Key takeaways

-

Redemption pressure isn’t easing. Withdrawal requests from investors in non-traded business development companies (BDCs) continue to exceed available liquidity, and unlike in the 2023 episode in real estate investment trusts (REITs), BDC net asset values (NAVs) hinge directly on borrowers’ ability to service debt.

-

A confidence gap is opening between managers. NAVs increasingly reflect manager-specific marks rather than a shared clearing price, widening dispersion and rewarding sponsors with stronger asset quality. Valuations could eventually converge toward market-clearing levels through NAV markdowns, wider secondary discounts, or realized losses.

-

Private credit isn’t a monolith. Stress is concentrated in direct lending’s corporate exposure, while asset-based finance offers collateral-backed profiles that can diversify portfolios.

The feedback loop between stale and often dispersed price marks and fund flows remains firmly in place. Redemption pressure in non-traded business development companies (BDCs), funds that invest in small and midsize private U.S. businesses, shows little sign of easing. Withdrawal requests from investors continue to exceed available liquidity, leaving managers reliant on caps and prorations. (In prorated redemptions, investors receive a fraction of their requested liquidity.) The basic dynamic is familiar: Redemption requests are fulfilled when inflows are sufficient to meet outflows, but once that balance breaks, liquidity has to be rationed.

The comparison with the non-traded real estate investment trust (REIT) episode of 2023 is useful, though not perfect. For private REITs, valuations can be supported by appraisals, long-term leases, rental income, cap-rate assumptions, and property-level fundamentals. Those marks can still be stale or optimistic, but the valuation process often moves more gradually.

For non-traded BDCs, the assets are mostly private loans to companies. The key question is more direct: Can the borrower keep paying interest and principal? If earnings weaken, interest coverage deteriorates, or the loan becomes nonaccrual (meaning no payment has been made for some period of time and the lender is no longer accruing interest), then the pressure can show up more quickly in income, marks, and net asset values (NAVs).

The 2023 episode showed that private REITs can withstand redemption cycles, provided asset quality, return stability, and investor confidence hold up. For non-traded BDCs, the task may be more challenging because private credit portfolios offer less scope to defer valuation adjustments and are more directly exposed to borrowers’ debt-service capacity. That puts greater weight on realized asset performance – and ultimately portfolio quality – from here.

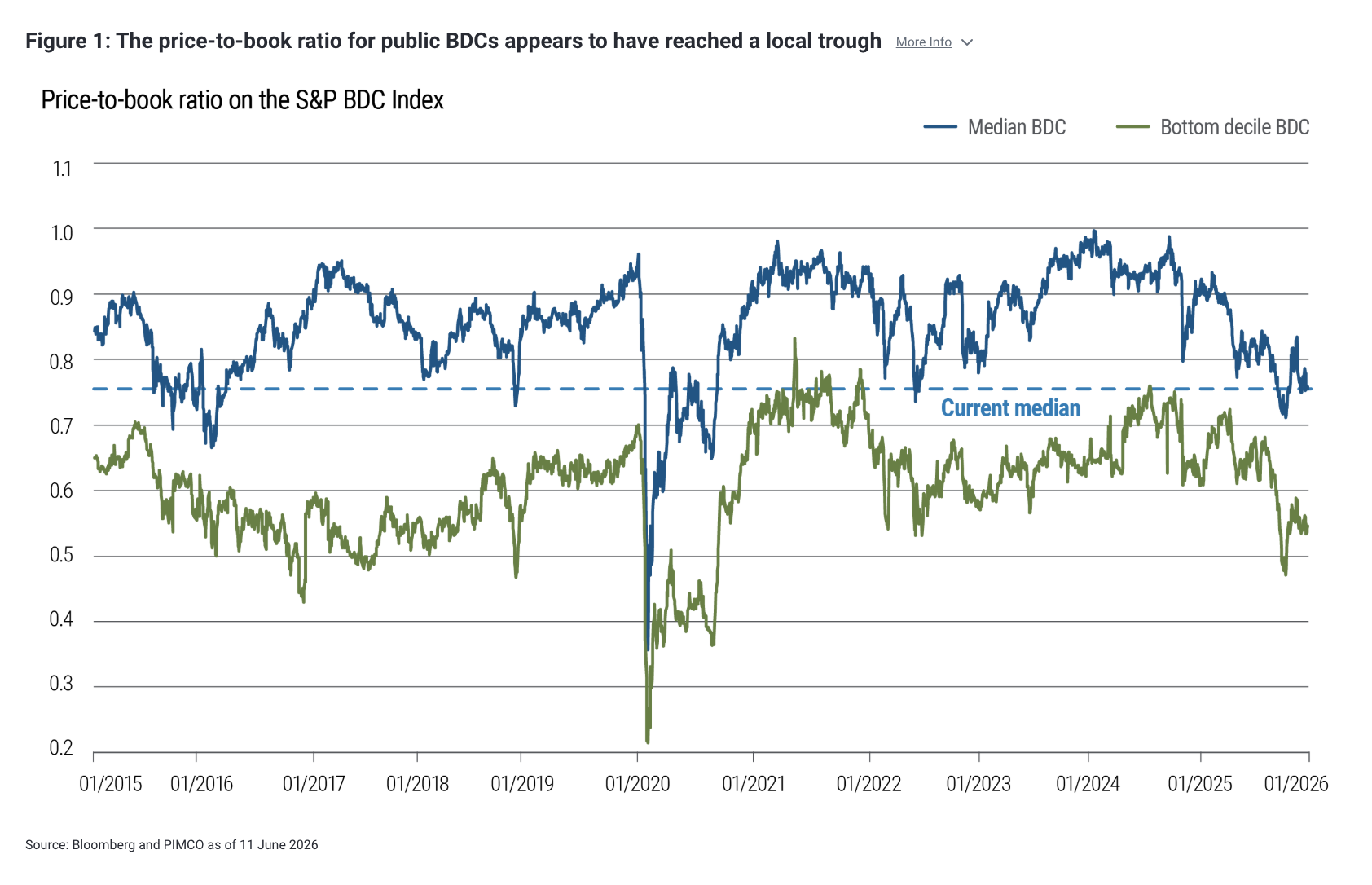

On the public side, the picture has remained more stable. The median price-to-book ratio appears to have reached a local trough, suggesting the pace of derating – or lowering internal valuations – may be slowing (see Figure 1). But discounts remain wide, dispersion has increased, and the weakest names have continued to cheapen. The market is therefore no longer applying a simple macro discount. It is differentiating more sharply across managers, asset quality, and confidence in reported marks.

Read more: The Strait is Open. What's Next for Markets?

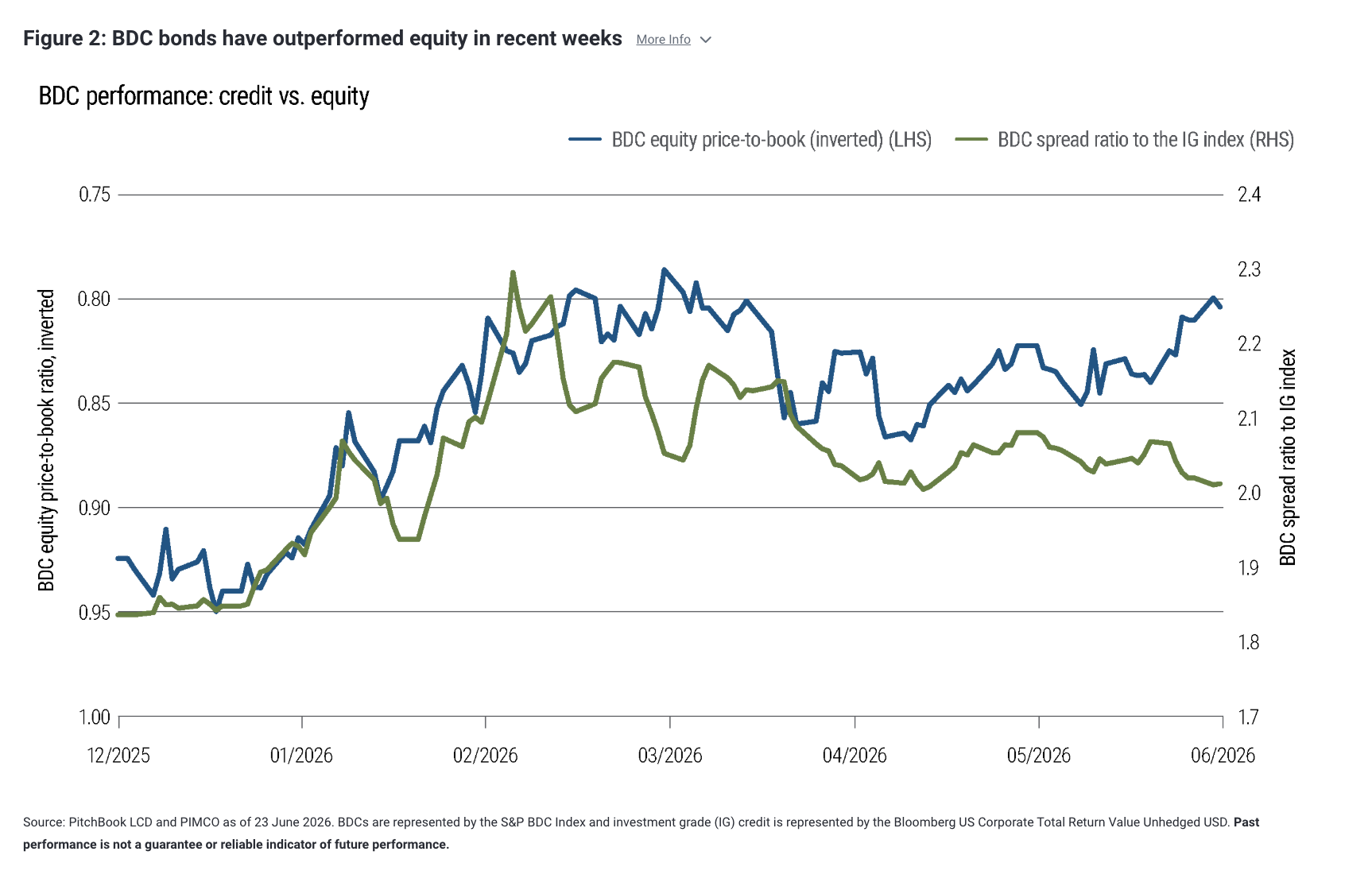

The capital structure performance of BDCs has also been telling. In our 27 April edition of The Credit Market Lens, we argued that the strong co-movement between BDC public equities and bonds was likely to weaken, with bonds outperforming in relative terms. That has now played out (see Figure 2). Equity investors have remained focused on the credibility of reported NAVs, while credit investors have been more willing to separate valuation uncertainty from default and recovery risk.

To be clear, bonds are not immune to those concerns, but the transmission channel is less direct. Much of the repricing has already occurred, with many BDC bonds trading at spreads not far from the BB rated segment of the Bloomberg US Corporate index. From here, further material widening would likely require a more acute shock – most plausibly a reassessment of balance sheet liquidity risk among non-traded BDCs. For now, that risk appears manageable given structural guardrails, including redemption limits and access to bank credit facilities.

Fundamentals: Not breaking, not healing

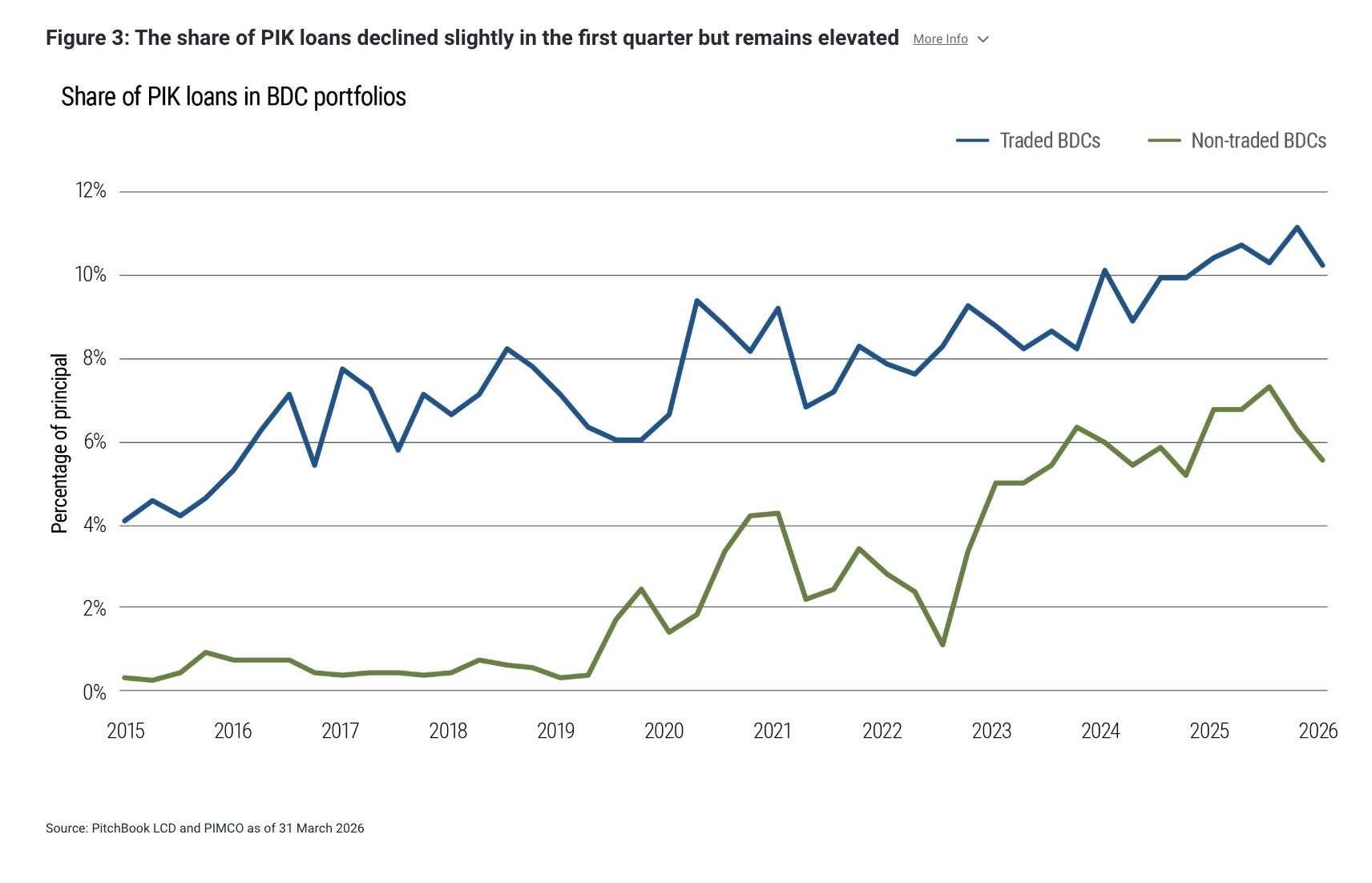

Looking at the underlying portfolios of BDCs, the fundamental picture is not breaking, but it is not healing, either. Sequentially, conditions look broadly stable: The share of payment-in-kind (PIK) loans was essentially unchanged in the first quarter of this year, suggesting limited incremental stress for now (see Figure 3). Year over year, however, the trend still points to deterioration.

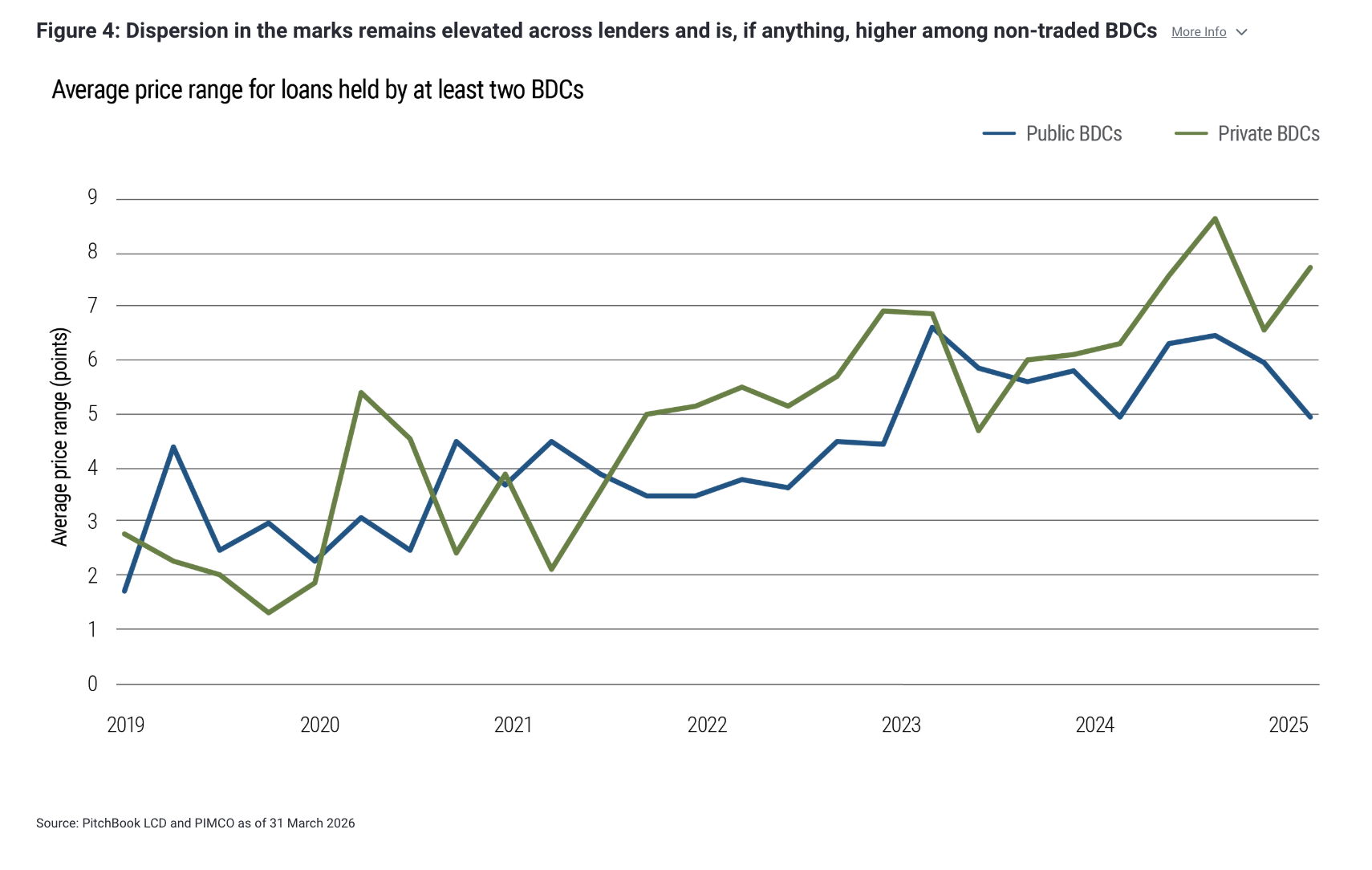

The more important signal continues to come from the marks. Dispersion remains elevated across lenders and, if anything, is higher among non-traded BDCs despite the perception of smoother reported performance (see Figure 4). Low time-series volatility alongside high cross-sectional dispersion is difficult to square with a common pricing anchor. It suggests NAVs are increasingly driven by manager-specific assumptions rather than a shared market-clearing level.

That is where fundamentals and flows connect. Smoothed valuations can support reported NAVs in the near term, but they also reduce transparency and widen the confidence gap across managers. As confidence erodes, redemption pressure can intensify, forcing managers to raise liquidity – often by selling the most liquid or better-marked assets first.

Absent a clear moderation in outflows, financing conditions are likely to tighten further. That raises the probability that valuations eventually converge toward market-clearing levels – through NAV markdowns, wider secondary discounts, or realized losses.

Direct lending faces the cycle; ABF diversifies away from it

Notwithstanding the many fundamental challenges that will continue to pressure direct lending portfolios, the broader takeaway is that private credit is not a monolithic asset class. The stress emerging in parts of direct lending says something important about corporate credit exposure, but less about the full private credit opportunity set.

We continue to think asset-based finance (ABF), along with high quality consumer and mortgage credit, currently stands out on diversification and valuation. ABF cash flows are less directly tied to corporate earnings, and the collateral base spans residential and commercial real estate, hard assets, and other pools of contractual cash flows. That has historically made ABF generally less correlated with the corporate credit cycle and often supported by structural downside mitigation embedded in the underlying assets.

Unlike direct lending, which is predominantly non-investment-grade corporate risk, many ABF exposures have the potential to deliver investment-grade-like profiles. That makes them more capital-efficient for large allocators such as insurance companies and helps explain why the opportunity is anchored less in headline yield than in opportunities for resilience, diversification, and risk-adjusted returns.

Disclosures

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

Charts are provided for illustrative purposes and are not indicative of the past or future performance of any PIMCO product. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. It is not possible to invest directly in an unmanaged index.

Past performance is not a guarantee or a reliable indicator of future results. References to specific securities and their issuers are not intended and should not be interpreted as recommendations to purchase, sell or hold such securities. PIMCO products and strategies may or may not include the securities referenced and, if such securities are included, no representation is being made that such securities will continue to be included.

All Investments contain risk and may lose value. An investment in a BDC is subject to credit and investment risk, leverage risk, market and valuation risk, price volatility risk, liquidity risk, interest rate risk and structural and regulatory risk. Private credit involves an investment in non-publicly traded securities which may be subject to illiquidity risk. Portfolios that invest in private credit may be leveraged and may engage in speculative investment practices that increase the risk of investment loss. The value of real estate and portfolios that invest in real estate may fluctuate due to: losses from casualty or condemnation, changes in local and general economic conditions, supply and demand, interest rates, property tax rates, regulatory limitations on rents, zoning laws, and operating expenses. REITs are subject to risk, such as poor performance by the manager, adverse changes to tax laws or failure to qualify for tax-free pass-through of income. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the author and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

CMR2026-0626-5663962

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© PIMCO

Read more commentaries by PIMCO