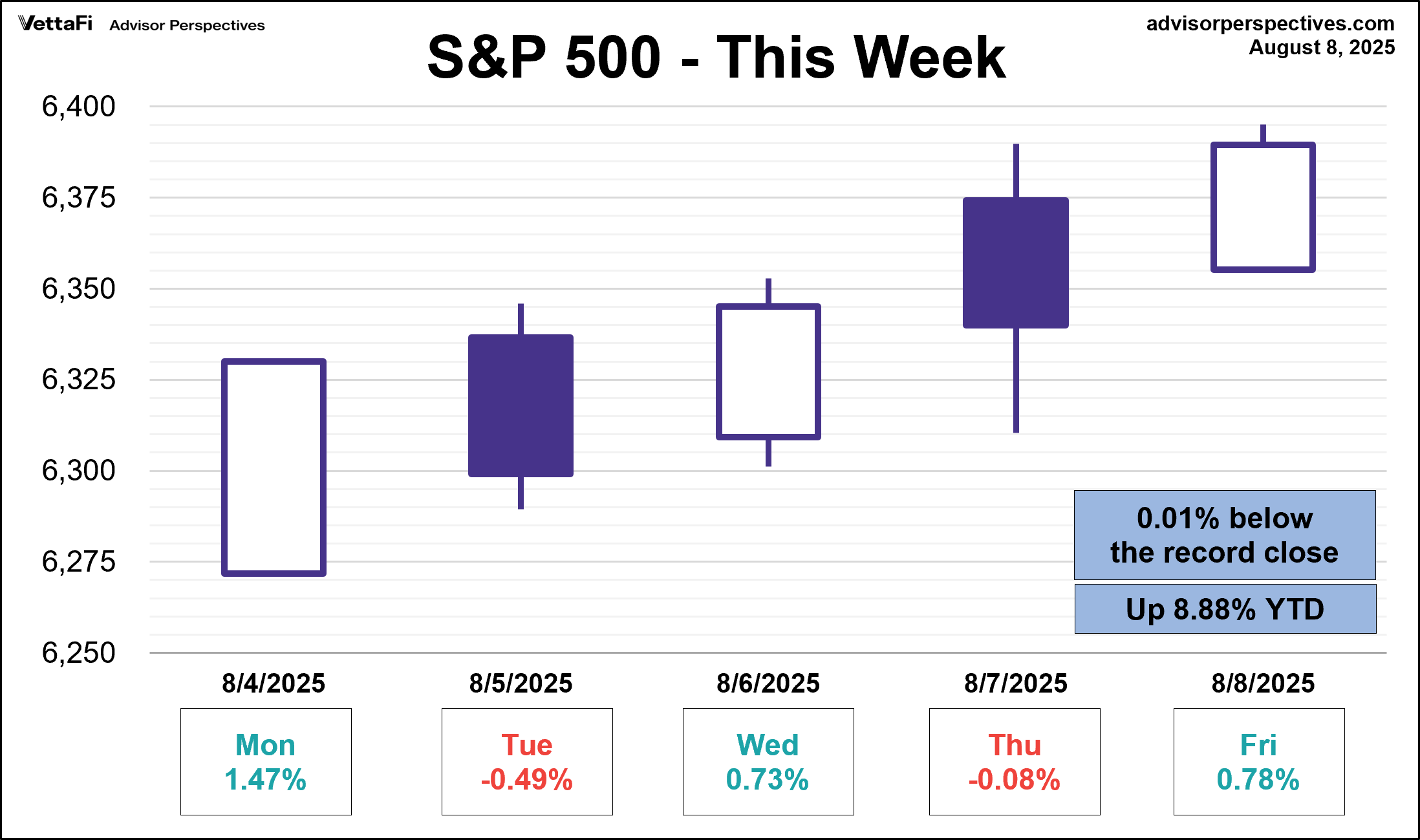

The week of July 28th-August 1st was one of the busiest of the year for financial markets, with a plethora of economic data, a Fed meeting, and significant market volatility. A strong GDP rebound and the Federal Reserve's decision to hold rates steady were quickly overshadowed by a weaker-than-expected jobs report and hotter-than-anticipated inflation. These negative surprises set the tone for the week, with the S&P 500 experiencing one of its worst weeks in over two months, as the Friday jobs report in particular dragged markets down after dramatic downward revisions.

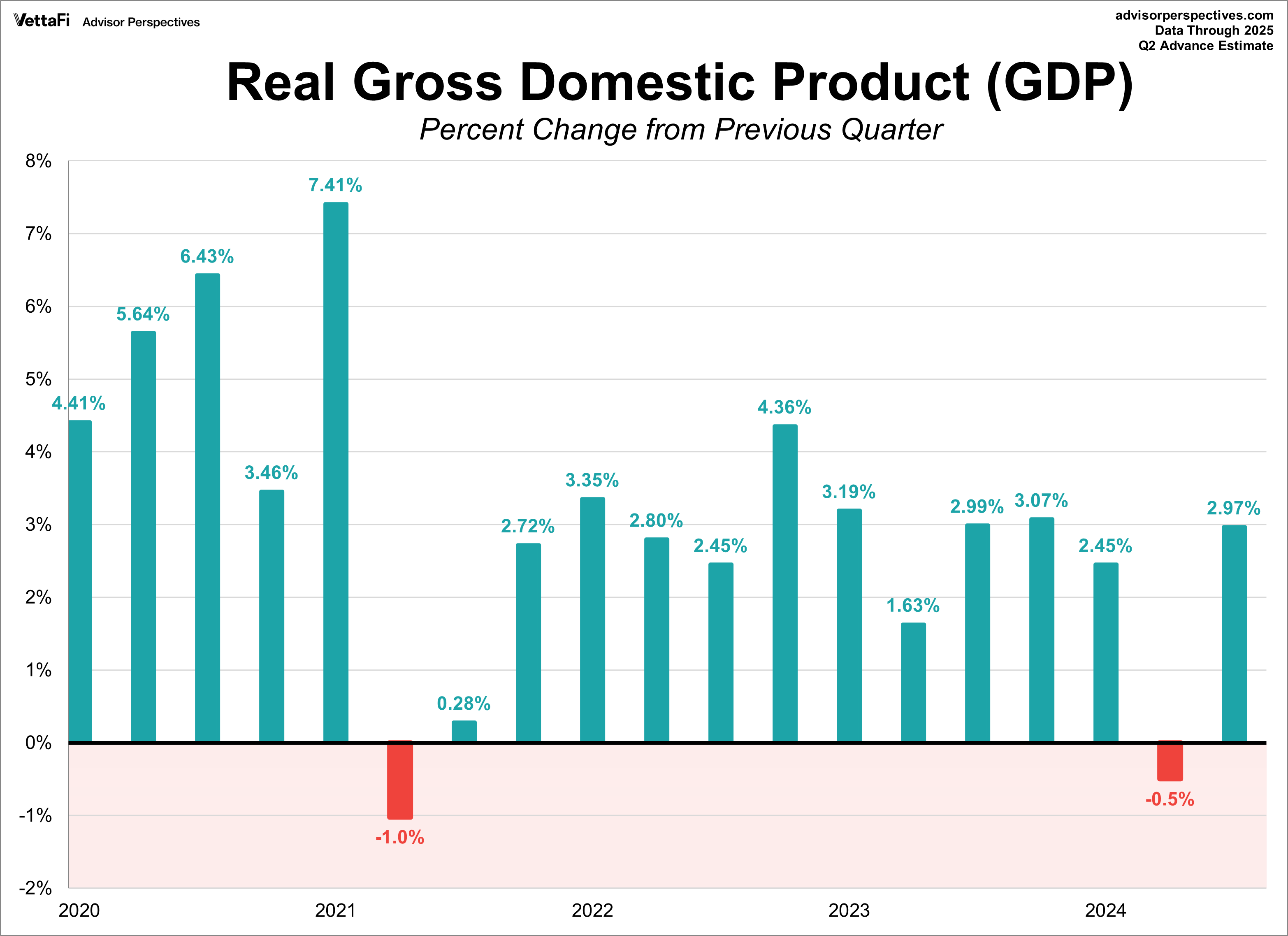

Gross Domestic Product (GDP)

According to the advance estimate, the U.S. economy posted a strong rebound in the second quarter, with real GDP — the inflation-adjusted measure of all goods and services produced — increasing at an annual rate of 3.0%. This marks a significant turnaround from the first quarter’s 0.5% contraction and surpassed the 2.5% forecast. The expansion was primarily driven by a decline in imports and an increase in consumer spending, although these gains were partially offset by a significant decline in business investment and a fall in exports.

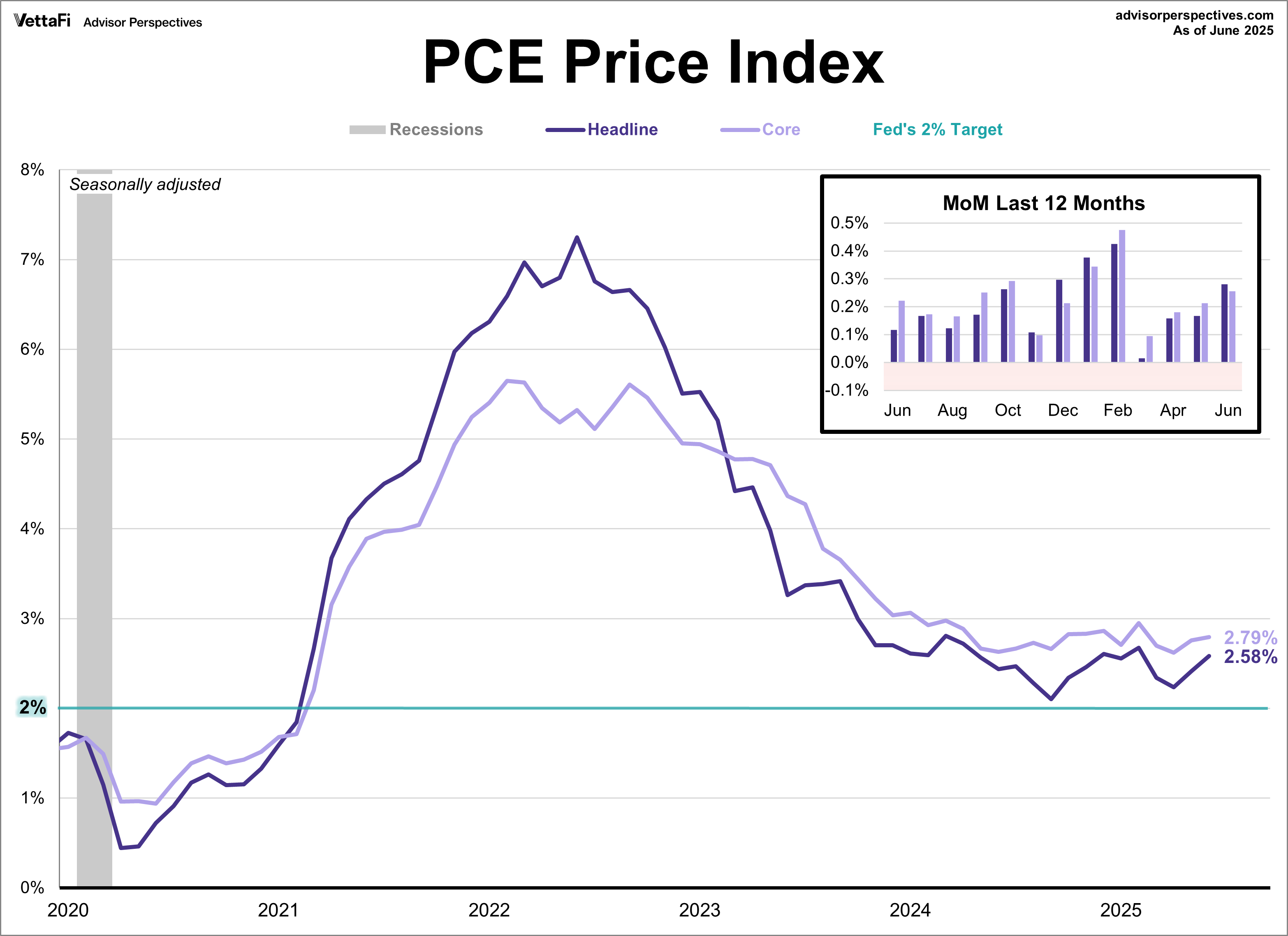

PCE Price Index

The Federal Reserve’s preferred inflation gauge was higher than expected last month, inching further away from the 2% target. The Core Personal Consumption Expenditures (PCE) Price Index, which excludes volatile food and energy costs, rose 2.8% year-over-year in June. This surpassed the expected 2.7% growth and was a slight pickup from May. The headline index also saw a higher-than-expected annual increase, rising 2.6% against a forecast of 2.5%, and was up from 2.4% in May. On a monthly basis, both core and headline prices rose by 0.3%, as expected.

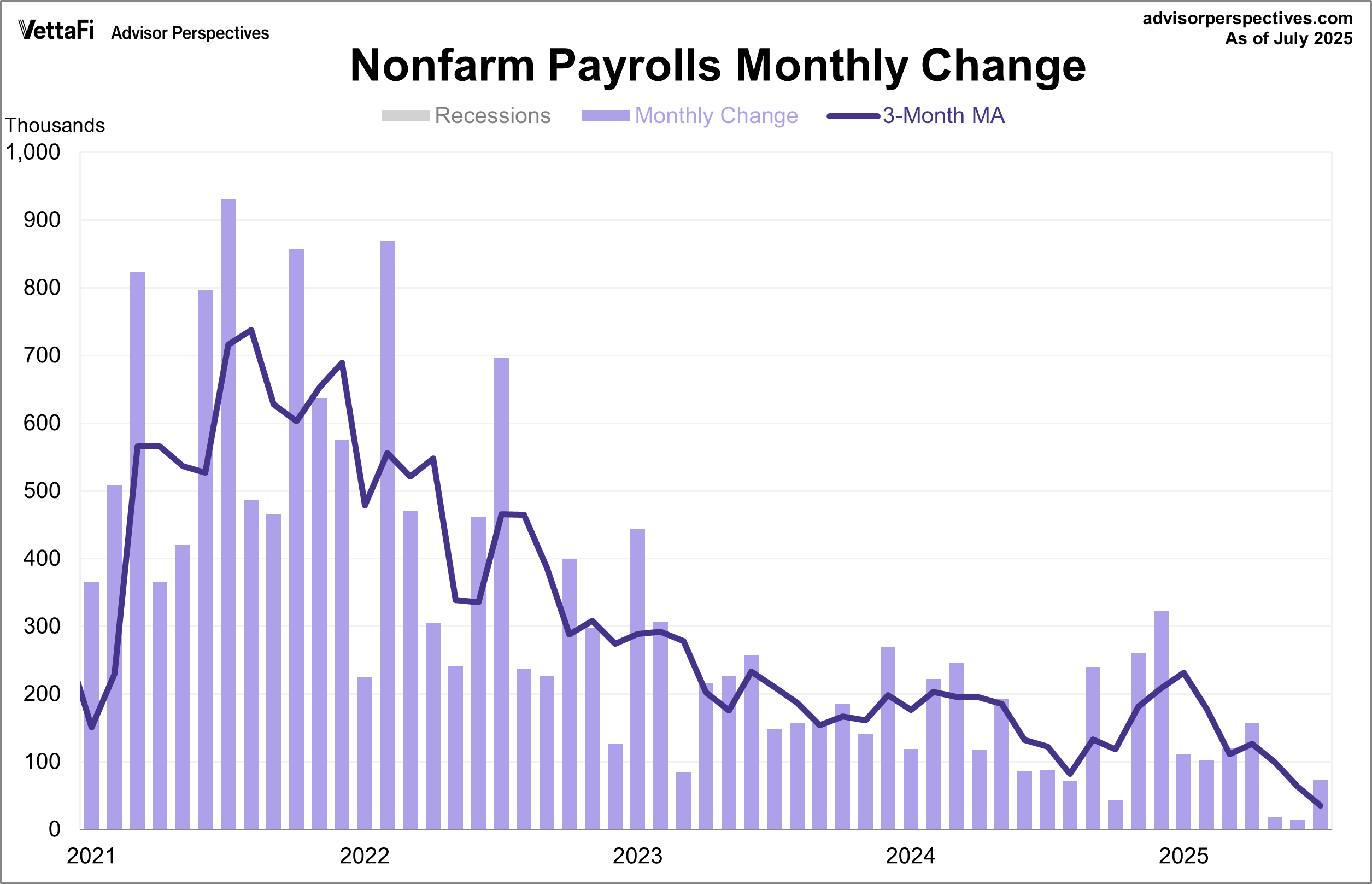

BLS Employment Report

The U.S. labor market is starting to show signs of trouble, as job growth was slower than expected and the unemployment rate ticked up. The latest employment report showed that 73,000 jobs were added last month, falling short of the expected 106,000 addition. However, the most alarming part of the report was the dramatic downward revision of previous months' totals. The jobs added in June were revised from 147,000 down to 14,000, while May's total fell from 125,000 to just 19,000. Meanwhile, the unemployment rate inched up to 4.2%, as expected, though it remains near a historically low level.

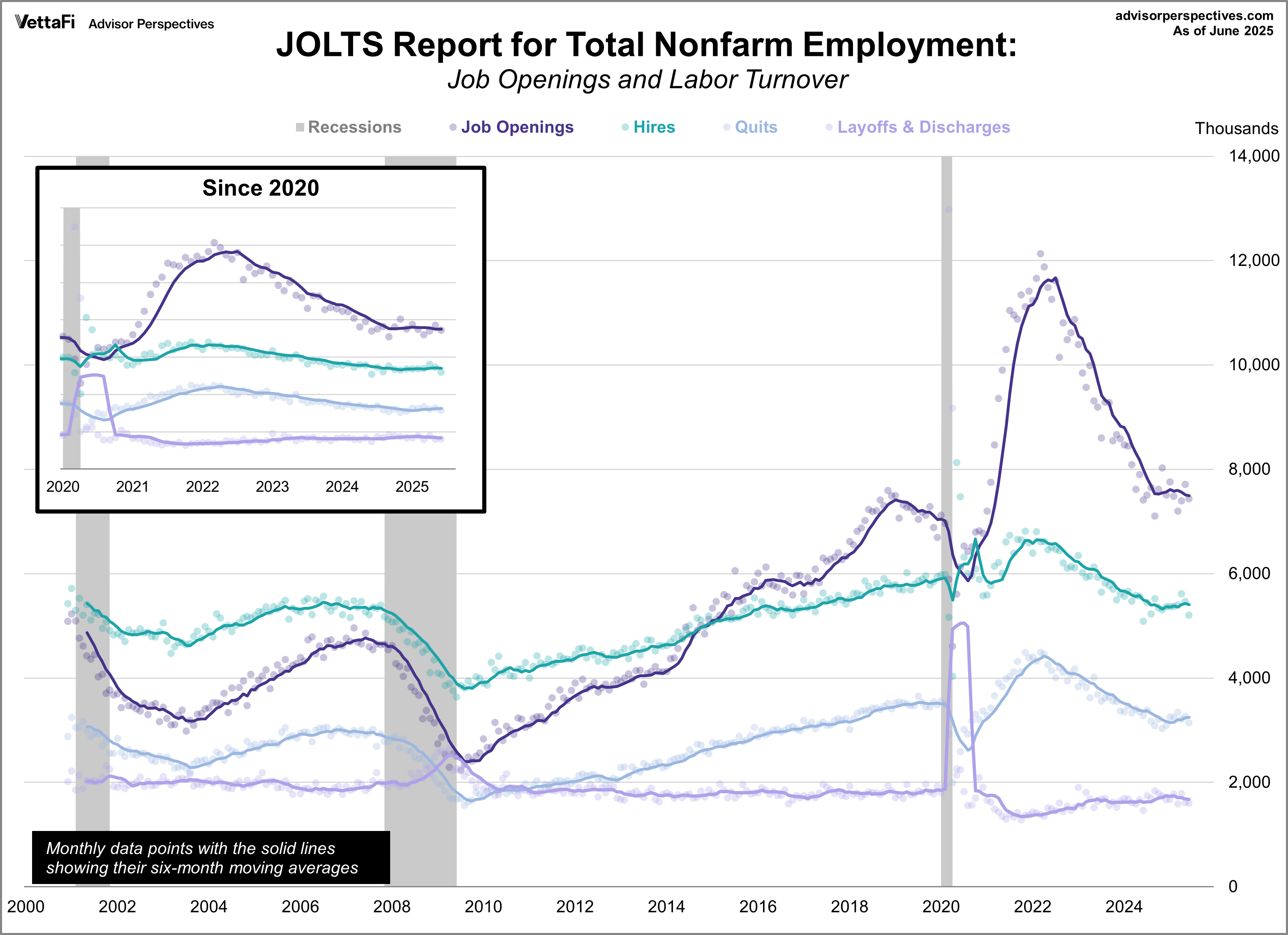

Job Openings and Labor Turnover Summary (JOLTS)

Job openings fell more than expected in June, declining for the first time in three months according to the latest JOLTS report. The number of openings dropped by 275,000 to 7.437 million, falling short of the expected 7.510 million. The report also revealed broader declines, with the hiring rate falling to 3.3% — near its lowest in a decade — and the quit rate remaining at 2.0%, below pre-pandemic norms. Despite the slowing pace in hiring, the labor market remains in a 'low hire, low fire' environment as layoffs continue to be low.

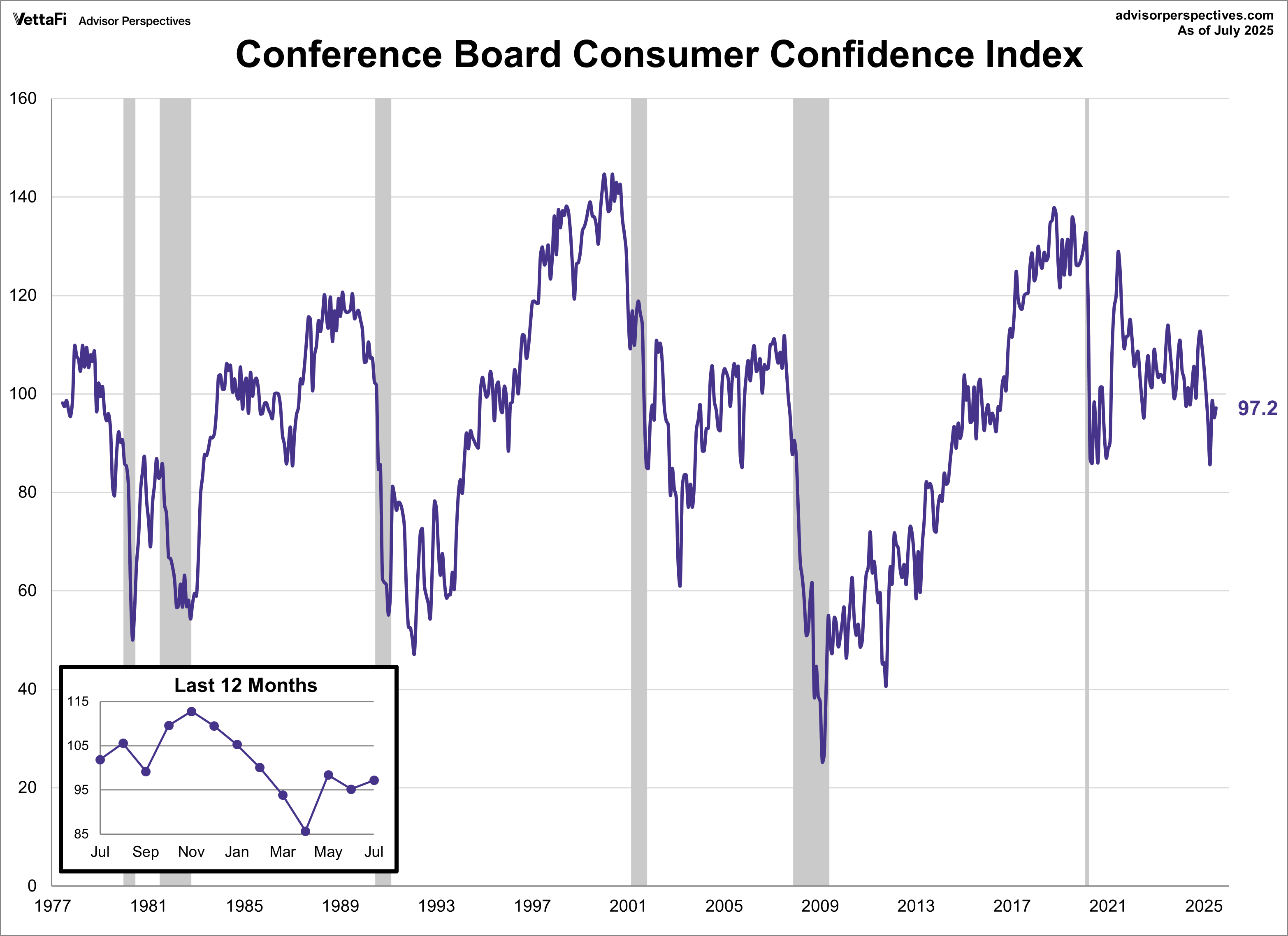

Conference Board Consumer Confidence Index

Consumer confidence improved slightly in July, with the Conference Board Consumer Confidence Index® rising 2.0 points to 97.2, surpassing the forecast of 95.9. This marks the index’s second gain in three months, suggesting a recent stabilization in consumer sentiment at a subdued level.

The rise was largely driven by greater optimism about future conditions, while assessments of the current situation worsened slightly. Notably, consumers are growing more concerned about current job availability but are more optimistic about their future income prospects. Other key takeaways from the survey showed that tariffs and inflation remain top of mind for consumers, though 12-month inflation expectations continued to ease.

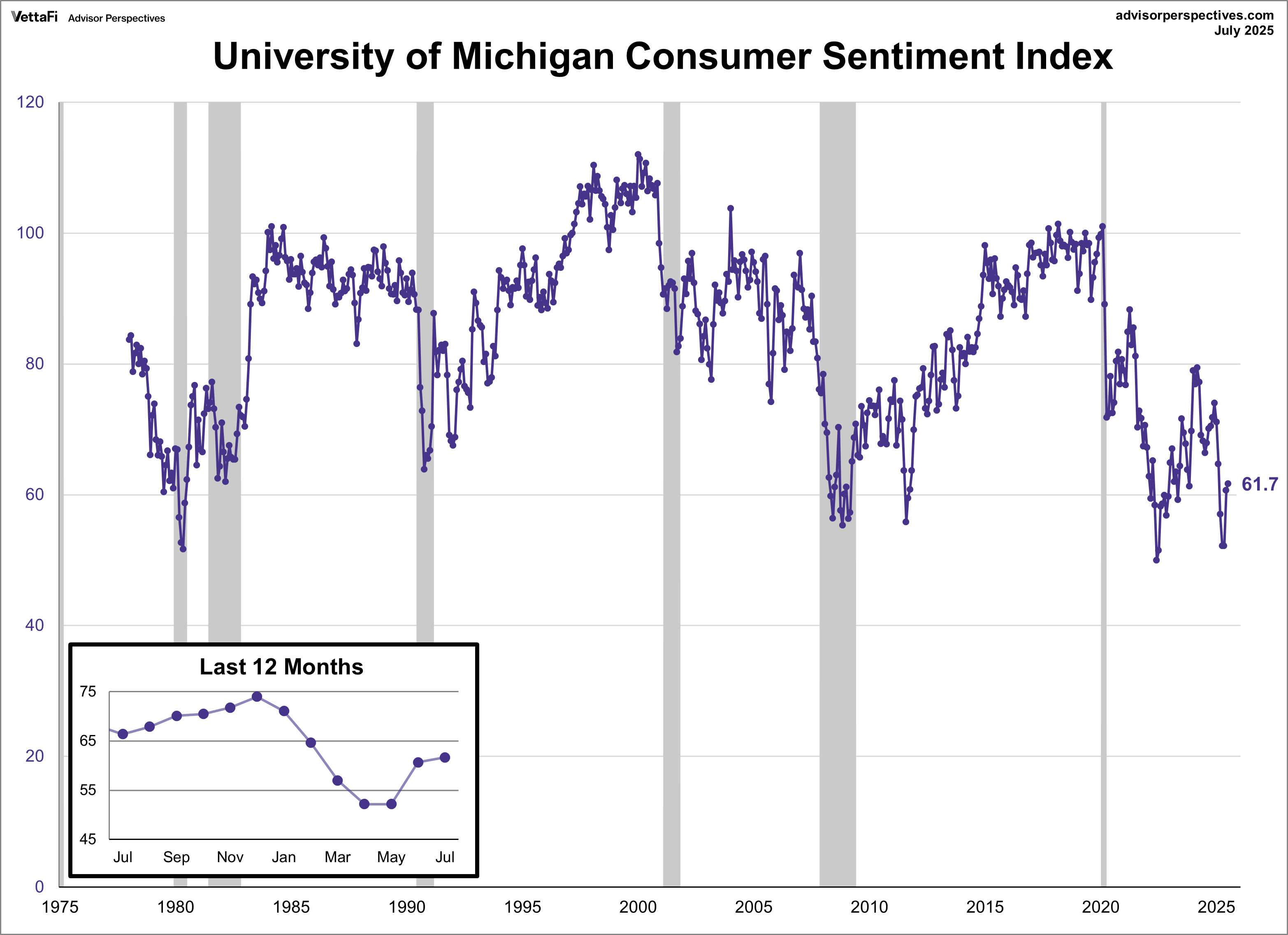

University of Michigan Consumer Sentiment Index

Consumer sentiment improved for a second straight month in July, with the University of Michigan Consumer Sentiment Index rising 1.0 point to 61.7. While this is the index’s highest level since February, it is still on the historically low end and indicates consumer attitudes remain broadly negative.

In contrast to the Conference Board’s Consumer Confidence Index, the index’s improvement in July was driven by an increase in optimism about current conditions but a fall in expected conditions. Inflation expectations also continued to ease for both the near and long term, though they remain historically high. Year-ahead expectations fell from 5.0% to 4.5%, while the five-year outlook dropped from 4.0% to 3.4%.

Market Reactions

The S&P 500 posted its largest weekly loss in over two months, falling 2.4%. This followed its worst day in over two months, a 1.6% loss on Friday after the release of the July jobs report. As a result, the SPDR S&P 500 ETF Trust (SPY) fell 2.4% last week. Meanwhile, the S&P Equal Weight Index was down 3.3% from the previous week and the Invesco S&P 500® Equal Weight ETF (RSP) fell 3.3%.

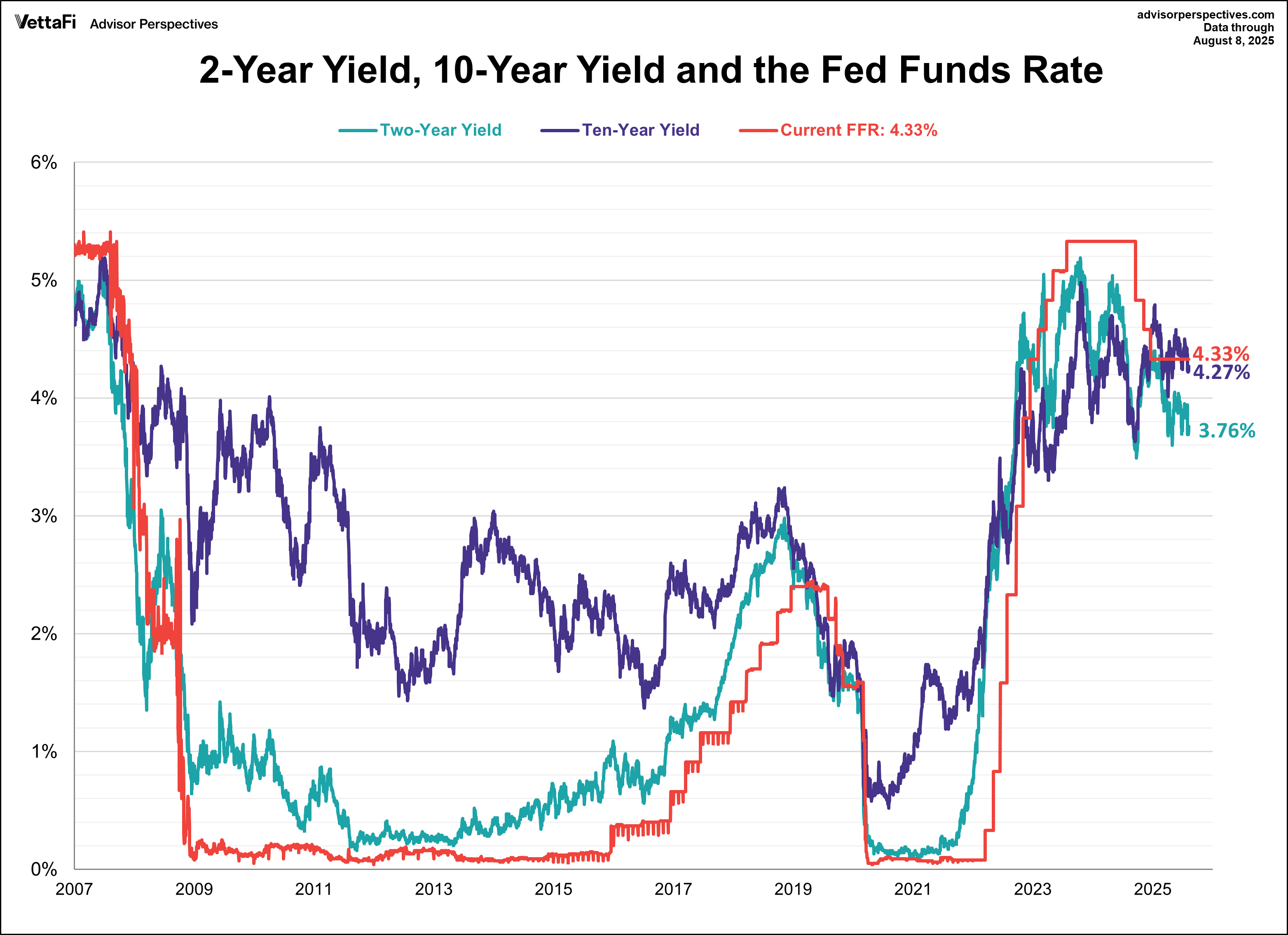

The 10-year Treasury yield finished the week at 4.23%, while the 2-year note finished at 3.69%. This is the lowest level for each bond yield in three months.

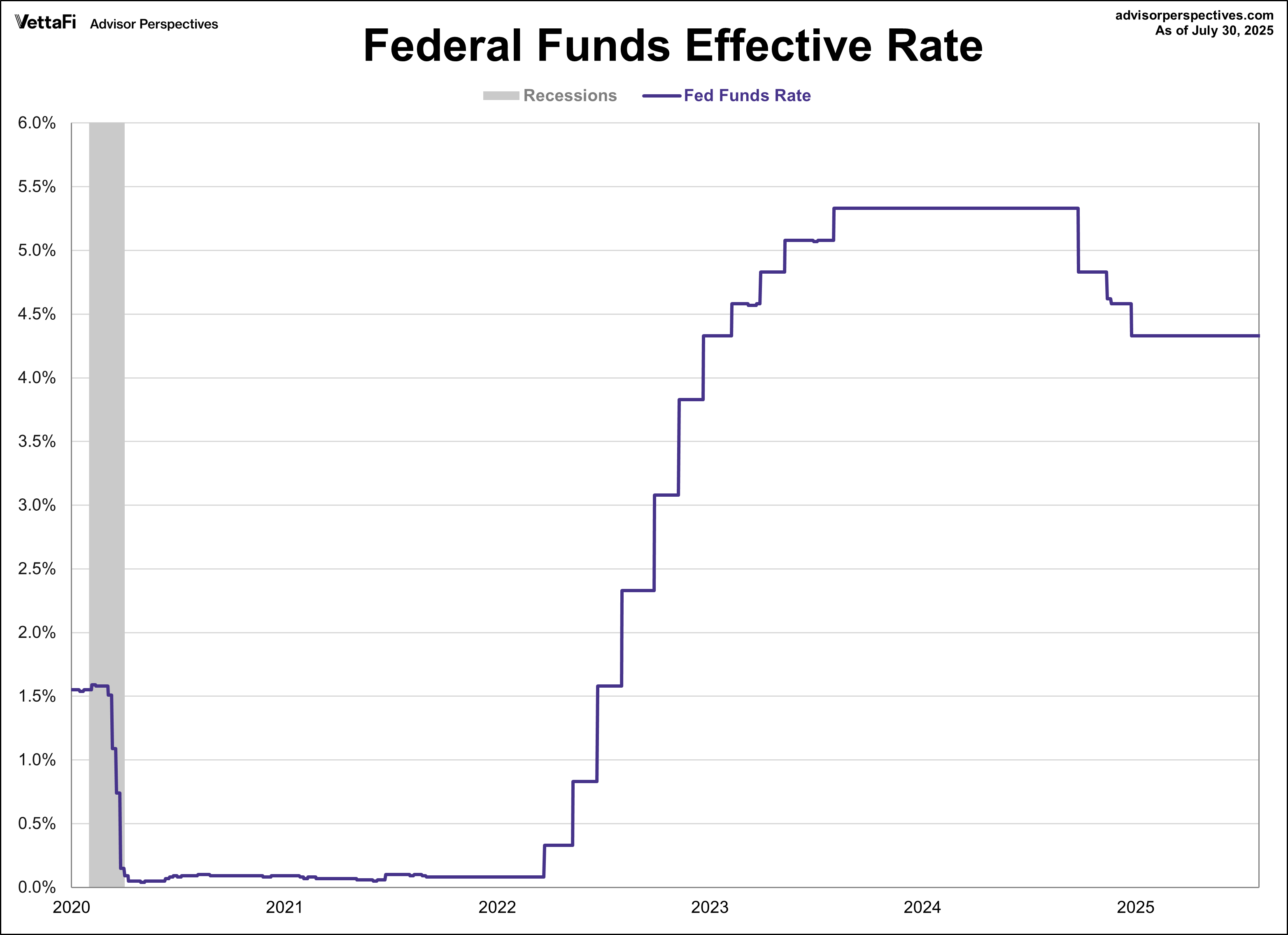

In their meeting last week, the Fed held rates steady at 4.25-4.50% for a fifth straight meeting. According to the CME FedWatch Tool, there's a strong likelihood of an interest rate cut at the Fed's next meeting, with an 88% probability. The market is also pricing in two additional 25 basis point cuts for the rest of the year, one at the October meeting and another at the December meeting.

Read more updates by Jen Nash