So far, President Donald Trump’s tariff policies haven’t induced quite the jump in prices that many of us feared. The latest inflation data was softer than anticipated and has locked in expectations for a couple of Federal Reserve interest rate cuts to close out 2025. But inflation is far from dead, and the labor market is far from collapsing — policymakers would be wise to proceed cautiously.

After next week’s rate adjustment, the Fed should prepare to pause in December to reassess the evolving economic landscape.

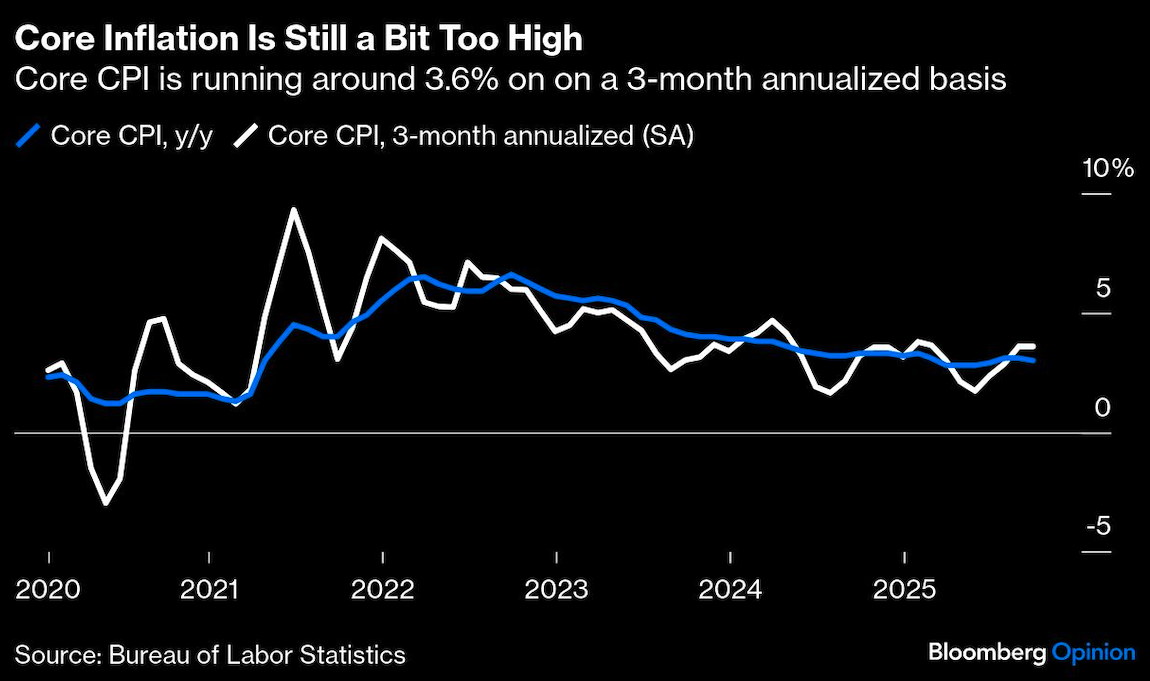

Take the latest data. On a month-on-month basis, the core Consumer Price Index — which excludes food and energy — was up just 0.2% in September, less than the 0.3% expected by economists in a Bloomberg survey. But on a three-month annualized basis, it is still running at around 3.6%, hotter than the 3% increase over the previous year. At a high level, inflation is still well above the Fed’s 2% target.1

Let’s start with the wonkiest but most important detail in Friday’s good-but-not-great inflation report.

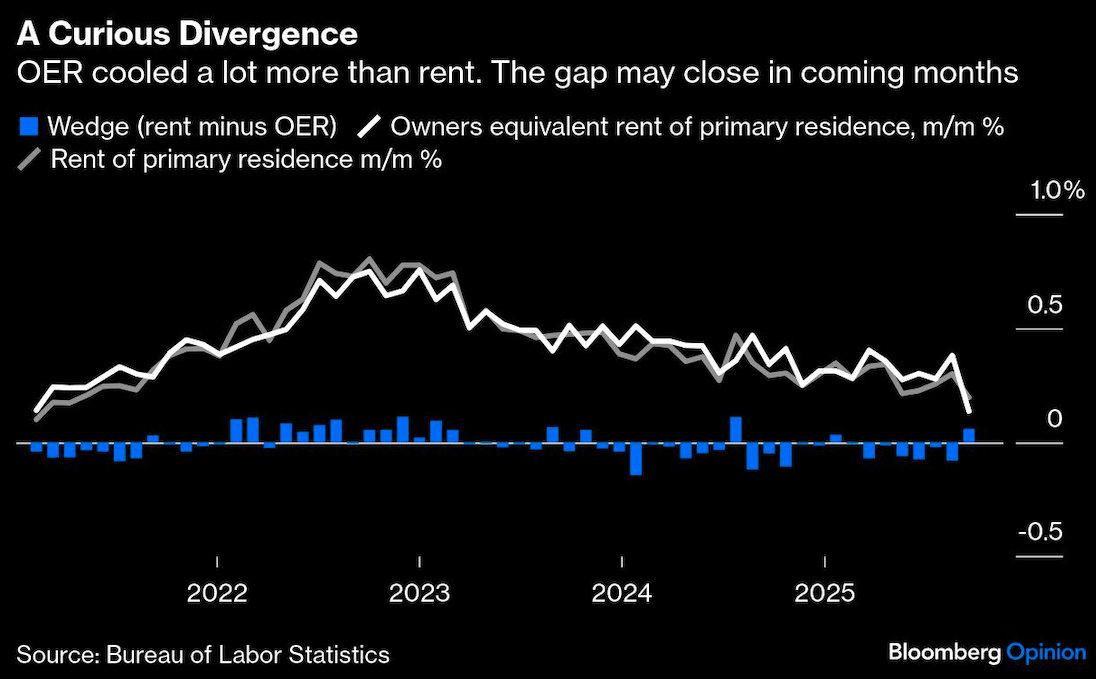

Housing was the key reason that inflation beat expectations in September. The “owners’ equivalent rent” category — a proxy for the inflation associated with homeownership that accounts for a whopping third of core inflation by weighting — rose just 0.1% from the previous month. That was a bit of a head-scratcher, because the OER figure is based on rents rather than actual home prices. And “rent of primary residence,” rose 0.2%.

“There is a big wedge between rent and OER that I suspect is almost certainly due to noise in the data,” Inflation Insights President Omair Sharif wrote in a note. “In that sense, this core reading almost certainly exaggerates the underlying inflation trend.” When it comes to shelter inflation, it’s important to hold two ideas in our heads simultaneously: Housing-related inflation really is cooling, but this number overstates the case. A snapback could easily embarrass an overeager Fed.

Next, there’s the question of tariff impacts. The core goods index — which includes such items as cars, apparel and washing machines — was up 1.5% from a year ago. Outside of the 2021-2022 spike, that’s the highest core goods inflation rate since 2012, so clearly tariffs are leaving their mark.

In the most recent month-on-month reading, it was apparel that stood out for its uptick. Here, economic orthodoxy would advise policymakers to “look through” one-time price shifts, and that may turn out to be the right course of action. But policymakers have to remain vigilant about inflation expectations and ensure that American households and businesses don’t start to assume that above-target inflation is becoming the norm. That could turn into a self-fulfilling prophecy and ultimately make inflation harder to root out. I’m not panicked about this possibility, but I don’t think we can take our eye off the ball. After all, Americans have now lived with this state of affairs for about five years.

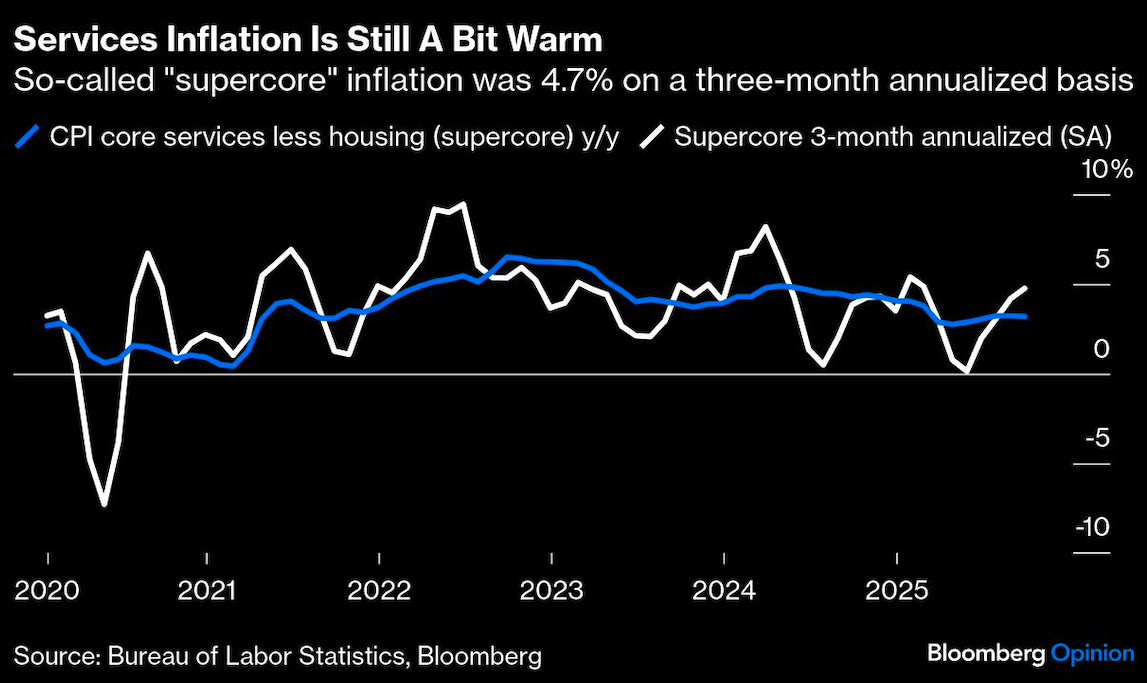

Finally, there are other core services, which continue to serve as the best rebuttal to claims that inflation is “only in tariffs.” In fact, this category should have nothing to do with Trump’s duties, and yet areas such as airfares and hotel prices have recently posted strong gains. On a year-over-year basis, the core services (excluding housing) category is now up around 3.2%. This shows that inflation would be a bit above target even without Trump’s duties.

To be clear, Friday’s report wasn’t alarming — it just wasn’t perfect. I’m comfortable with the Fed following through with the widely expected 25-basis-point rate cut next week to guard against risks to the labor market. But in order to make the case for more rate cuts, the committee will have to find further evidence that either inflation data is moving from so-so to pristine, or that the labor market is moving from so-so to bad.

On the latter, state data reviewed by Bloomberg Economics suggest that initial jobless claims were just around 227,000 in the week ended Oct. 18. Payroll additions have certainly slowed, but lower immigration flows are at least part of that story. The unemployment rate — the best all-in statistic — has been creeping higher, albeit at a glacial pace, which suggests that policymakers have time to move cautiously and manage risks to both sides of their stable prices and maximum employment mandate. Meanwhile, the labor outlook could find support from strong growth in gross domestic product and a stock market that continues to enrich many Americans — at least those at the high end of the income distribution.

There’s no question that policymakers are in a tricky position, and it won’t get any easier as the government shutdown drags on. When the shutdown began on Oct. 1, the Bureau of Labor Statistics had already gathered the inflation data for September. But the White House said Friday that the government probably wouldn’t be able to release inflation data for October. For the employment side of the mandate, the Fed may have a slightly easier time of replacing the missing statistics with private sector alternatives, but the October CPI will be sorely missed.

Given what we know about the economy today, policymakers would be well advised to slow down in this data haze. If anything, Friday’s CPI report made that even more clear than before.

1. The Fed technically targets PCE inflation, which hasn’t yet been released for September. But even there, inflation seems to be trending in the high twos for both headline and core.

A message from Advisor Perspectives and VettaFi: Ready for your next career move?Explore our articles on financial advisor transitions.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.