Banks’ businesses don’t change radically year to year so nor should their capital requirements. In the US, however, the Federal Reserve’s annual stress tests have been volatile, unpredictable and one of the main determinants of how much equity big banks need in the 12 months after the results come in. No other country uses this approach. Now as the Fed and other regulators prepare to tackle this and other banking rules under a biddable and deregulation-friendly White House, watchdogs need to ensure they don’t hastily give too much away.

Excitement about an easing of capital demands under President Donald Trump helped propel bank stocks to highs at the start of the year. But change has been slow to arrive, disappointing investors who had hoped for billions of dollars in rapid share buybacks. In truth, it was always going to take time to fill the roles that oversee reviews. Michelle Bowman has been nominated as vice-chair for supervision at the Fed and to lead its rulemaking efforts. Meanwhile, the acting heads at the Federal Deposit Insurance Corp. and Office of the Comptroller of the Currency are waiting to be confirmed in their roles after Treasury Secretary Scott Bessent made clear this month that there were no plans to merge these bodies. Bankers expect all three will look on the industry more favorably than their predecessors.

Out of a string of potential changes, the Fed’s stress test is likely to be tackled first. To speed things along and put pressure on Chair Jerome Powell, banks launched an extremely rare lawsuit against the US central bank on Dec. 24 — a day after the Fed said it planned to improve the transparency and reduce volatility of the tests.

The opacity of the models used in the exercise was deliberate, designed to stop banks optimizing their numbers to limit the impact, which is still a good idea. The Fed is offering to make the models more transparent, which could undermine the examination if it goes too far. But the worst proposal is to allow banks to debate the market scenarios chosen each year. That will just produce a barrage of complaints and risks diluting the process to the point it becomes meaningless — the tests should be stressful!

The Fed’s best idea is to grant banks two years to phase in the resulting capital demands, rather than in full at the start of each new year. A rolling stress capital requirement will allow banks to plan better, but reducing the variation in the results would also help. Last year, Goldman Sachs Group Inc. complained when its results led to a more than $6 billion jump in its equity requirements, or nearly a full percentage-point increase in its common equity tier 1 ratio. The bank had been expecting something like a $3 billion decline based on its own modeling; the Fed reduced its demands by one-fifth of a percentage point in response.

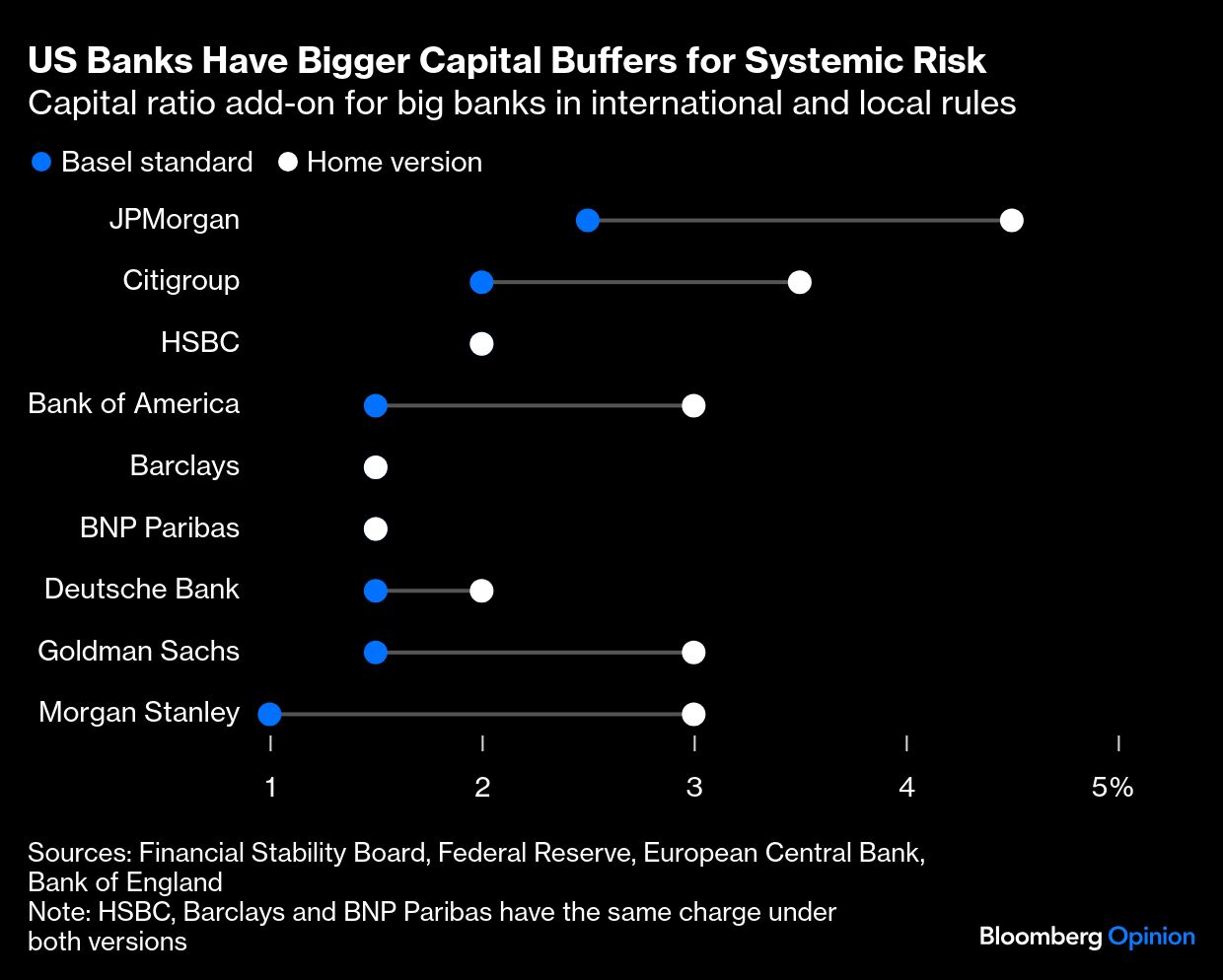

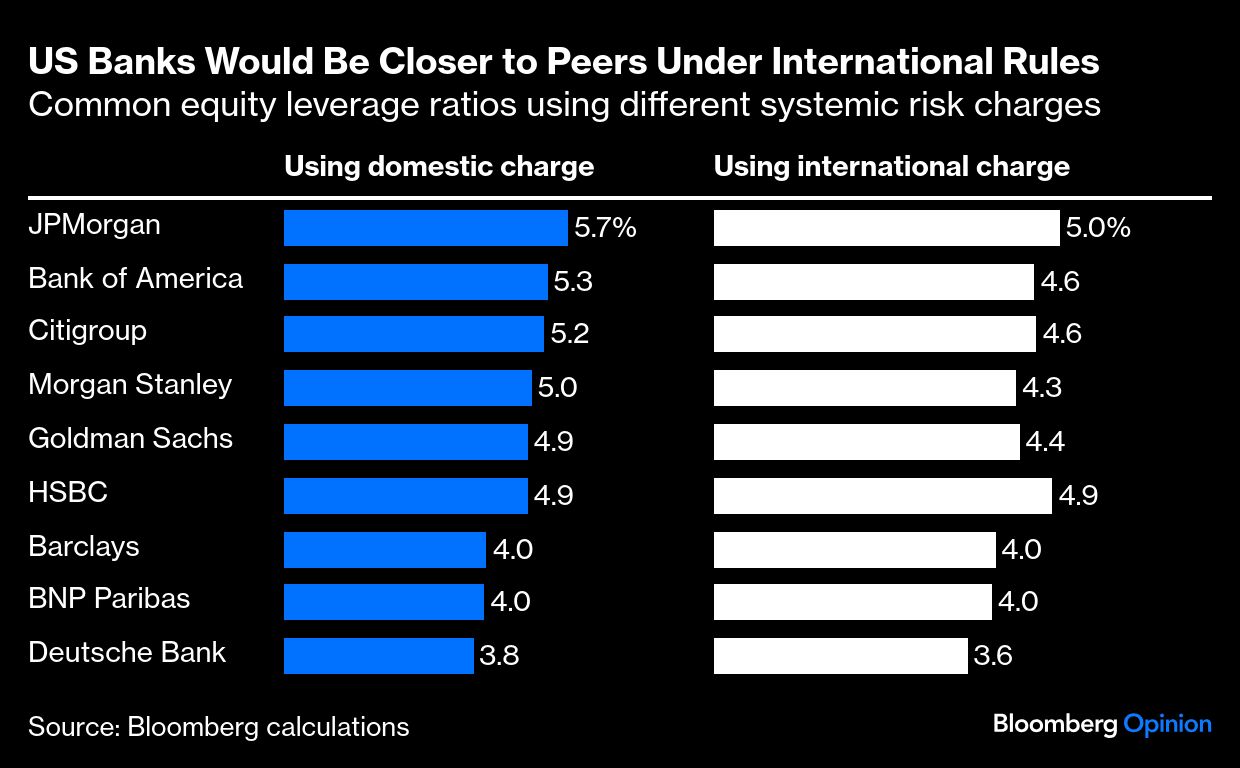

Another area where some banks are hopeful for change is a cut to the extra layer of capital that the largest and most interconnected – or systemically important – banks must have. The US version is tougher than for big European banks, where regulators mostly use the method created by global standard setters at the Basel Committee on Bank Supervision. For JPMorgan Chase & Co. and Morgan Stanley, the so-called G-SIB surcharge increases their capital ratios by two percentage points compared with the international standard. For Bank of America Corp., Citigroup Inc. and Goldman Sachs, it is 1.5 percentage points greater. Only Deutsche Bank AG and UBS Group AG among big European banks have a higher charge than the Basel version.

If US banks used the international standard instead, their total equity capital would be more in line with Europeans as a proportion of total assets (using the most comparable leverage exposure measure). However, moving US banks onto the international version would be a huge giveaway, so investors shouldn’t hold their breath. At JPMorgan, for example, this would release about $35 billion of capital on current numbers.

Nevertheless, US regulators have previously pledged to review how the G-SIB buffer interacts with economic growth or the size of the Fed’s balance sheet. The systemic importance of US banks in the US scoring method simply grows when the global economy does, whereas in the international version their importance only increases if a bank grows relative to the economy. Changing that aspect could allow regulators to trim the charge on its big banks slightly and stop it from inflating excessively in the future.

A third reform that might come soon is to slash the capital charges banks face for owning Treasuries. Bessent has talked about this, and Beth Hammack, a former Goldman banker who now runs the Cleveland Fed, discussed it in a recent speech. The aim would be to protect liquidity in the government bond market by making it less costly for banks to trade there. However, this looks to me like a short cut in trying to solve a more complex set of problems.

Finally there’s the Basel III endgame, the updating of US rules to the latest international standards that dominated financial rulemaking under the last White House. This is a longer and more complicated effort because it involves rewriting hundreds of pages of a deeply unpopular proposal.

Bankers expect the stress-testing regime to be revisited soonest because the Fed doesn’t need the agreement of other regulators to act. The big-bank buffer could also be adjusted quite quickly when the heads of other agencies are confirmed. But what would be better is for regulators to review all these things simultaneously and come up with a suite of measures that’s more stable, coherent and in line with international standards. Bowman advocated this approach in several speeches while she was a Fed board member.

This would take time and likely be frustrating for banks and their shareholders, but it could produce a far superior long-term settlement. As I’ve written before: Getting this stuff right is more important than just getting it done.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Paul J. Davies