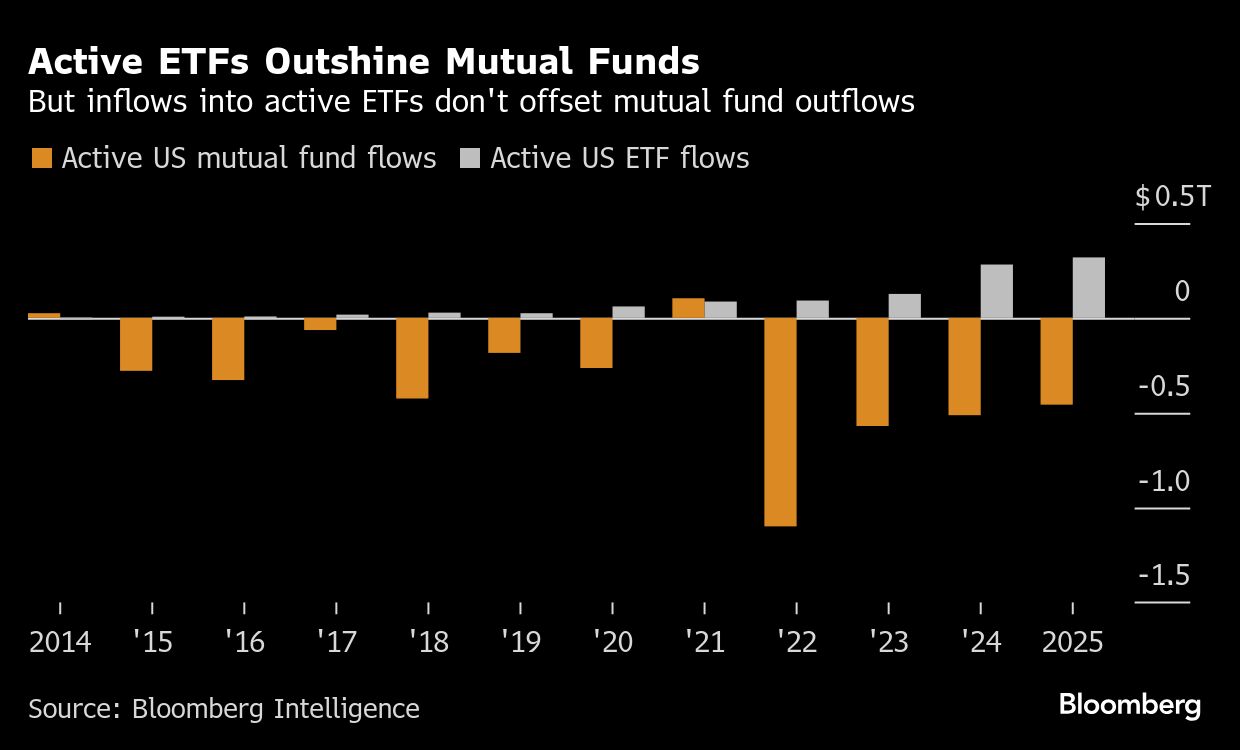

Investors are pouring money into active ETFs, but a closer look reveals a migration of assets into the wrapper instead of a resurgence in alpha-chasing bets.

Over the past five years, firms like Capital Group and Dimensional Fund Advisors have seen tens of billions in ETF inflows — just as their mutual fund complexes have lost even more. At Capital Group, $76 billion entered active ETFs while $294 billion exited mutual funds through the end of September. Dimensional flipped $125 billion in outflows into $135 billion of active ETF inflows in that timeframe, Bloomberg Intelligence data showed.

The two-way traffic suggests that this isn’t active management making a grand comeback — it’s largely investors shifting to the ETF wrapper from mutual funds. Advisers and platforms are swapping into the exchange-traded structure for lower fees and to minimize taxes. Among managers of active strategies, only JPMorgan seems to show genuine net growth, with both its mutual funds and active ETFs attracting new assets.

The result of the migration into the ETF wrapper is a less-than-perfect offset in at least some smaller categories. Families of so-called clones, which Morningstar Inc. defines as funds with 90% overlap in their holdings, have seen nearly $288 billion exit from active mutual funds since the start of 2020. Their ETF counterparts, meanwhile, have absorbed roughly $222 billion.

“Outflows in the overall active bucket are getting bigger. The ETFs are getting some flows, but it’s not reversing or slowing down the trend of money fleeing active equity funds in general,” said Jack Shannon, principal, equity strategies at Morningstar. “Even for the clones, it’s not a pure offset.”

It’s an asterisk on yet another banner year for actively managed ETFs, which have seen their share of the $13.2 trillion US ETF industry double in less than a decade, Bloomberg Intelligence data showed. A record $319 billion has poured into the structure year-to-date — shattering the previous high-water mark, which was set just last year. At the same time, nearly $458 billion has exited from active mutual funds so far in 2025.

Reality Check

The persistent net exodus from active funds is a potential brake check for legacy asset managers looking to dive into the ETF arena. Mutual fund shop Baron Capital filed for its debut ETFs in August after watching its assets decline more than 20% from a peak of some $59 billion in late 2021. Hedge fund Man Group Plc and centuries-old Pictet Group have joined the fray as well.

Even behemoth Vanguard Group, the second-largest ETF issuer, is leaning aggressively into active ETFs as industry-wide outflows beset the firm’s mutual funds.

Invesco Ltd. is facing questions as to whether its new ETFs are simply “cannibalizing existing wrappers” like mutual funds, as Autonomous Research’s Patrick Davitt asked executives asked during a recent earnings call. Chief Executive Office Andrew Schlossberg answered that it was unclear if that’s the case.

Capital Group’s Holly Framsted, meanwhile, said that growth of the firm’s ETF business has largely been fueled by “net new money,” given that the bulk of their mutual-fund clients are investing for retirement. Capital-gains taxes — which the ETF wrapper famously defers — don’t apply to 401(k)s, removing a key catalyst for why investors would jump from one structure to the other.

“About $2 trillion of our $3.2 trillion in assets under management are in mutual funds held within retirement accounts, which are already tax deferred,” Framsted, Capital Group’s head of product, said. “So it’s unlikely those investors are selling out of the mutual fund to invest in an ETF.”

A Dimensional spokesperson declined to comment.

A Litmus Test

In late September, the Securities and Exchange Commission indicated that it will soon allow Dimensional — and potentially dozens of other firms waiting in the wings — to offer ETF share classes of existing mutual funds. To Bloomberg Intelligence mutual fund analyst David Cohne, whether or not “cannibalization” is truly taking place will become clearer once US money managers begin offering such structures to investors.

“The ETF share class can smooth the transition, but it won’t guarantee net inflows — it only makes it easier for clients to stay if they still believe in the firm’s alpha story,” he said.

So far, not even outperformance has managed to stem the tide from mutual funds. Over the past five years, just 13.9% of more than 2,000 diversified active equity mutual funds have delivered “true alpha,” which Bloomberg Intelligence defines as annualized returns of at least 2% beat versus the benchmark. Despite the beat rates, investors still yanked a combined $55.2 billion from those top-performing funds over the past five years through September.

One area that’s attracting cash is non-index ETFs, such as leveraged single-stock funds, defined-outcome ETFs and yield-chasing covered-call funds. While such strategies don’t fit the typical mold of stock- and bond-picking funds, they still qualify as being active. That flavor of active management is clearly in vogue, while old-school managers making careful bottoms-up security selections continue to fall out of fashion, according to Morningstar’s Shannon.

“If you take the traditional view of active management — I’m paying this person to pick stocks to beat the market — that clearly is still in decline and isn’t being helped by the ETF in any material way,” Shannon said.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Katie Greifeld