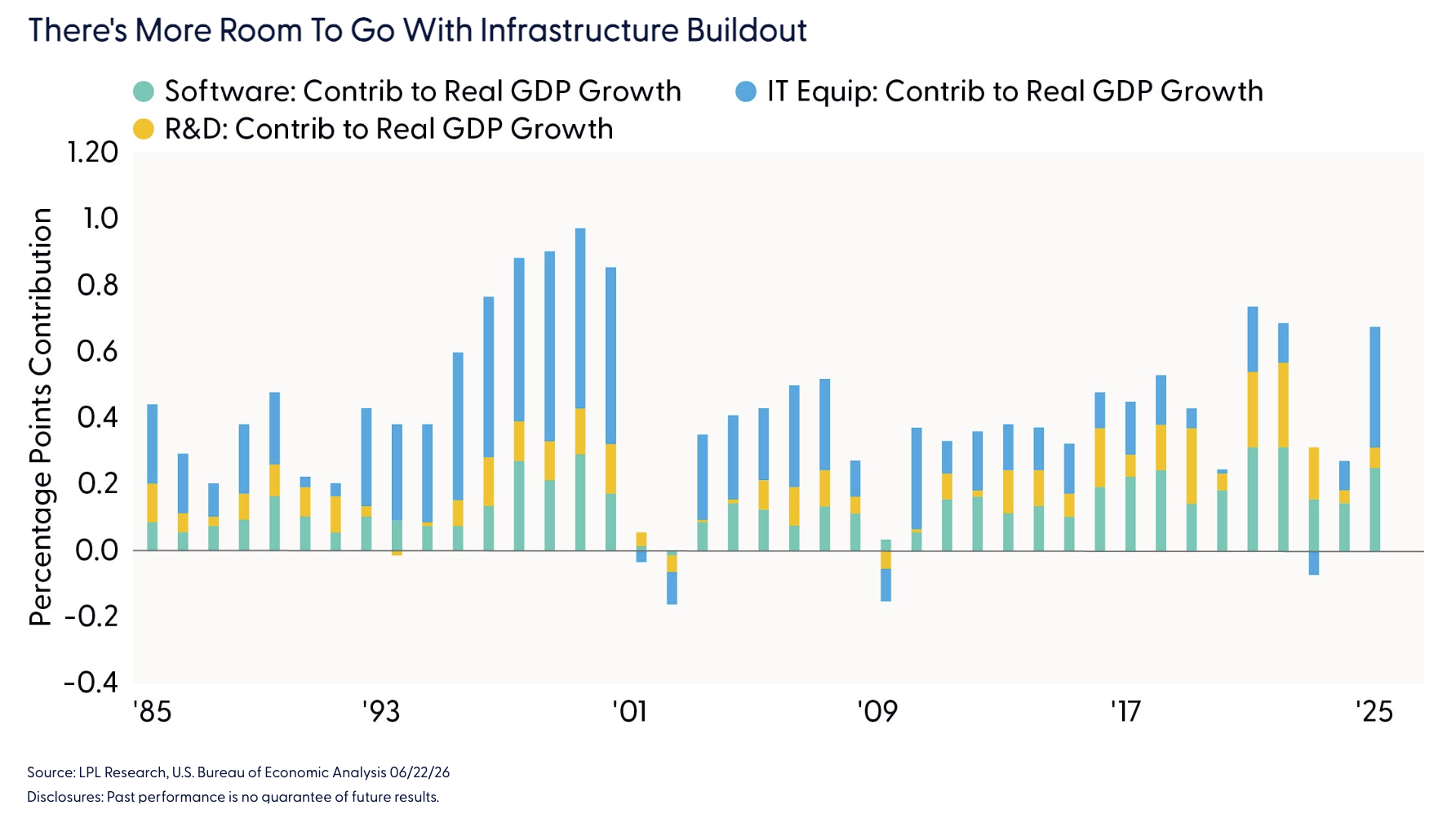

After geopolitical tensions ease, we expect the Fed to examine the underlying drivers of growth more closely, with a particular focus on whether business investment — especially in AI-related infrastructure — is generating sustained momentum rather than a temporary cycle boost. Capital spending tied to data centers, semiconductors, and digital infrastructure has emerged as a key support for productivity and potential output, suggesting growth could remain near trend even amid tighter financial conditions. If these investments translate into measurable productivity gains, the Fed may view this expansion as more durable and less inflationary, shaping a more balanced policy response over time. We know from earlier speeches that Chair Warsh believed AI would boost productivity and help relieve inflation pressures.

Will Oil Prices Return to Pre-War Levels? It Depends on China’s Economic Growth

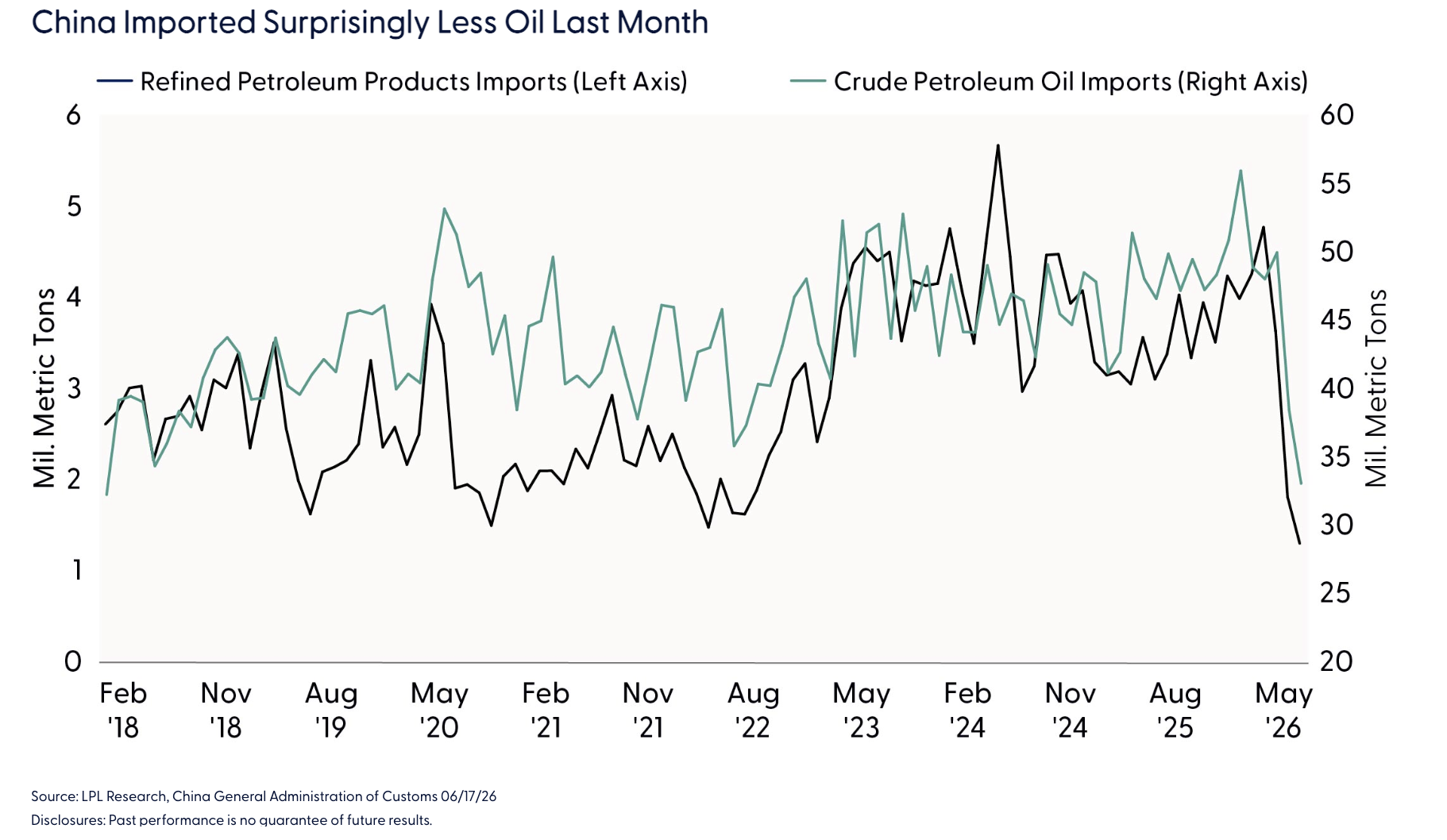

One of the key questions for investment professionals is whether oil prices will return to pre-war levels once the Middle East crisis is resolved. At the same time, many are asking why oil prices are not higher, especially since the latest U.S.–Iran deal recently pushed crude to its lowest level since the initial attack. More than 100 days after the war in Iran disrupted the Strait of Hormuz, oil prices remain surprisingly contained, and one such reason could be China’s sharp pullback from the crude market. According to Vortexa data, Chinese crude imports by tanker fell to 6.7 million barrels a day last month, nearly 40% below the 2025 average.[1] That reduction — roughly 4 million barrels a day — is enormous, equal to the combined oil consumption of Germany and France. This could be the central factor keeping prices below $100 a barrel, as Beijing has somehow slashed imports without obvious economic damage other than a slowdown in year-over-year gross domestic product (GDP) from 5% in Q1 to 4.6% in Q2.

Chinese retrenchment has helped offset what would normally be a major supply shock. Even with the Strait of Hormuz effectively closed, oil has continued to leave the Gulf through Saudi and UAE pipelines and tanker shuttle operations. At the same time, the market entered the conflict with a sizable surplus, strategic reserves are being released at a record pace, and global refinery runs have fallen as demand weakens, especially in petrochemicals.

China is the key variable. Some price-suppressing forces, such as emergency stock releases and inventory drawdowns, are temporary. The central question is how long Beijing can continue importing so little crude. If Chinese buying returns before supply risks ease, oil’s next move could look very different.

Other factors have also dampened the oil price response. Refineries are more flexible than in past crises, allowing them to adjust crude slates and product output. Production growth in the Americas, including Brazil, Guyana, the U.S., and China, has added to supply. Meanwhile, traders have increasingly hedged geopolitical risk through options rather than physical oil purchases, and better satellite imagery and tanker tracking have reduced the fog of war.

But Do We Really Understand Tanker Activity?

It depends on how accurately we can track vessels.

The familiar model of maritime monitoring, the Automatic Identification System (AIS) signal, breaks down when geopolitics enter the picture. In places such as the Strait of Hormuz and the Red Sea, vessel movements help us assess crude flows and potential market disruptions. But that evidence can be incomplete, delayed, spoofed, or deliberately obscured.

The stakes are especially high in the Strait of Hormuz, one of the world’s most important oil chokepoints. A tanker tracked through the strait may appear to be a simple line on a map, but in a crisis it becomes a market-sensitive claim about whether oil is moving, whether a cargo is stalled, whether a sanctioned ship transited, or whether traders should price in disruption.

Several categories of maritime risk now shape the operating environment. “Dark vessels” could disappear from normal visibility to conceal port calls, route changes, or ship-to-ship transfers. “Spoofing” involves false position signals that can make a vessel appear somewhere it is not. “Shadow fleets” describe opaque networks of vessels that move sanctioned commodities.

In contested waters, the vessel track is only valuable if it is to be trusted. For energy markets, false signals can quickly become false narratives about supply, disruption, or sanctions risk.

Concluding Thoughts

Ultimately, whether oil prices return to pre-war levels depends on both the formal resolution of the Middle East crisis and the durability of China’s demand slowdown. China’s unusually steep reduction in crude imports, as shown in the “China Imported Surprisingly Less Oil Last Month” chart, has absorbed a large share of the supply shock, but that cushion may prove temporary if economic activity reaccelerates, inventories are rebuilt, or Beijing resumes normal buying patterns. At the same time, today’s oil market is pricing not only barrels, but also information quality. Tanker flows, shadow-fleet activity, spoofed signals, and dark vessels can all distort the narrative around supply risk. For now, surplus inventories, strategic reserve releases, flexible refineries, hopeful political deals, and weaker Chinese demand have kept crude prices contained. But if China’s growth strengthens before geopolitical risks fully fade, and if vessel-tracking data becomes harder to trust, the market could quickly shift from complacency back toward scarcity pricing.

Asset Allocation Insights

The LPL Research Strategic and Tactical Asset Allocation Committee (STAAC) maintains its recommendation for a tactical equity overweight and fixed income underweight. While maintaining our equity and U.S. equity overweights, the Committee favors neutral style exposure because of stretched market positioning and technical indicators following the recent growth-led rally. As such, this view is expressed via a defensive factor tilt given our expectation for bouts of volatility until the macro backdrop begins to improve as the situation in the Strait of Hormuz eventually plays out to a resolution, allowing markets to refocus on a broadly healthy fundamental landscape.

[1] Record Low Inflows | Vortexa

Jeffrey J. Roach, Chief Economist, LPL Financial

Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

All investing involves risk, including possible loss of principal.

US Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

The Bloomberg U.S. Economic Surprise Index measures the degree to which U.S. economic data releases surprise to the upside or downside relative to market expectations.

All index data from FactSet or Bloomberg.

This research material has been prepared by LPL Financial LLC.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by LPL Financial