A violent rotation in the underbelly of a bullish stock market is extending the worst run for quantitative hedge funds since 2023.

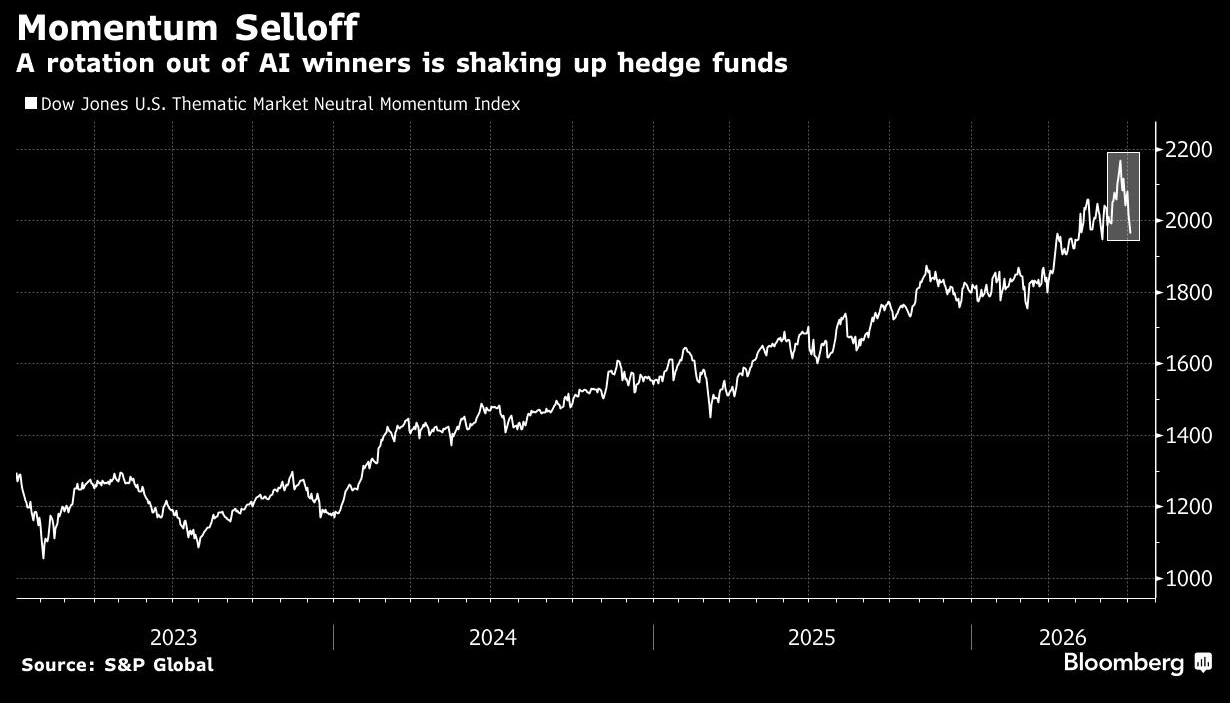

A long-short momentum strategy, which buys recent equity winners and sells losers, dropped more than 3% for a second straight week, an S&P Global index shows, taking its two-week loss to the worst in more than three years.

Systematic long-short managers dropped 2.1% last week through Thursday, after declining 3.1% over a five-day stretch that was their worst since December 2023, according to Goldman Sachs’s prime brokerage. Fundamental managers also fell last week as hedge funds cut leverage, with tech among the most-sold sectors.

The S&P 500’s steady gains last week belied a drastic shift under the surface that’s shaking up stock pickers. As the AI trade lost steam, with high-flying chip names like Micron Technology Inc. sliding, stodgier and cheaper stocks have rebounded again.

“Momentum volatility, now running hotter than the dot-com era, is flushing out hedge funds with VAR limits and retail traders chasing breakouts,” Jordi Visser, the head of AI Macro Nexus Research at 22V Research, wrote in a note, referring to value-at-risk calculations commonly used in risk management.

Read more: Momentum Selloff Raises Question About Next Step: Equity Insight

A widely followed quantitative factor known for its epic crashes, momentum often overlaps with crowded winning trades — such as major AI beneficiaries in this case. Before this recent selloff, the S&P momentum index had rallied for nearly three straight years to reach the highest in data going back to 2002.

While gross leverage in high-momentum stocks has dropped, it remains elevated on a two-year basis, “leaving positioning still vulnerable to further unwind,” according to a note from UBS Systematic Advisory last Thursday.

The latest quant unwind comes after a year in which computer-driven funds have largely done well but suffered a few notable — and occasionally inexplicable — drawdowns, including last summer and early January. Unlike those episodes, which were triggered partly by a junk rally, the backdrop has been different this time, as low-volatility shares rebounded.

Even with the recent pain, systematic managers are still up about 11.1% this year, while their fundamental peers have added nearly 16%, Goldman data show.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Justina Lee