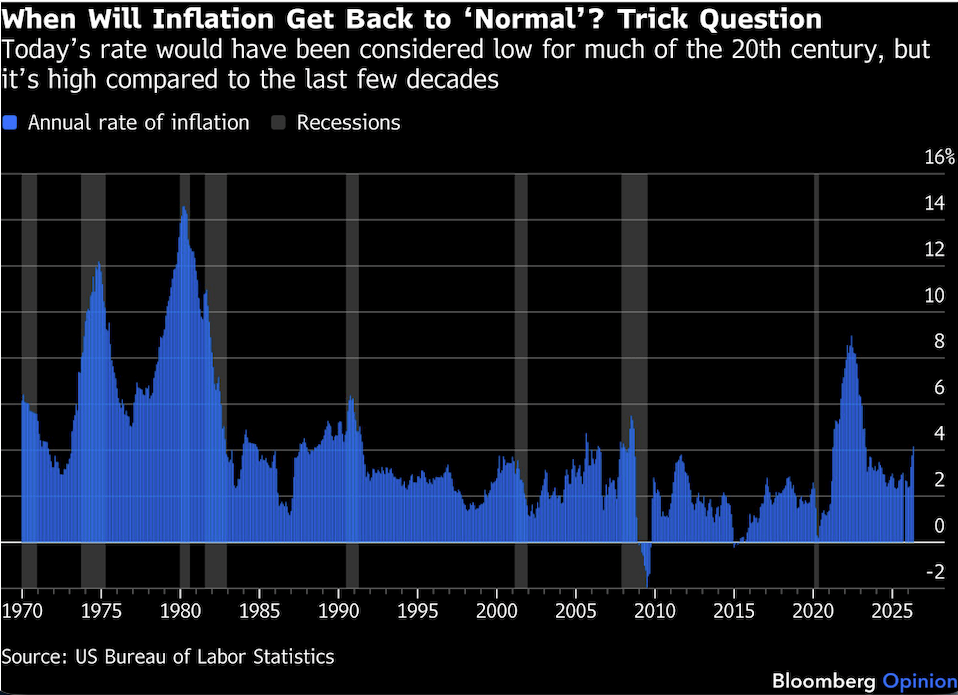

The US Bureau of Labor Statistics said Tuesday that the Consumer Price Index fell 0.4% in June, bringing the inflation rate over the past 12 months down to 3.5%. That’s good but not good enough. Inflation is still too high. Even with the drop in June — which was due in no small part to falling gasoline prices — inflation has averaged 3.8% over the prior three months, almost double the Federal Reserve’s target of 2%. Neel Kashkari, president of the Minneapolis Fed, recently said what everyone knows: People hate inflation, which they have been dealing with for more than five years, and every time they go to the grocery store they “feel they are falling further and further behind.”

No lie there. When wages don’t keep up with inflation, people suffer because they are effectively poorer. Just as bad is the unpredictability: When they go shopping, people don’t know what things will cost. In finance, an asset with a more variable return is worth less. Unpredictable inflation does the same thing to incomes. Inflation adjusted average hourly earnings have fallen 0.33% over the April, May and June period, versus an average gain over the past 20 years, according to data compiled by Bloomberg.

But while everyone can agree that the rate of inflation is too high and too uncertain, no one wants to admit that this may be the new normal.

It is easy to forget, but it wasn’t that long ago that policy makers wanted 3% to 4% inflation. For much of the 20th century, that level would have been considered a policy success. Then, for most of the 2010s, the inflation rate was below target, near zero, and it seemed too low.

This left central bankers almost impotent to influence the economy. Back then, many policy makers and economists thought 4% inflation was better than 2% because it allowed monetary policy more room to be effective. Businesses also didn’t mind, because higher inflation allowed for stealth wage cuts: When there’s high inflation during a recession, firms can decrease their labor costs just by not giving raises. That may sound bad, but it’s better than layoffs.

The world is now getting a brutal reminder of how much people hate inflation. It not only makes them poorer but, unlike unemployment, it also affects everyone all at once. Any healthy economy has some inflation — it is a sign of growth — but ideally it is in the sweet spot: moderate, predictable and tolerable.

But what exactly is moderate and tolerable? A rate of 4% or even 3% feels high because it is significantly more than 2%. After almost 20 years of low inflation, expectations have changed; now people expect inflation to be so low they don’t have to think about it. Those expectations get baked into pay raises — so even when the economy is booming, 4% inflation sets a higher bar for wages to keep up. And while stealth wage cuts may be useful when the job market is terrible, the rest of time they are awful. A higher rate also leaves more room for variance, and the accompanying uncertainty can be just as destructive as the level of inflation. Finally, higher inflation also means higher and more variable interest rates, which introduces more risk into financial markets and increased the cost of capital.

If economists have learned anything in the last few years, it might be that inflation of more than 2.5% is much worse than we thought. That’s unfortunate, because the Fed may not be able to return inflation to that level.

The bank has been saying for years that inflation rates would fall back to target, and it hasn’t happened. Yes, there have been policy shocks — a pandemic, wars, tariffs — but those are a fact of life. The low inflation of the 2000s and 2010s could have been a result of deflationary pressures from technology and globalization, which may not be repeated. In fact, an aging population could mean more inflation. And once inflation expectations take hold — whether for less inflation, as they were for much of the aughts and teens, or for more, as they are now — they can be hard to dislodge.

A world with an inflation rate of 3% to 4% poses many challenges. For one, the Fed is still promising it can get inflation back to 2%. If it fails, its credibility suffers, as does its ability to conduct monetary policy in the future. For another, higher prices are a real burden for households, especially if wages don’t keep up.

Finally, for not only central bankers but also other policy makers, higher inflation complicates other risks they are trying to manage. Some expect prices to moderate if the price of oil stabilizes, or if AI makes the economy more productive. That may well happen, but it’s starting to feel like wishcasting.

Not too long ago, many economists thought overshooting the Fed’s inflation target of 2% might be better than falling short of it, or that the target should be 3% or 4%. We all should have known how good we had it.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

More Innovative ETFs Topics >