Key Takeaways

-

The planning window closes before the transaction: Many of the most valuable strategies available to founders, including equity gifting, trust structures, and QSBS qualification, become harder to execute once a sale or funding event is underway.

-

Concentration is the defining risk: Most founder wealth is tied to one company, one industry, and one exit outcome, which creates planning needs that a standard investment portfolio approach cannot address.

-

Coordination matters more than any single advisor: Founders with a CPA, attorney, and investment account but no one connecting the pieces are leaving the most valuable planning work undone.

Founders tend to think of hiring a wealth advisor as something for after the sale closes. After the wire hits. That instinct makes sense in the early years, but it creates a real problem.

The most consequential decisions a founder will face, equity gifting before valuations increase, trust structures timed ahead of a sale, QSBS qualification built while eligibility still exists, all must be decided before liquidity. Once the transaction closes, much of what was available earlier is simply gone.

This article covers when a wealth advisor adds the most value, what that advisor should do, what qualities matter most, and when a founder may not need one yet.

Financial Planning for Founders Starts Before the Portfolio Exists

Founder wealth requires a different kind of planning than what most advisory frameworks are designed to handle.

The Wealth Is Concentrated, Illiquid, and Hard to Plan Around

A founder may carry significant net worth on paper while living on a modest salary. Their largest asset, private company equity, is difficult to value, impossible to sell outside of a structured liquidity event, and tied to one company, one industry, and one exit outcome. Standard asset allocation advice fails here because the largest asset is outside the portfolio entirely. That concentration often built the wealth, but the same strategy rarely protects it.

Early Planning Is About Decisions, Not Portfolios

Pre-liquidity founders do not need an advisor to manage a large portfolio. What they need is help with the decisions that shape how wealth eventually arrives: equity structure, option timing, estate planning before valuations increase, and tax coordination. The advisor’s role is less about selecting funds and more about ensuring current decisions do not close off options that will matter later.

Read more: The Consumer Sentiment Disconnect From Economic Reality

Pre-Liquidity Planning for Founders: The Moments That Matter Most

Several situations reliably create planning urgency before a liquidity event. Founders who engage early have more options than those who engage during them.

Before a Major Funding Round or Valuation Increase

Rising valuations create gifting and estate planning urgency that many founders do not recognize until it has passed. An equity interest transferred at a $5 million valuation carries far less gift and estate tax exposure than the same interest transferred after a Series B pushes that value to $40 million. This is when 83(b) elections, option timing, and ownership structure decisions tend to be most consequential, and the right choices require someone looking at the full picture.

Before Exercising Stock Options or Making Major Equity Decisions

ISOs, NSOs, restricted stock, and founder shares each carry distinct tax treatment, and the differences matter at scale. An ISO exercise may trigger alternative minimum tax; an NSO creates ordinary income at the spread. A large exercise with no corresponding liquidity can leave a founder with an unexpected tax bill and no cash to pay it. A wealth advisor working alongside a CPA can model the full cost before the decision is made rather than after.

Before a Tender Offer, Secondary Sale, or Partial Liquidity Event

A tender offer is often the first opportunity to convert paper wealth into actual cash. Three planning questions consistently surface beforehand:

-

Federal vs. State / Pennsylvania QSBS treatment: Pennsylvania does not conform to the federal Section 1202 exclusion, meaning gains fully excluded at the federal level may still be assessed under Pennsylvania’s personal income tax, materially changing the after-tax outcome.

-

Estimated tax obligations: Partial liquidity events can trigger significant estimated payment requirements that founders without prior planning frequently underestimate or miss entirely.

-

The diversification trade-off: Selling at less than the expected future value may still be the correct decision depending on the rest of the balance sheet.

Before Selling the Company or Entering M&A Discussions

The period before a sale is the highest-value planning window a founder will encounter, and several strategies, including QSBS eligibility reviews, trust formations, and charitable transfers, must be completed before the deal takes on binding form. A pre-sale review should address:

-

QSBS eligibility review: Confirm the holding period and documentation requirements for Section 1202 treatment have been met, including any stacking or trust strategies still available.

-

Charitable planning: Evaluate donor-advised fund contributions or charitable remainder trusts funded with pre-sale stock, where the tax benefit is greatest before the sale closes.

-

Estate plan updates: Ensure documents reflect the company’s actual value, not the plan drafted when the business was worth a fraction of today’s.

-

Deal structure analysis: Model installment sales, earnouts, or other structure options that may reduce the immediate tax burden or manage liquidity timing.

-

Pennsylvania-specific tax exposure: Account for the state’s non-conformity with federal QSBS exclusions and any PA income tax obligations the federal analysis may not capture.

Our QSBS stacking and trust planning case study covers how this coordinated process works in practice.

Before an IPO or Lockup Expiration

An IPO replaces illiquid concentration with publicly traded concentration, but lockup periods often prevent selling freely while the price moves. 10b5-1 plans, diversification timelines, and estimated tax planning all require preparation before the IPO date, not after the lockup expires.

After the Exit: Still Valuable, but Different

Engaging a wealth advisor after a liquidity event is not too late, but the work shifts from designing outcomes to executing them: reserving taxes, building an investment policy, and sequencing diversification deliberately rather than reactively. We cover what that process looks like in our guide to what happens after you sell your business.

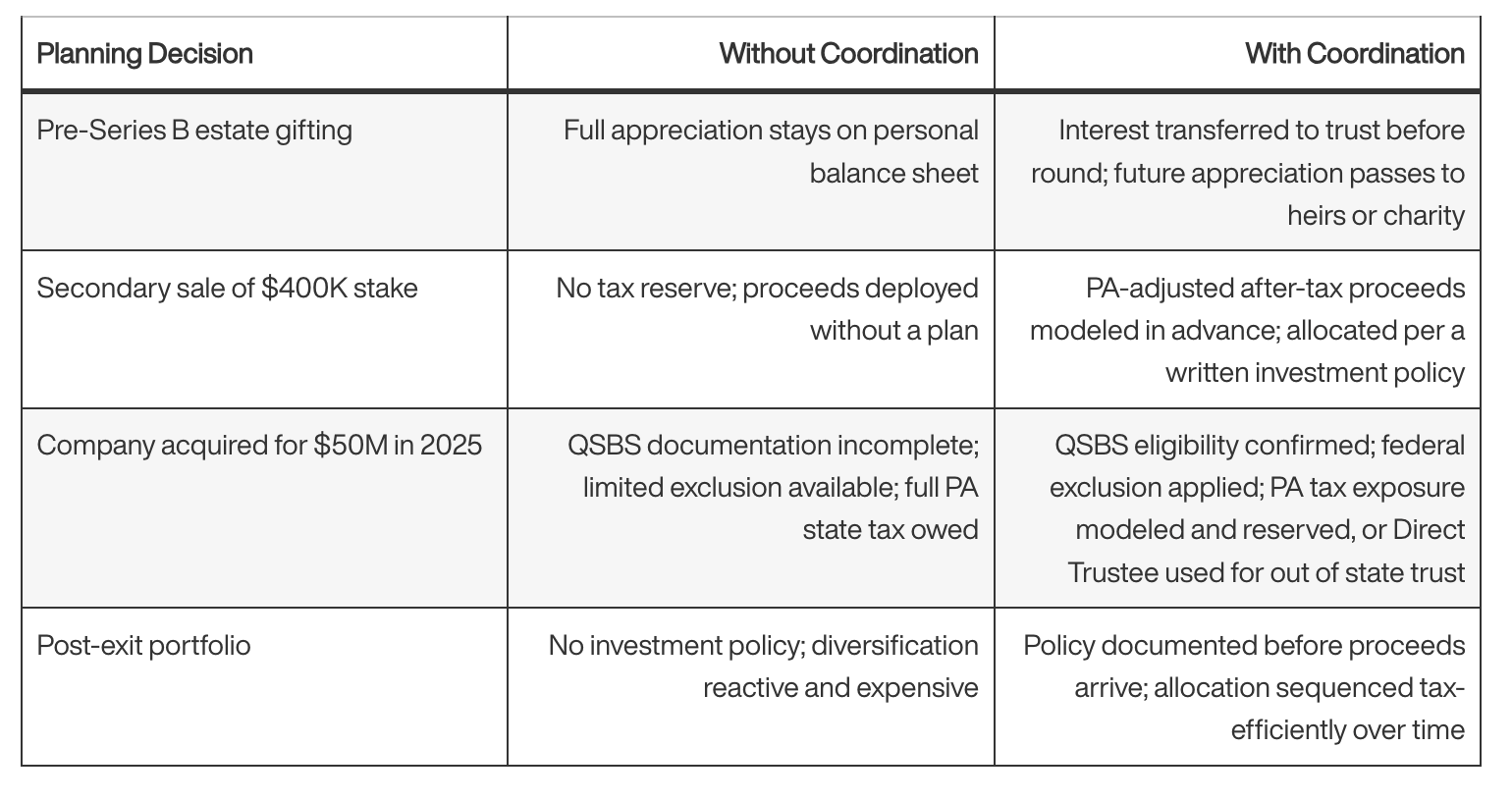

What Coordinated Wealth Planning Actually Looks Like for a Founder

Consider a Pittsburgh technology founder whose company completes a Series B at a $40 million valuation in 2024, giving them roughly $14 million in paper equity with no liquidity. Our wealth management case studies offer additional examples of these decisions in practice.

The difference is almost never about investment selection. It is almost always about the decisions made, or not made, before the transaction.

What a Wealth Advisor Should Help a Founder Do

The right advisor for a founder is not simply an investment manager with a few business owner clients. The scope is different, and the advisor should demonstrate that clearly. Our approach to wealth management and advisory for founders reflects this broader mandate.

A founder-focused wealth advisor should be capable of:

-

Modeling multiple exit scenarios: Building after-tax projections across different transaction values, structures, and timing so the founder understands which outcomes are genuinely life-changing and which are merely attractive.

-

Coordinating tax planning before the event: Reviewing QSBS eligibility, modeling capital gains and state tax exposure, identifying charitable opportunities, and sequencing decisions before the transaction closes.

-

Building a diversification strategy around illiquid equity: Addressing staged selling, liquidity targets, and portfolio construction in a way that accounts for the full balance sheet, not just investable assets already in an account.

-

Integrating estate planning with equity ownership: Ensuring trusts, gifting strategies, and ownership structures reflect the founder’s current net worth and family goals, not documents drafted years earlier.

-

Creating a post-exit investment and cash flow plan: Segmenting proceeds between taxes, reserves, lifestyle capital, and long-term wealth before the wire hits.

None of this replaces the CPA or the M&A attorney. It connects them, and it keeps the founder from making consequential decisions in each silo without seeing how they affect the others.

Signs a Founder Has Outgrown Basic Financial Advice

Several patterns consistently signal that a robo-platform, a generalist CPA, or a single brokerage account is no longer adequate:

-

Equity dominates the personal balance sheet: When private company stock is the most significant asset but the planning conversation is still only about liquid investments, the coverage has a meaningful gap.

-

Tax decisions span multiple years: When the question shifts from this April’s return to structuring the next three years, annual filing services are the wrong tool.

-

A liquidity event is approaching: Any tender offer, secondary sale, acquisition, or IPO creates planning decisions that generalist advisors rarely have the experience to coordinate.

-

Estate documents are outdated: If company value has grown substantially since the last estate planning review, the mismatch between actual wealth and documented intentions is a compounding risk.

-

No one coordinates the full picture: A CPA who files, an attorney who drafts, and a brokerage that invests are not the same as integrated planning, and the gaps between those silos are where the most expensive mistakes happen.

When several of these apply at once, that gap tends to be both large and urgent.

What to Look for in a Financial Advisor for Startup Founders

Not every advisor who works with business owners is equipped for founder-level complexity. Three qualities matter most:

-

Founder-specific experience: The advisor should have genuine experience with private company equity, liquidity events, and concentrated wealth, and be comfortable coordinating with CPAs, M&A attorneys, and estate attorneys. General business owner experience is not the same as working through an acquisition alongside deal counsel.

-

Tax and estate awareness: For Pennsylvania founders, this means understanding the state inheritance tax, the absence of a separate Pennsylvania estate tax, and how Pennsylvania’s QSBS treatment diverges from federal rules. Succession planning questions often surface alongside these when family members are involved in the business.

-

Investment discipline after liquidity: The advisor should bring a written investment policy, a sequenced liquidation plan, a tax-aware allocation, and a clear framework for evaluating private market investment opportunities rather than defaulting to whatever seems most compelling.

These qualities matter more than credentials, and any strong candidate should demonstrate them with specific examples.

When a Founder May Not Need a Wealth Advisor Yet

Not every founder at every stage needs a dedicated wealth advisor. Three conditions suggest the immediate need may not yet be there:

-

Early-stage speculative equity: If the company is pre-revenue or the equity has limited assigned value, planning needs are primarily operational and legal rather than advisory in the wealth management sense.

-

Simple personal finances: If the founder has no material equity decisions, no near-term transaction activity, and no family complexity, a generalist CPA or financial planner may be sufficient for now.

-

Immediate need is filing or compliance: Basic tax preparation, legal entity formation, or budgeting support do not require the level of coordination that founder wealth planning provides.

The threshold is not a net worth number. It is complexity. When equity, taxes, estate planning, and liquidity decisions begin to interact, planning needs more coordination, and in our experience with Pittsburgh and Pennsylvania founders, that inflection point arrives earlier than most expect.

Frequently Asked Questions

When is the right time for a startup founder to hire a wealth advisor?

The right time is almost always before a significant liquidity event, option exercise, or valuation milestone, not after. Many of the most valuable planning strategies, including trust formation, equity gifting, QSBS qualification, and charitable planning, are harder to implement once a transaction is underway or complete. The planning work that matters most happens while the company is still private.

Does a founder need a wealth advisor if they already have a CPA and an attorney?

A CPA and attorney are necessary but not sufficient for founder-level financial planning. Neither is typically responsible for integrating investment policy, estate coordination, tax modeling, liquidity planning, and post-exit portfolio design into one coordinated plan. A wealth advisor provides that coordination layer, and the gap between having it and not having it is where most of the planning value gets left behind.

What is the difference between a financial advisor and a wealth advisor for founders?

The distinction is less about title and more about scope. A financial advisor often focuses on investment management or retirement savings. A wealth advisor working with founders covers a broader set of decisions: private equity planning, tax strategy, estate coordination, liquidity event preparation, and portfolio construction after a sale. Founders should prioritize demonstrated experience with founder-specific situations over general investment management credentials.

How does Pennsylvania tax treatment affect a founder’s wealth planning?

Pennsylvania does not follow the federal Section 1202 QSBS exclusion, meaning founders may owe state income tax on gains entirely excluded at the federal level. Pennsylvania also imposes an inheritance tax triggered by the decedent’s state of residence rather than a separate estate tax, which affects how family transfers and trust structures should be designed. These differences make early, coordinated planning especially important for Pennsylvania residents.

What should a founder look for when evaluating a wealth advisor?

Founders should look for demonstrated experience with private company equity, concentrated wealth, and liquidity event planning, plus the ability to coordinate with CPAs, M&A attorneys, and estate attorneys. Founder-specific experience matters more than credentials. The advisor should be able to explain concretely what they do differently for a founder, and that explanation should reflect actual experience rather than a marketing pitch.

Please read important disclosures here.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Defiant Capital Group

Read more commentaries by Defiant Capital Group