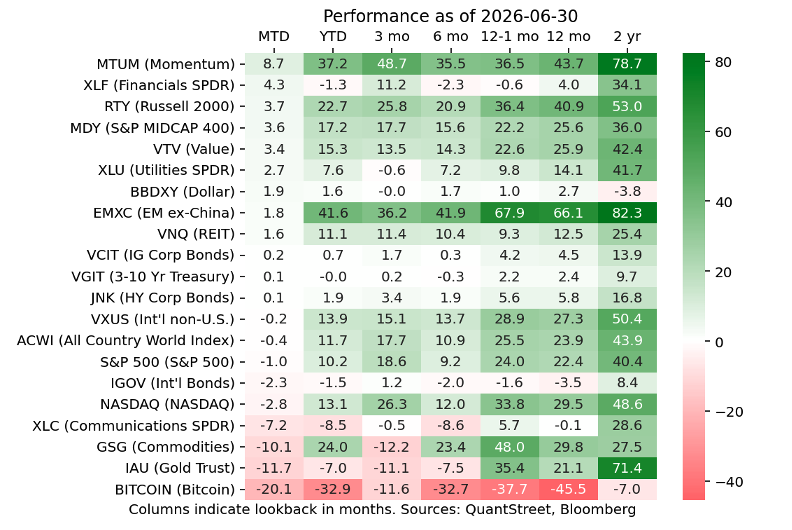

From our vantage point, the most interesting shift in market price action in June was the strong outperformance of value stocks compared to the broad market and tech. VTV, Vanguard’s value ETF, was up 3.4% on the month, while the S&P 500 was down 1% and the tech-heavy Nasdaq index was down 2.8%. The dollar had a strong month, up 1.9%, and is now up 2.7% on the year, after being down significantly in 2025. Two dollar hedges, bitcoin and gold, both got crushed in June, though gold remains up 21% on a year-over-year basis. For what it’s worth, Goldman Sachs (and we) remain bullish on gold, though the next gold cycle is likely to only materialize when the market expects the Fed to start cutting rates (second half of 2027, according to Goldman).

To gain more insight into what’s going on, let’s look at the components of VTV and QQQ (the largest Nasdaq-100) ETFs. VTV contains America’s blue-chip, traditional economy companies:

My guess is Micron, which makes memory chips and is up 700% over the last year, will soon be dropped from the list of value stocks. On the other hand, QQQ contains the tech luminaries (including Micron):

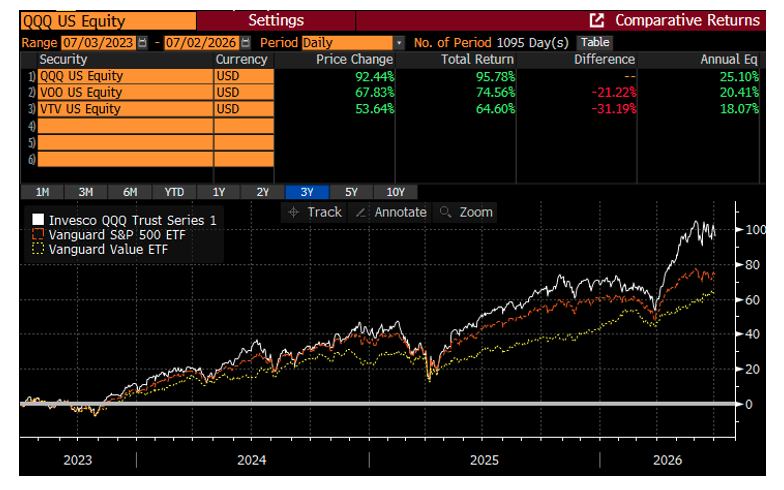

The relative performance of the two indexes, as well as VOO (an S&P 500 ETF), over the prior few years looks like this:

Read more: Passive and Buy And Hold Investing Don’t Work Unless!

What might explain these performance gaps?

First, QQQ is more volatile than VOO which is more volatile than VTV. So partially this performance ranking reflects the relative riskiness, and thus the relative risk compensation, of the three indexes. (For the academic sticklers out there, the beta ranking is the same.)

Another reason, though, is the market’s view on how different sectors of the economy will be impacted by the AI buildout. The most quickly impacted sector is tech. These are the folks who bring us large language models and the chips on which to run them. Second in order of impact is the broad S&P 500 index, since it has a very heavy loading on the Magnificent 7, as we are frequently reminded. Last in order of impact—though perhaps not in terms of magnitude of impact—are the traditional economy companies, like banks, consumer goods firms, retailers, and pharmaceuticals.

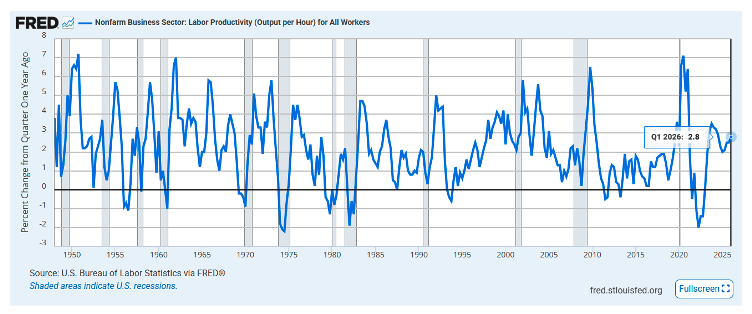

The underlying premise of the AI trade is that AI-driven productivity gains will impact exactly the firms that are in VTV, admittedly with some lag. There is conflicting evidence as to whether this is happening. The good news is that labor productivity, measured via real output per hour worked, has ticked up recently to 2.8%. If this persists, it would bring the US economy back to its heady growth days of the ‘50s and ‘60s, as well as of the late ‘90s. One interpretation of this is that AI is starting to boost economy-wide productivity.

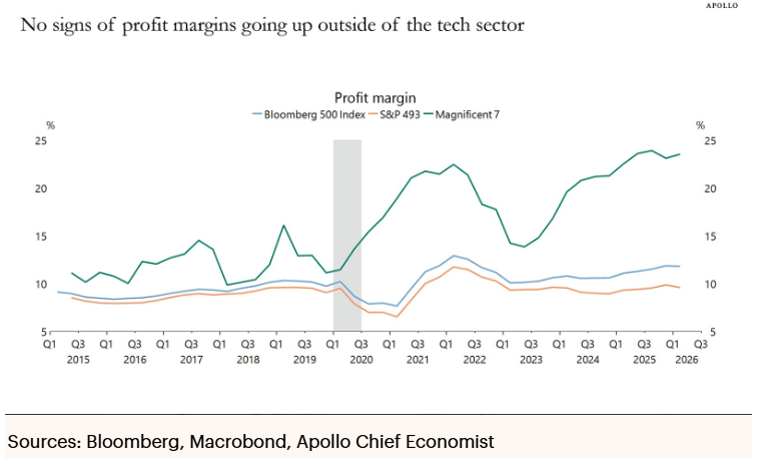

On the not-so-good news side, Torsten Slok in his June 30, 2026 Daily Spark Note points out that profit margins in the non-Mag 7 part of the S&P 500 have not meaningfully increased. Maybe the VTV price action in June of 2026 suggests that the market is thinking the AI impact on the profitability of the rest of the corporate sector will come soon enough.

Positioning for the Coming Month

This month, our valuation models identify sector after sector as having low expected year-ahead returns due to high valuation measures, either price-to-book ratios or sector-specific CAPEs (cyclically adjusted price-to-earnings ratios). Our valuation models haven’t sent this uniform a signal in quite some time. The heavily impacted sectors are: equal-weighted S&P 500, the Nasdaq, small- and mid-caps, communications, software, and technology, among others. Being “heavily impacted” requires two things: first, you need to have high valuations and second, they need to have historically forecasted your future returns. (The usual disclaimer applies: These are just model forecasts. Reality has no obligation to abide by our model. Futures returns may differ materially from the forecasts.)

Our interpretation is that a lot of good news is already priced in. (For a particularly panicky though fun take on this situation, see this piece from the FT.) As we wrote in last month’s investor letter, bull cycles can last a really long time, and the current bull market may have a lot of legs left. We are far from turning bearish, but feel it prudent to diversify a bit into the traditional economy stocks that have been less impacted by the AI trade.

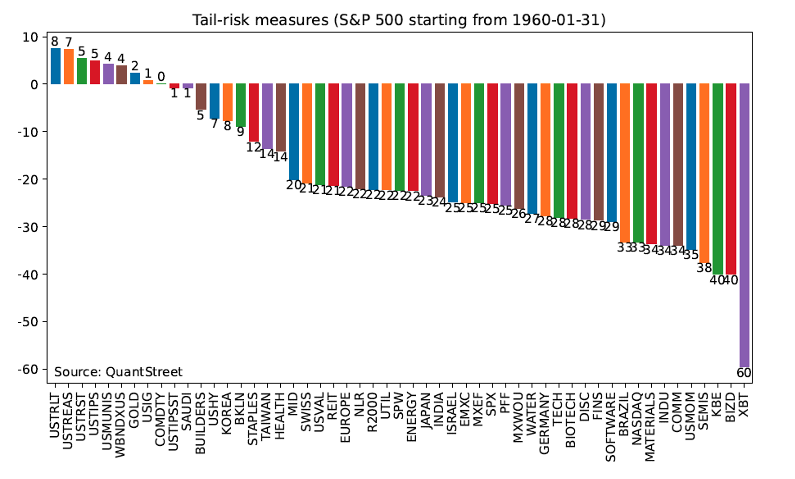

We are thus continuing the shift started last month into a heavier VTV exposure across all our portfolios. While we maintain the usual volatility targets across our portfolios, VTV’s lower tail risk (see chart below which shows the average return of each sector in a 1-in-20 bad S&P 500 return year) relative to the broader market has the ancillary benefit of lowering our portfolio’s tail risk exposure.

Finally, for some of our clients for whom we think this is a fit, we are recommending allocating a small portion of their public market exposures to alternatives, as another form of away-from-tech diversification. There are many issues that need to be carefully considered here, but it’s a conversation worth having. Finally, we have spent a fair bit of time analyzing 351 ETF exchanges for one of our clients. This is a transaction where a basket of long-held, low cost-basis stocks can be exchanged for a newly formed ETF, which will track a broad market index, like the S&P 500. There are also many issues here that need careful consideration. If you would like to discuss either of these two portfolio options, please reach out.

Working with QuantStreet

QuantStreet offers financial planning, wealth management, model portfolios, portfolio analytics, and a platform for advisors looking to gain independence. The firm’s investment approach is systematic, data-driven, and shaped by years of investing experience. To work with or learn more about QuantStreet, join our mailing list or contact us at [email protected]. Also, please sign up for our Substack.

QuantStreet is a registered investment advisor. Registration does not imply a certain level of skill or training. All financial forecasts are fraught with risk and uncertainty. Our views may prove incorrect and market outcomes may be materially worse than we anticipate. Please see our full disclosure about the limitations of forward-looking statements and the risks of investing at https://quantstreetcapital.com/blog_disclosure/.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© QuantStreet Capital

Read more commentaries by QuantStreet Capital