Banks from Wells Fargo & Co. to smaller Japanese lenders are flocking to top-rated collateralized loan obligation deals, pushing up secondary prices for buyout debt.

JPMorgan Chase & Co., Bank of America Corp. and Wells Fargo have been buying AAA rated CLO securities in bulk, three years after a market-wide pull back from such securities. The $1.3 trillion CLO market has welcomed renewed appetite from other buyers, such as Japanese firms JA Bank Osaka and Rakuten Bank, which are both deploying capital into CLO deals.

“The CLO AAA market is unique because it’s the only large floating-rate asset class rated AAA,” said Brian Pilko, the head of portfolio management and research at AGL Credit Management. “So if you’re a bank and looking to deploy billions of dollars in AAA, this is the best option.”

Demand for CLOs is helping to keep issuance of the securities high, close to last year’s record pace, even if there are few new leveraged loans to bundle into the bonds. Many of the loans for the bonds are coming from the secondary market, helping to keep prices on the debt relatively high. Investors snatching up the CLOs are betting that the floating-rate debt will pay relatively high yields as rates stay elevated.

For CLO managers, the steady stream of buyers interested in the top tranches helps guarantee they can put a deal together, given AAA pools make up about 60% of a deal.

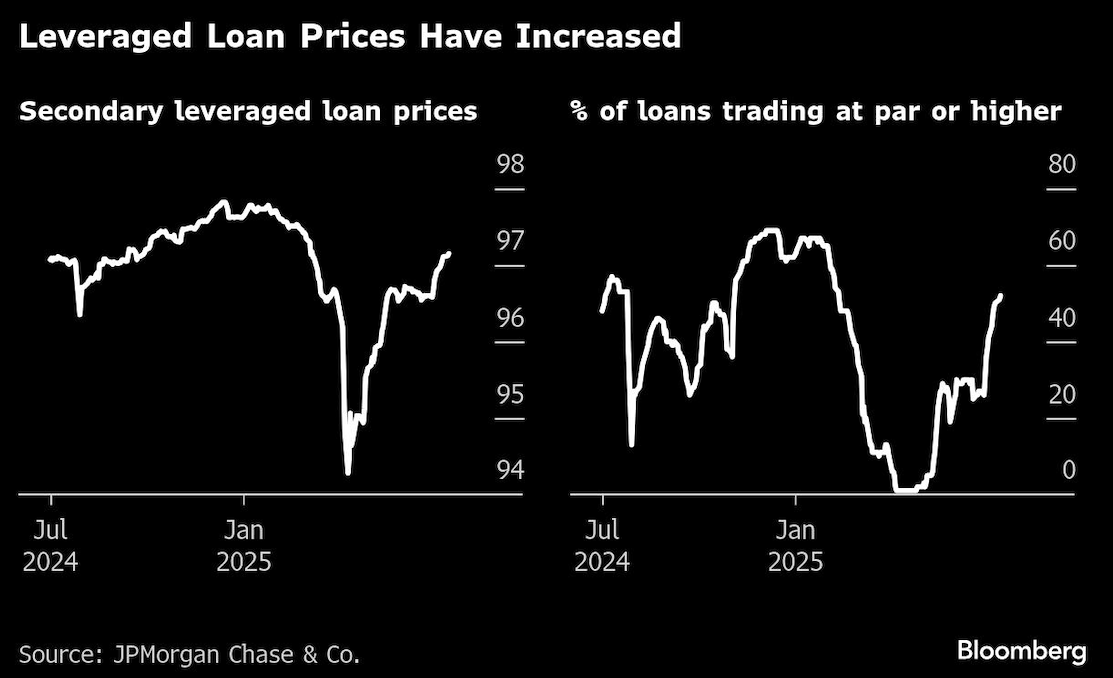

Avid buyer interest and a steady lack of mergers and acquisitions are pushing up leveraged loan prices, with half of the market trading above par, according to data from JPMorgan.

“There’s a lot of CLO supply and, for once, it seems like there’s enough of it to meet the demand, which means CLO spreads are not tightening,” said Ian Gilbertson, the co-head of US CLOs at Invesco Ltd. But at the same time, leveraged loans keep rallying because “every single manager is buying in secondary,” he said.

Wells Fargo has been willing to buy about half of AAA rated tranches on some transactions, while other US banks have been willing to gobble up almost 90% of the deals, market participants said.

Japanese banks SBI Sumishin Net Bank Ltd., JA Bank Osaka and Rakuten Bank are among those that have been holding conversations with CLO managers about buying up top-rated tranches of the securities, according to people with knowledge of the matter, who asked not to be identified discussing private information. Some of the banks have recently asked CLO managers for larger tickets in AAA rated tranches, said some of the people.

Bank of Fukuoka has already been buying CLOs, said a spokesperson for the bank, who declined to comment further.

Rakuten Bank is making limited investments in CLOs “with a strict set of conditions and with a focus on maintaining balance within its portfolio,” a Tokyo-based spokesperson said, declining to comment on the scale of the investments or future plans.

A spokesperson for Nochu, as agricultural bank Norinchukin Bank is known, said CLOs are a part of its “well-balanced portfolio in terms of overall risk.”

Representatives for JA Bank Osaka and SBI Sumishin declined to comment, while representatives for JPMorgan and Bank of America didn’t respond to requests for comment.

Retail Buyers

On top of the institutional investors, exchange-traded funds that buy CLO securities are also back in the market, after many offloaded billions earlier this year.

The ETFs have a record $32 billion of assets, according to data from Bank of America. While these vehicles primarily used to buy secondary deals, some are now buying new deals. Foreign-domiciled ETFs focused on US AAA CLO debt have also grown, such as Canada-based Mackenzie AAA CLO ETF, or Janus Henderson Tabula, which is incorporated in Luxembourg.

In 2022, interest rate hikes pushed most large CLO buyers out of the market, making it harder for money managers to issue the bonds. But, asset managers and insurers, who used to buy the more junior portions of the CLOs, are now also buying up the AAA rated debt.

Investor demand has pushed spreads on top-rated securities tighter since April, with deals pricing at about 1.3 percentage points over the benchmark. But they are struggling to tighten any further.

Despite all the enthusiasm for the top-rated portions of the bonds, CLO managers are still facing a dearth of buyout loans to buy. About 15% of US leveraged loan launches so far this year have been used to primarily help fund acquisitions, according to data compiled by Bloomberg, with the bulk of the transactions being either refinancings or repricings.

“CLOs can’t keep growing indefinitely if there are no new loans created,” said Pratik Gupta, who leads CLO research at Bank of America, adding that net issuance has been relatively low.

CLOs tied to broadly syndicated loans have been “driven by recycling old assets into new deals and extending existing transactions,” he said.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Carmen Arroyo, Rachel Graf