Investors are fretting that a year-long rally in global credit is papering over the risk that US policy uncertainty tips the world’s largest economy into a recession.

Some are sounding the alarm that this could be a ‘gray swan’ event — a shock that is predictable in theory, but largely ignored until it hits. Unlike black swans, which are truly unforeseen, gray swans lurk in plain sight.

In contrast to the selloff in other asset classes, very little bad news has been priced into credit markets so far, with banks on Monday pulling off a whopping €7.45 billion ($8.1 billion) debt deal. That may look complacent as US President Donald Trump prepares to impose a barrage of trade tariffs this week.

“Credit markets in the US are pricing in a much lower chance of a recession than equity markets are and something has to give,” said Chris Ellis, a London-based high-yield portfolio manager at Axa Investment Managers. “I’ve heard it described as a ‘gray swan’ risk in the market, which seems apt to me. We don’t know exactly what could trigger a selloff, but we have to tread carefully.”

A model by JPMorgan Chase & Co. strategists showed in mid-March that the S&P 500 was pricing a 33% probability of a US recession, up from 17% at the end of November, while credit was only pricing in 9% to 12% odds.

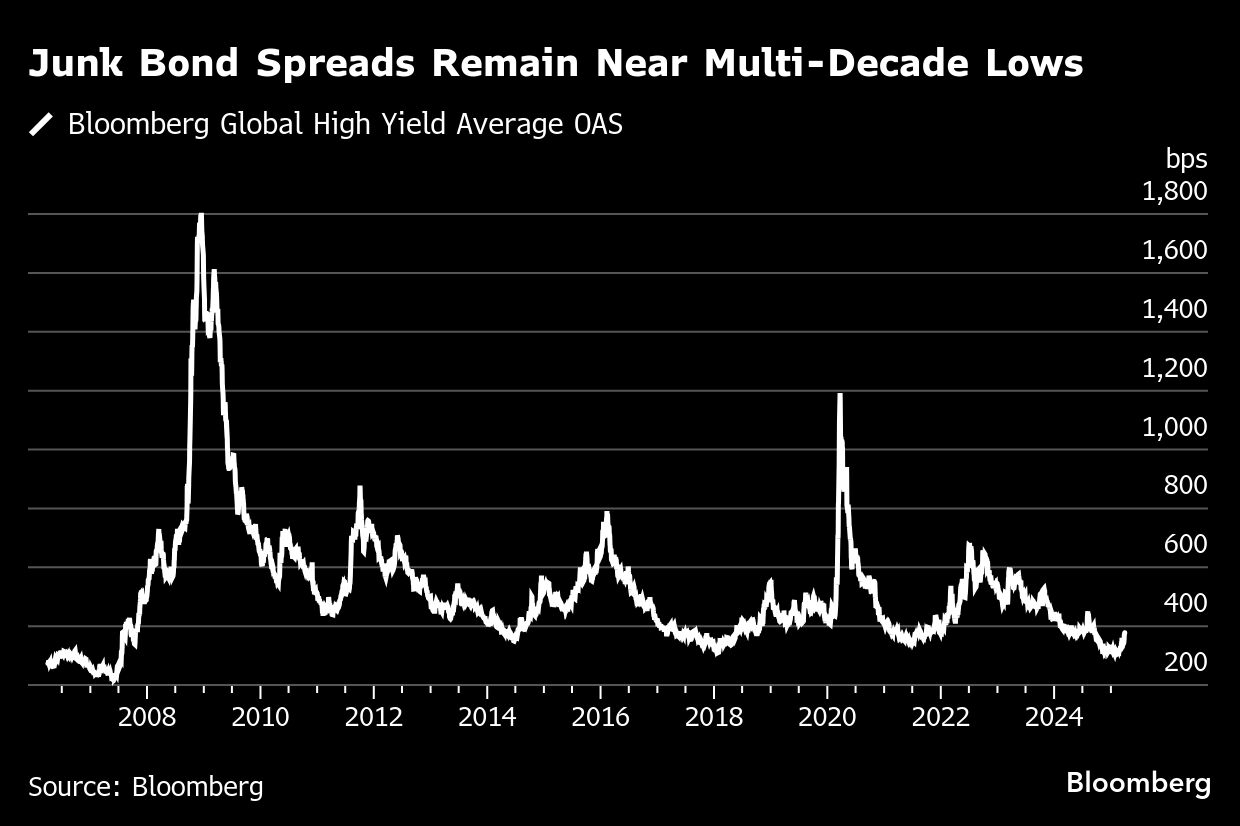

While the bank’s strategists thought the US stock market might be overpricing the risk, the S&P 500 just suffered its worst quarter since 2022. Meanwhile, the pain seen so far in junk bond markets, supposedly the riskiest corner of the debt world, has been limited.

With Trump planning a “Liberation Day” on April 2 to impose tariffs on major trading partners and the European Union prepared to retaliate, the risks should be widely known by now. The new trade restrictions placed on the auto industry last week offered an example of how credit could be vulnerable to this kind of gray swan risk.

The 25% tariffs on all non-US auto companies forced one auto supplier to sweeten pricing to avoid having to cancel a live debt deal, while a number of other firms in both Europe and the US saw their bond prices drop and spreads widen. Now a $2.25 billion buyout debt package is being threatened by this week’s tariff risks.

And on Tuesday, Pacific Investment Management Co., one the world’s biggest bond investors, warned that President Donald Trump’s aggressive trade, cost-cutting and immigration policies threaten to slow the US economy by more than previously expected.

Buying Blindly

Overall, technical factors have been masking the impact. A lack of dealmaking has meant less debt supply, while the attractive coupons on offer in a higher-rate environment have been pulling in fund flows. Some investors have also been switching from leveraged loans to high-yield bonds.

“The technical has been so strong in credit that passive investors like ETFs or maturity funds are buying bonds blindly,” said Candriam’s global head of fixed income Nicolas Jullien.

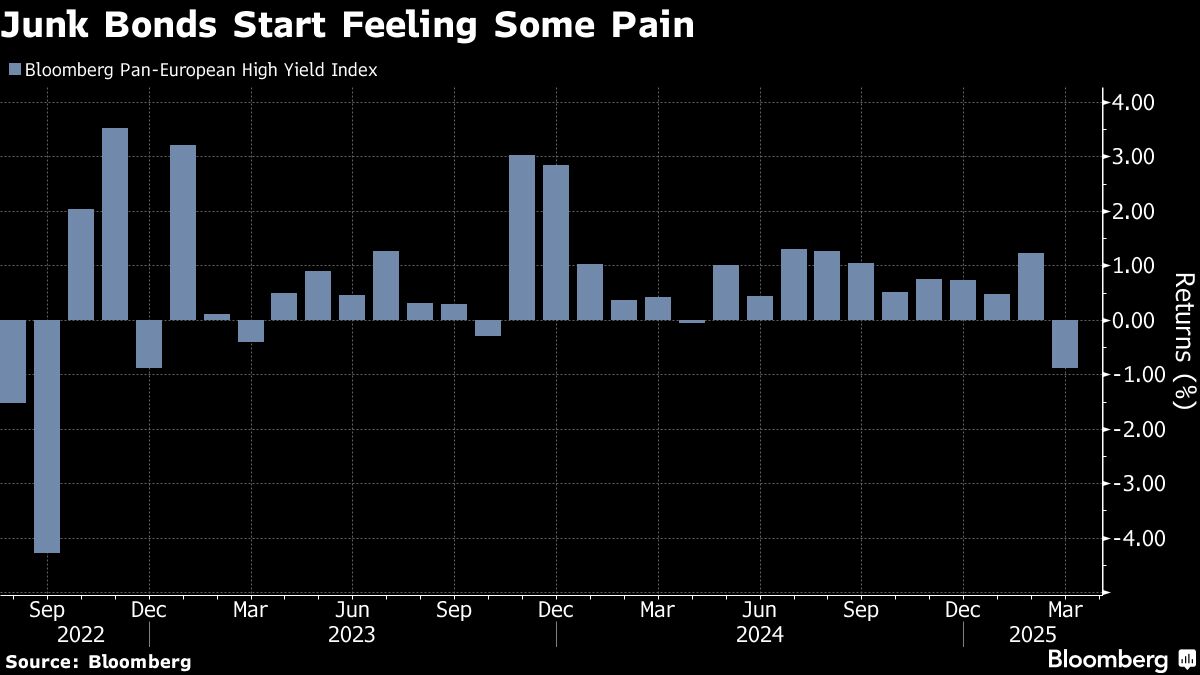

In recent weeks, high-yield bonds have started selling off along with global stock markets. March was the worst month for high-yield bond returns since September 2022 in Europe and October 2023 in the US.

And yet, on a historic basis, spreads are still in very good shape. Typically, a junk bond spread of 800 basis points is seen as presaging a recession. Even after the recent selloff, they are less than half of that on both sides of the Atlantic. Monday saw banks wrap up a sale of leveraged loans and high-yield bonds to finance Clayton Dubilier & Rice’s purchase of a stake in a Sanofi SA unit.

“We have built in a slightly more defensive portfolio posture as we feel that credit spreads, particularly in the US, leave investors exposed to any potential bad news,” said Sriram Reddy, head of client portfolio management at alternative investment manager Man Group Plc. “There isn’t a specific trigger we are watching for — it could be a multitude of different factors that could push spreads wider, but the underlying currents are to slowing growth.”

Other market indicators show that worry is building, none more so than the amount of money being held in cash — over $7 trillion in the US alone. Gold, meanwhile, climbed through the roof to a new all-time peak above $3,130 per ounce on Tuesday. And indexes of junk-rated credit default swaps in Europe and the US, used to hedge against credit risk, are now up to their highest levels since August.

Gray swan risks picked out for 2025 by Nomura Holdings Inc. included a crash in Nvidia Corp. shares, 10-year US Treasury yields above 6% and a US growth shock.

Candriam’s Jullien reckons spreads still do not reflect the credit risk embedded in the high-yield market in general. As for the auto sector, he thinks credit ratings will need to be adjusted, including multi-notch downgrades in some cases.

“We could definitely widen to reflect higher risk of recession,” he said. “Some sectors that are highly exposed and sensitive to tariffs like autos could go into stressed territories.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Abhinav Ramnarayan