Americans place a premium on elite and exclusive institutions. Many of us want to get into top-tier universities, pledge storied fraternities and, upon graduation, attain membership at Soho House. And for most of recent history, we have also been more than happy to pay more for a stock just because it got into the prestigious S&P 500 Index — the Skull and Bones of corporate memberships.

Admittedly, that changed for about four or five years in the late 2010s, but human nature is now reasserting itself. My analysis of data going back to 2015 makes clear that the S&P 500 inclusion premium has risen from the dead. The resurrection bears the fingerprints of a newly influential group of retail traders who are changing the role of individual investors and making markets more unpredictable.

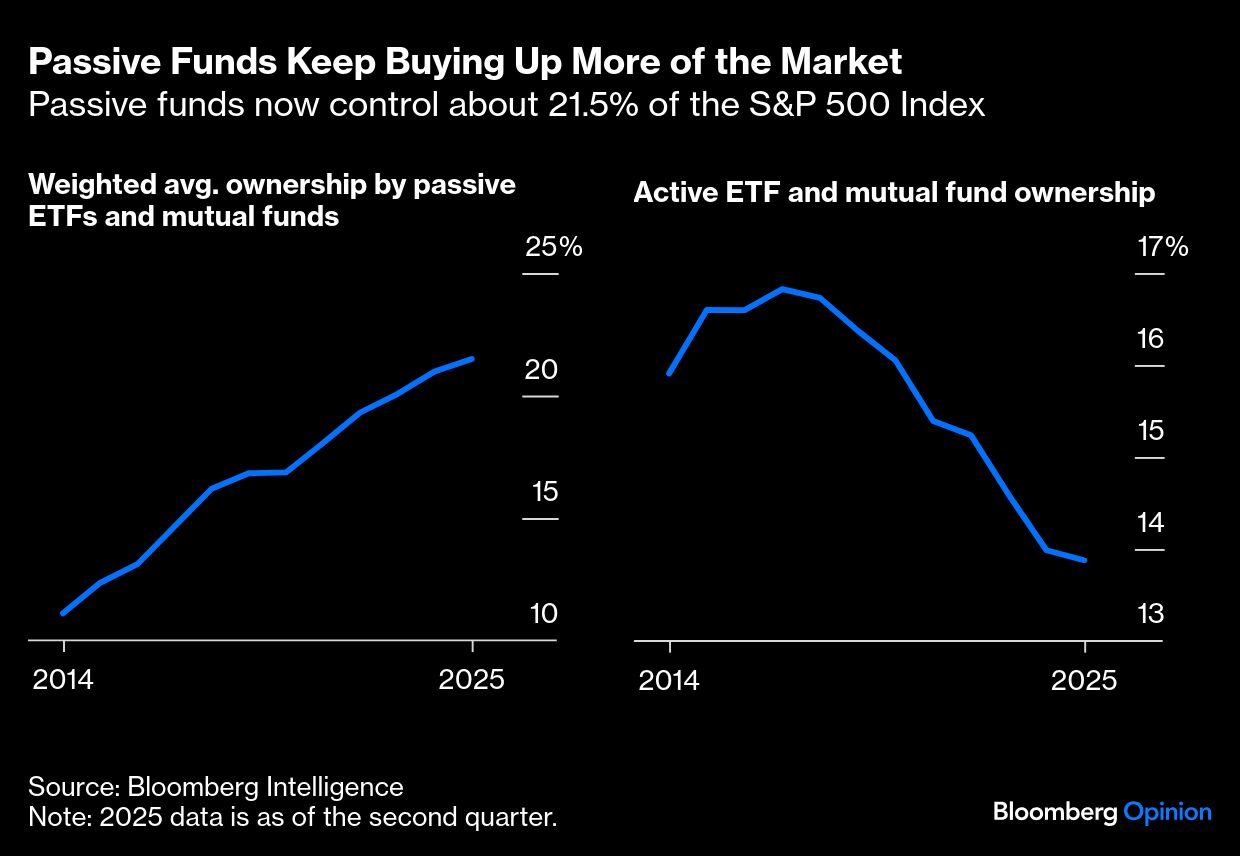

The essence of this is straightforward: Trillions of dollars in so-called passive investments are automatically allocated to the stocks in the S&P 500 through funds that track the index. Until the 2010s, this generally generated gains for the newbies, but by 2016 or so, the stocks in question barely seemed to budge when the index committee announced an inclusion.

A new academic consensus started to emerge that the effect was weakening or even vanishing — a victory for believers in efficient markets because S&P 500 membership doesn’t change a company’s fundamentals and thus shouldn’t change its stock price. (See key examples here, here, here and here.) Most intriguingly, this narrative took hold when the popularity of passive investing was soaring, making it a powerful rebuttal to those who claimed that passive flows would distort public markets.

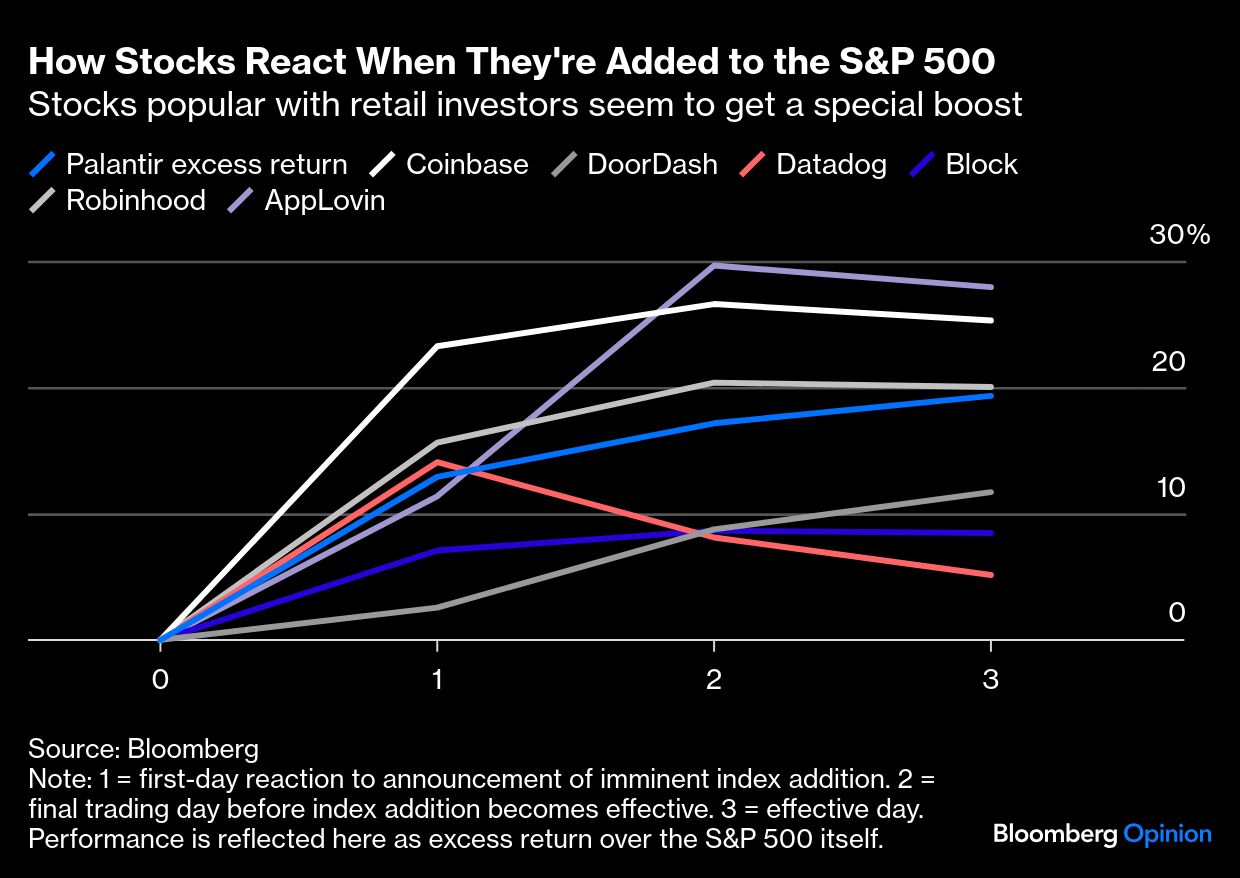

Now, the index effect is back with a vengeance, plainly visible in the S&P 500 debuts of companies such as Coinbase Global Inc. and Robinhood Markets Inc. But rather than point fingers at index-hugging investors, this latest twist seems part of a complex interplay with a new class of active retail investors whose influence runs alongside their passive brethren and is particularly pronounced when their favorite stocks are involved.

Instead of becoming more mechanical, the market is becoming more dynamic: Individual investors refuse to kick the trading habit they developed during the work-from-home days of the Covid-19 pandemic, enabled by zero-commission online brokerages and trade ideas crowdsourced from social media. The price movements they drive may not always be conventionally rational, but they’re nothing like the boring future many of us imagined with the proliferation of index-tracking mutual and exchange-traded funds.

It helps to first consider whether the ostensible death of the index inclusion effect was partially a statistical illusion.

For the former, index addition can feel like a highly predictable event that doesn’t change much. When these companies enter the S&P 500, mid-cap funds must ditch them while large-cap funds will add them, historically netting out to something of a nothingburger.

For the latter group, index addition can unleash a tsunami. About $23 trillion in assets is linked to the S&P 500, including $15 trillion of index-tracking products and derivatives and an additional $8 trillion of actively managed funds benchmarked to the index. In 2015, there were just $2.1 trillion in tracking assets and $7.5 trillion in benchmarked assets.

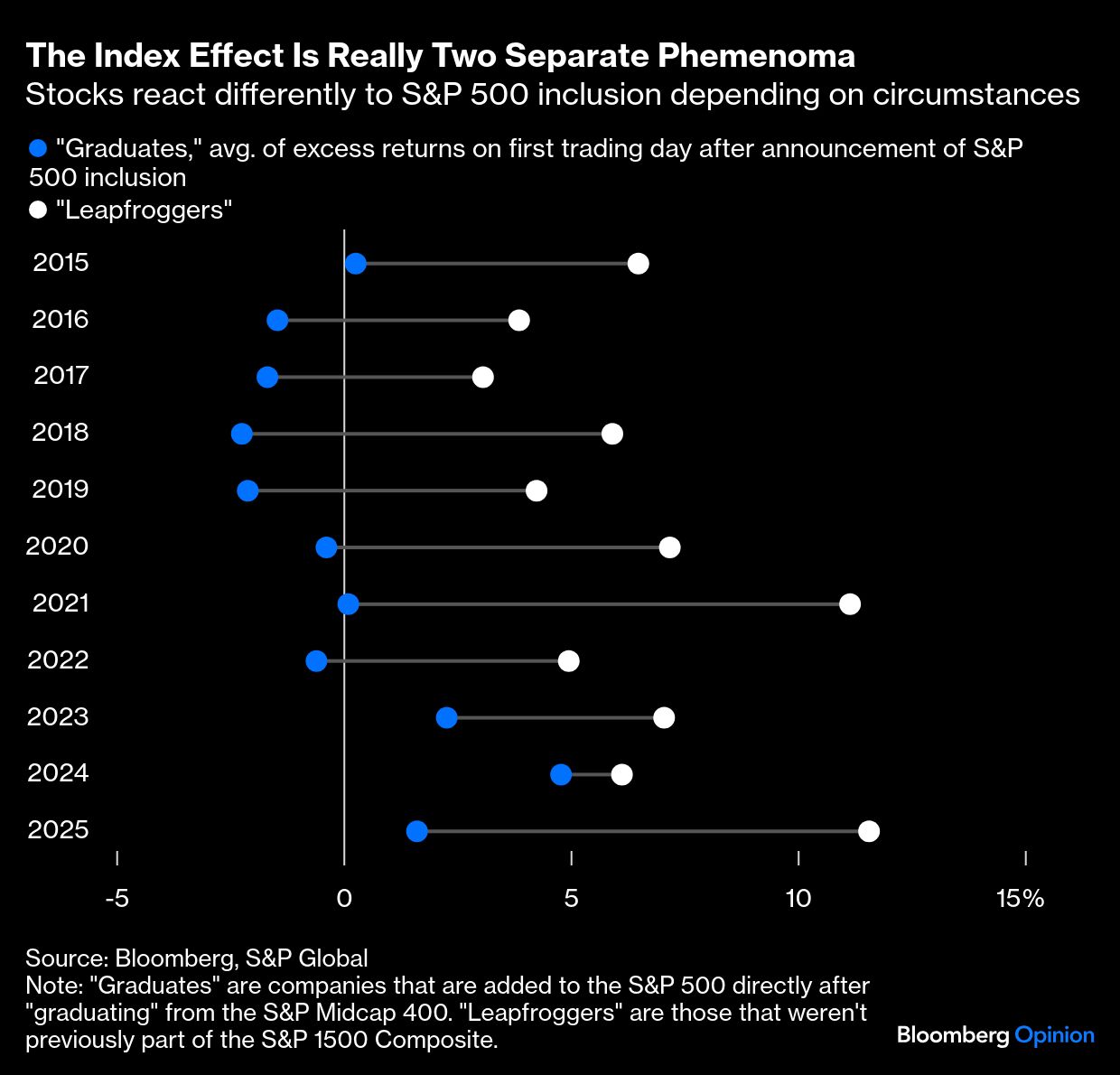

Clearly, the leapfroggers are the more exciting additions — and they deliver the most spectacular pops. The crop of leapfroggers depends in large part on the state of the IPO market over the previous one to four years.

In the 2010s, a lackluster IPO market following the financial crisis meant that there simply weren’t many exciting new companies around. The vast majority of additions were S&P Midcap 400 graduates. Arithmetically, that alone would have made it seem as if the index effect was weakening. Once people came to believe that the index pop was dying, they stopped treating it as a tradeable event — and then it really did go on life support.

There were exceptions, of course: Facebook (now Meta Platforms Inc.) delivered a one-day excess return of 5.3% when its inclusion was announced in 2013. Twitter Inc. (now X) had an excess return of 5% in 2018. But pops like those became the exception to the rule.

Then the IPO market surged back to life in 2021, and everything changed again.

The IPO revival coincided with a shift in market psychology. The watershed moment for this was Tesla Inc.’s 2020 addition to the index in the midst of the pandemic’s retail-trading mania. The stock had an excess return of 8.7% the day after the announcement and continued to rally broadly unabated for weeks. By the time Tesla joined the index a month later, its stock had climbed an extraordinary 70.3%, an excess return of 67.9%!

Clearly, elements of the Tesla story were unique, with the stock entering the index with a whopping 1.6% weighting. Yet the experience seems to have made index-effect believers of a whole new generation of asset managers and retail traders.

The post-announcement pops have more or less continued since. The shift is stark in my analysis of the data, which included 172 episodes of companies being added to the S&P 500 (not counting mergers and spinoffs). In the first half of the sample (2015-2019), the average pop was just 0.5% (median: -0.7%), but it has been 4% since 2020 (median: 2.7%).

And the stocks popular with the retail investing crowd almost always experience the biggest rallies. In recent years, the big winners have included Palantir Technologies Inc., Coinbase and Robinhood. Evidently, club membership doesn’t confer the same benefits on every stock, and it seems to matter most for the companies that were already popular with the retail crowd. For them, membership is a form of validation — a specious interpretation, in my opinion, but one that helps explain the explosive rallies.

Even more curious is what’s transpired with the graduates — a group that has historically fallen on news of index additions but now gains (see the third graphic).

For these graduates, the near-term benefits of S&P 500 membership are growing more stark as the index’s assets grow relative to the S&P Midcap 400 and S&P Small Cap 600. About 36 times as much money is indexed to the S&P 500 as the Midcap 400, up from around 22 times in 2019. Even if the heaviest-weighted mid-cap stock becomes the tiniest in the S&P 500, it’s still likely nowadays to receive significant net inflows from the move.

The behavioral quirks of social media-driven investing are clearly factors, too. Look no further than the 2024 addition of Super Micro Computer Inc., an announcement that produced an epic 18.7% next-day pop (an 18.8% excess return) despite Super Micro being a Midcap 400 graduate. At the time, it happened to be a popular retail play on the AI story.

Is some of this pure sentiment and borderline irrational? Possibly. The index effect was also quite strong in the late 1990s when internet companies were first debuting on the S&P 500 and investor enthusiasm about individual stocks was notoriously over-the-top. But even the post-announcement excess returns of Yahoo! (6.9% in 1999) and America Online (17.9% in 1998) pale in comparison to Coinbase’s 23.3% this year.

This is happening when retail flows into stocks have soared and are near records. In many cases, that’s been a positive development (it truly is “democratizing finance,” as the brokerage and ETF community claims). But it’s also, at times, enabling behaviors that look an awful lot like high-stakes gambling — which in turn affects how the market works for everyone.

Index additions and deletions shouldn’t — under an efficient-markets framework — have such a powerful impact on prices. To the extent that such anomalies exist, theory tells us that arbitrageurs will exploit them swiftly into nonexistence. For that reason, the death of the index effect was celebrated as a long-awaited victory for market efficiency. Others used the narrative to rebut concerns that passive investing was pushing equity prices away from their underlying values. Those takes will require some revisiting, though we seem no closer to resolution.

Rather, markets are a constant reminder to stay humble. Evidently, a new class of retail investors is changing the way the market works, and we’re all along for the ride.

A message from Advisor Perspectives and VettaFi: Gain exposure to the evolving digital asset landscape. Learn about CoinShares ETFs.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin