For Elon Musk, the public market debut of SpaceX could hardly have gone better. It priced at the dictated $135 per share and has since jumped by almost half, adding more than $870 billion in just three trading sessions to an already huge market capitalization. At $2.64 trillion, Space Exploration Technologies Corp. rivals Amazon.com Inc., the far more profitable technology giant whose chairman is Musk’s great rival in rockets, Jeff Bezos. Along the way, Musk has become the world’s first trillionaire.

SpaceX has also well and truly eclipsed Musk’s other company with a gravity-defying stock, Tesla Inc. If the present trend holds, that should make it much easier for Musk to merge them into one sprawling, listed, multitrillion-dollar empire, potentially rivaling Nvidia Corp. for the title of the world’s most valuable listed company.

Musk’s assiduous melding of narratives at the two companies, centered on artificial intelligence, provides a strong rationale for him to combine them, as does his evident desire for greater control over Tesla and that company’s faltering growth and imminent cash burn (I wrote about all this here). That logic, and Musk’s dominant role at both companies, creates a potential conflict of interest because it would advantage the likely acquirer, SpaceX — where Musk has far greater control and now derives the vast majority of his net worth — if Tesla became relatively cheaper.

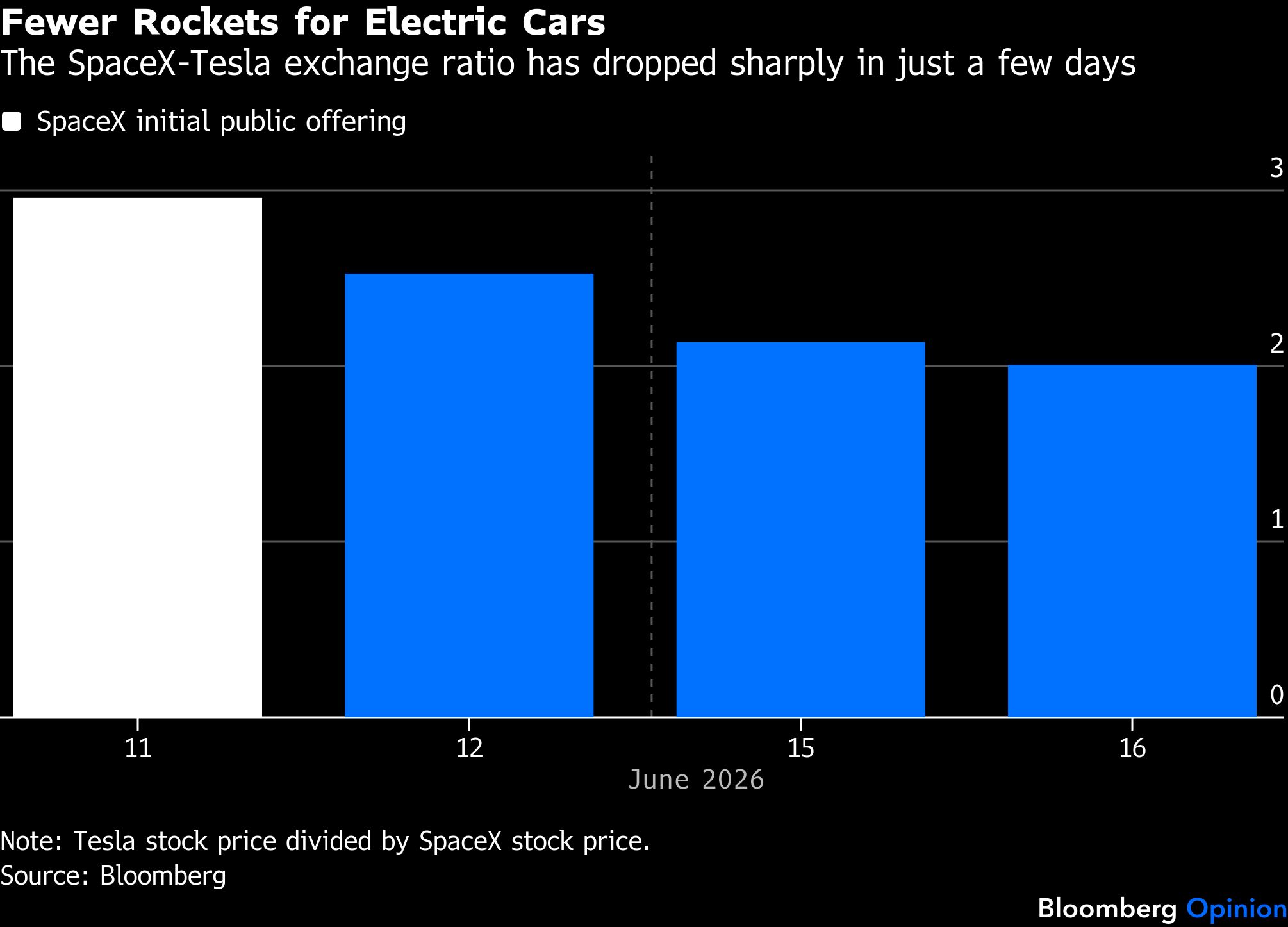

The market is doing that job already, and quickly. These are early days for SpaceX stock, of course. Its current price is even less tethered to reality than is usual for a Musk-led company given the confluence of its limited free float ahead of lockups expiring, the start of options trading, plus lingering IPO hype before any formal results. Still, if SpaceX’s relative ascendence versus Tesla holds, it would smooth an all-stock deal.

The exchange ratio, which shows how many SpaceX shares would need to be handed over to cover one Tesla share, tells the story. That number has fallen 32% already. SpaceX was valued about $266 billion more than Tesla when it priced. That has widened to $1.1 trillion.

A gap like that represents an open invitation for consolidation.

A critical aspect of such a deal, perhaps the key aspect, would be Musk’s resulting level of control. He has an iron-clad grip on SpaceX already — with a dual-class structure giving him 84% voting power at the IPO — and a much lower stake in Tesla, below 20%, including restricted stock units. Given that, the greater the valuation gap in favor of SpaceX, the higher Musk’s control of a combined company.

By my reckoning, SpaceX could offer Tesla a one-third takeover premium on its current price, and Musk might still end up with pro-forma voting control of about 74%. This would imply a valuation for Tesla of just more than $2 trillion, which could go a long way to persuading shareholders to vote for it, especially given the company’s deteriorating financials. It would also provide Musk the added bonus of unlocking the first tranche of his $1 trillion compensation package at Tesla — the rest would disappear — which would convert into more SpaceX shares. All else equal, and with the big assumption that SpaceX’s own price remained resilient, such a deal would come with a headline valuation of almost $5 trillion, rivaling Nvidia’s market cap.

In any normal situation, a cash-burning company buying another cash-burning company at a premium, and both of them run by the same person, would trigger a selloff and shareholder revolt. At roughly $2 trillion, SpaceX would be paying 138 times forward Ebitda for Tesla, and the position of SpaceX’s other shareholders would be diluted from around 50% to less than a third.

But none of this is normal — we’re talking about the biggest IPO in history, for a loss-making company, and then nearly $900 billion added to the market cap in three days. SpaceX investors not named Elon Musk happily signed up already for a shareholder structure that makes their Class A position essentially powerless when it comes to votes.

They were also fine with SpaceX having paid $250 billion for Musk’s other side gig, and cash furnace, xAI. Tesla shareholders have more control in theory, but Musk’s centrality to the value of their stock, along with a supine board, mean the reality is somewhat less than the theory. And while we haven’t got details yet, there is almost certainly a sizable overlap in the two companies’ investor bases, which may explain the relative pressure on Tesla shares as some liquidate those holdings to fund SpaceX purchases.

If the early trading is telling us anything, it’s that Musk’s fans want him to get the gang together and rule it untrammeled.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Liam Denning