Imagine I get extremely rich like Michael Burry on a contrarian short position. I’d immediately cash in my chips (but I wouldn’t tell anyone I was “semi-retiring” from the game). Then, after extracting some funds for fun and my kids’ education, I’d put 95% of my remaining winnings into a passive portfolio of stocks and bonds and marvel at the compounding.

But the real stroke of genius is what I’d do with the 5% left over: I’d use it to make bold (but relatively small) calls on the next big collapse to tempt the media into writing about me for the rest of time, thus burnishing my personal brand and giving me a free option to sell books, speeches, screenplays and whatever else.

Sounds familiar, right? I don’t know if that’s what Burry is up to — I’m strictly speaking for myself! — but he’s certainly proved that my plan can work.

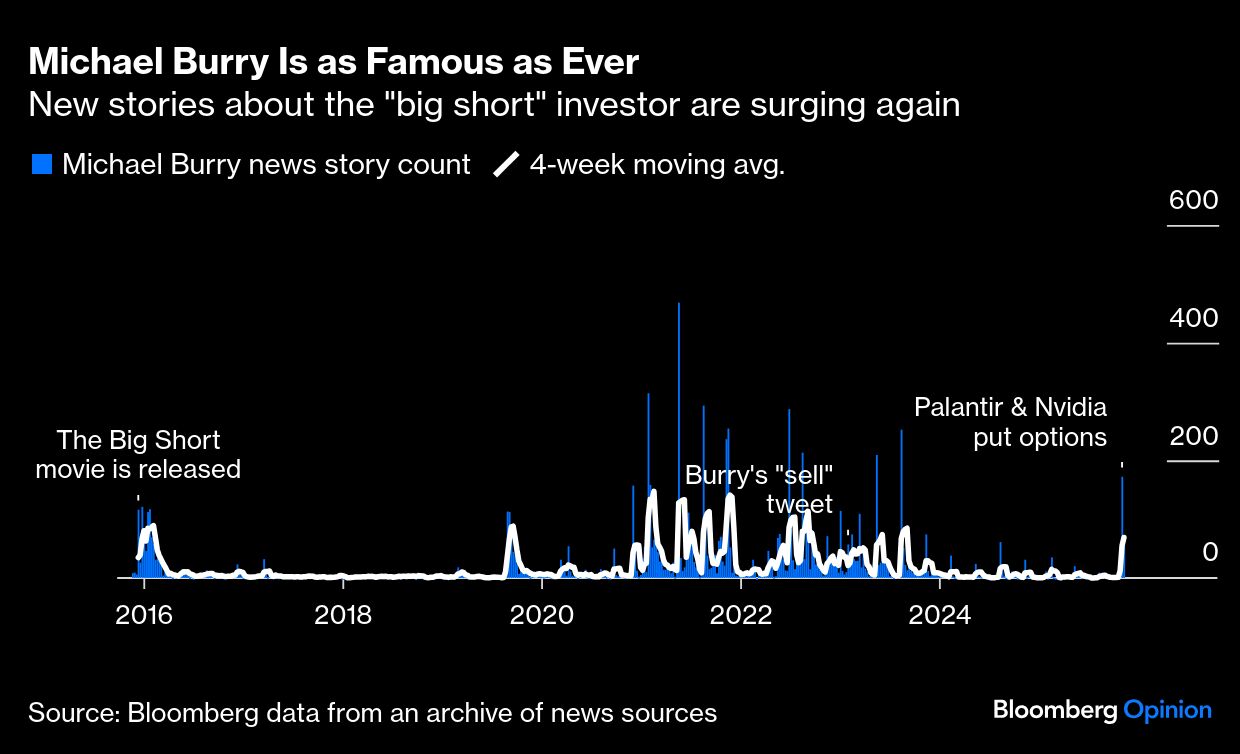

I bring this up because Burry, the investor who got famous for correctly betting against the US housing bubble, has been back in the news a lot lately.

- On Oct. 30, he cryptically posted a picture of his character in The Big Short movie to X, accompanied by the text “sometimes, we see bubbles.”

- On Nov. 3, in a 13F regulatory filing, his firm Scion Asset Management disclosed ownership stakes in put options tied to Nvidia Corp. and Palantir Technologies Inc.

- Later that week, he stayed in the news because Palantir CEO Alex Karp, a media darling in his own right, shot back at Burry for what he characterized as “batsh*t crazy” short bets.

- And then, on Wednesday, we learned that Burry’s fund had terminated its registration status with the Securities and Exchange Commission.

Huh?! In each case, there’s a ton that we don’t know. But one thing’s for sure: Burry is even more financial-media famous today than he was in 2015, the year he was portrayed by Christian Bale in the movie-version of Michael Lewis’s The Big Short: Inside the Doomsday Machine. That, in turn, tells us more about ourselves than Burry — we’re obsessed with contrarian investors that make concentrated “hero bets” on macro outcomes, and our fascination has only grown as an artificial intelligence boom pushes valuations ever higher.

That’s understandable. For the millions of households who have missed out on the Nasdaq-100’s 113% return since the release of ChatGPT, it’s reassuring to hear a legendary investor hint that the winners are about to get their comeuppance. For the millions of others who’ve participated in the rally, there’s a growing anxiety driven by the simple belief that your luck eventually runs out. Everyone has been forced to engage with one key question: Are we in a bubble? The empirical data offers few satisfying answers and so, we anchor to enigmatic social media postings from a guy who got it right once before.

It’s extremely hard to parse out a holistic and fair report card for Burry in recent years. Going back to his alleged big short on AI stocks Nvidia and Palantir, recent news suggests that it may not have been what it initially seemed. For instance, Burry clarified that he had spent $9.2 million on options to sell Palantir at $50 in 2027 (it trades today at $174), but some news chyrons focused on the vastly larger and more sensational notional value.

As Bloomberg News’ David Marino wrote Thursday, the original filings leave much to the imagination, in part because of the conventions for reporting on such options. As Scion’s 13F discloses in the footnotes, put positions may also “serve to hedge long positions which are not eligible to be reported.” So, to borrow from Marino’s excellent headline, 13Fs “are more like travel diaries than investing road maps.”

As a more general matter, we don’t know enough about Burry’s recent performance record to believe that he’s someone we want to emulate. His fund had around $155 million in regulatory assets under management as of this year, which is quite unspectacular by today’s standards. It’s also less than half of the $387 million in RAUM that it reported five years ago and a quarter of what Burry reportedly managed in the 2000s. We don’t know why the fund is smaller today by this metric — and there are many potential pitfalls in interpreting Form ADV data from the SEC — but it’s safe to say that Burry is no Warren Buffett (in fact, Buffett has long advised against the sort of market timing that Burry engages in).

Likewise, I’m not sure that over-extrapolating from Burry’s X posts is wise, since his social media commentary has been... spotty. In the bear market month of September 2022, he posted, “No, we have not hit bottom yet.” And while he wasn’t totally wrong — it wasn’t the precise bottom — the next bull market would start only a few weeks later. Then, in January 2023, he told followers in a one-word-no-context tweet to “sell” (presumably stocks? everything?), and the S&P 500 Index proceeded to return around 75% ever since.

I appreciate anyone who sticks his neck out with bold calls, and I understand that we’re all ultimately mortal. If I had nailed a macro call early in my career and was lionized in a Hollywood movie, you better believe I’d be milking it for decades with teasing tweets and hard-to-interpret 13Fs. For his part, Burry’s latest social media post claims he’ll be “on to much better things Nov 25th,” whatever that means. I just hope that Burry’s 1.5 million X followers are able to put all of this in its proper perspective.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin