Last week's economic reports painted a stark picture of rising inflationary pressures and plummeting consumer confidence, casting a shadow over the U.S. economy and sending the stock market into a decline. The Federal Reserve's preferred inflation gauge, the PCE Price Index, unexpectedly accelerated, reinforcing concerns about persistent price pressures.

Simultaneously, consumer sentiment, as measured by both the Conference Board and University of Michigan indices, plunged to multiyear lows, driven by heightened anxieties over economic policies, rising prices, and future economic prospects. Despite positive GDP figures from late 2024 and continued home price growth, the prevailing sentiment is one of caution, leaving markets and policymakers navigating an increasingly uncertain landscape.

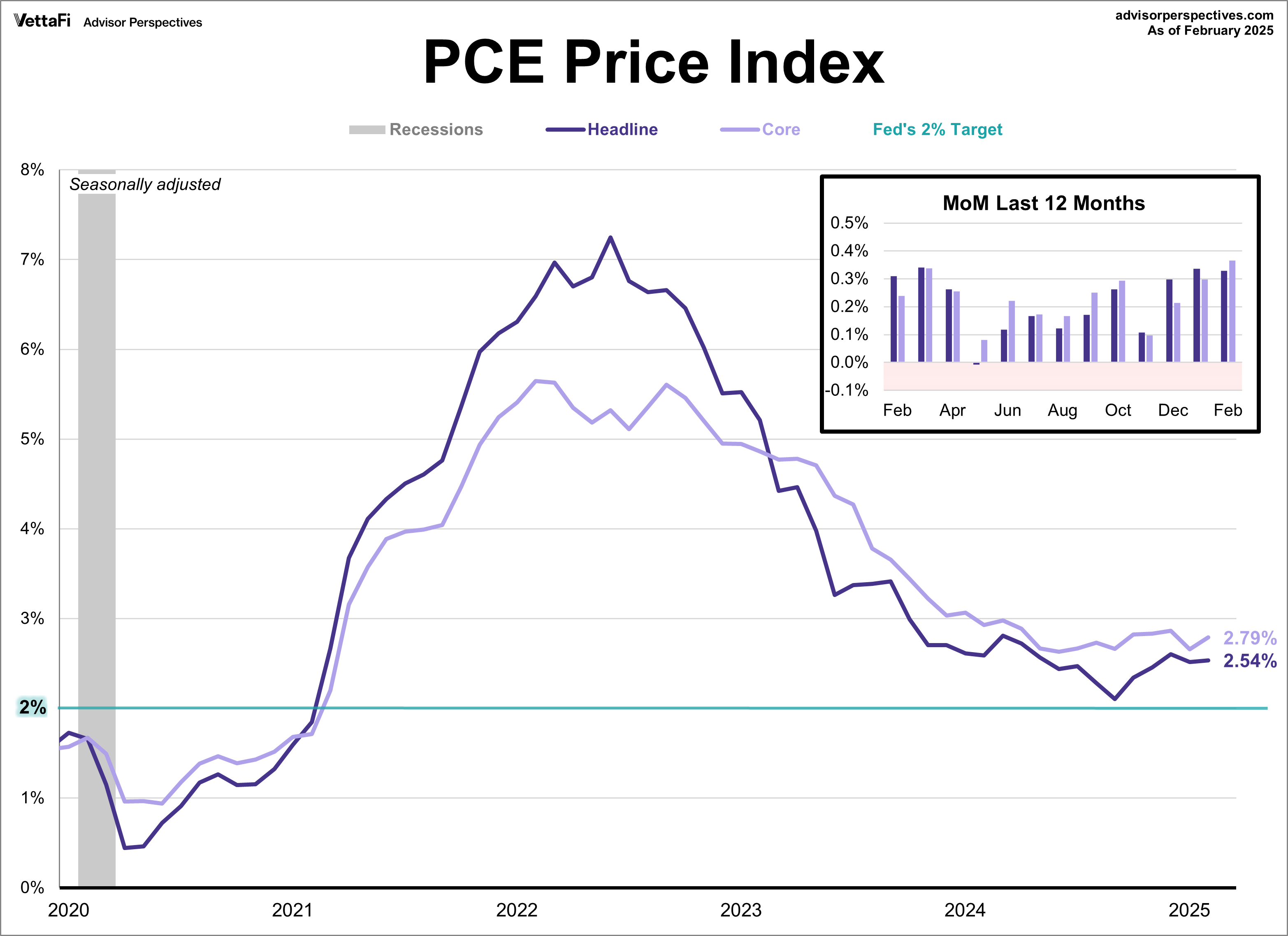

PCE Price Index

Inflation, as measured by the Federal Reserve's preferred metric, unexpectedly heated up last month. The Core Personal Consumption Expenditures (PCE) Price Index, which excludes volatile food and energy costs, rose 2.8% year-over-year in February, higher than the expected and a pickup from January’s 2.7% growth. On a monthly basis, core prices also came in above forecasts, increasing 0.4%. This is the largest monthly increase since January 2024. Meanwhile, the headline PCE Price Index saw a 2.5% annual increase, unchanged from January. Monthly, the headline index also rose by 0.3%, as predicted. The latest report continues to support the Fed’s “wait and see” approach as inflation is proving sticky amid ongoing economic uncertainty.

Consumer Attitudes

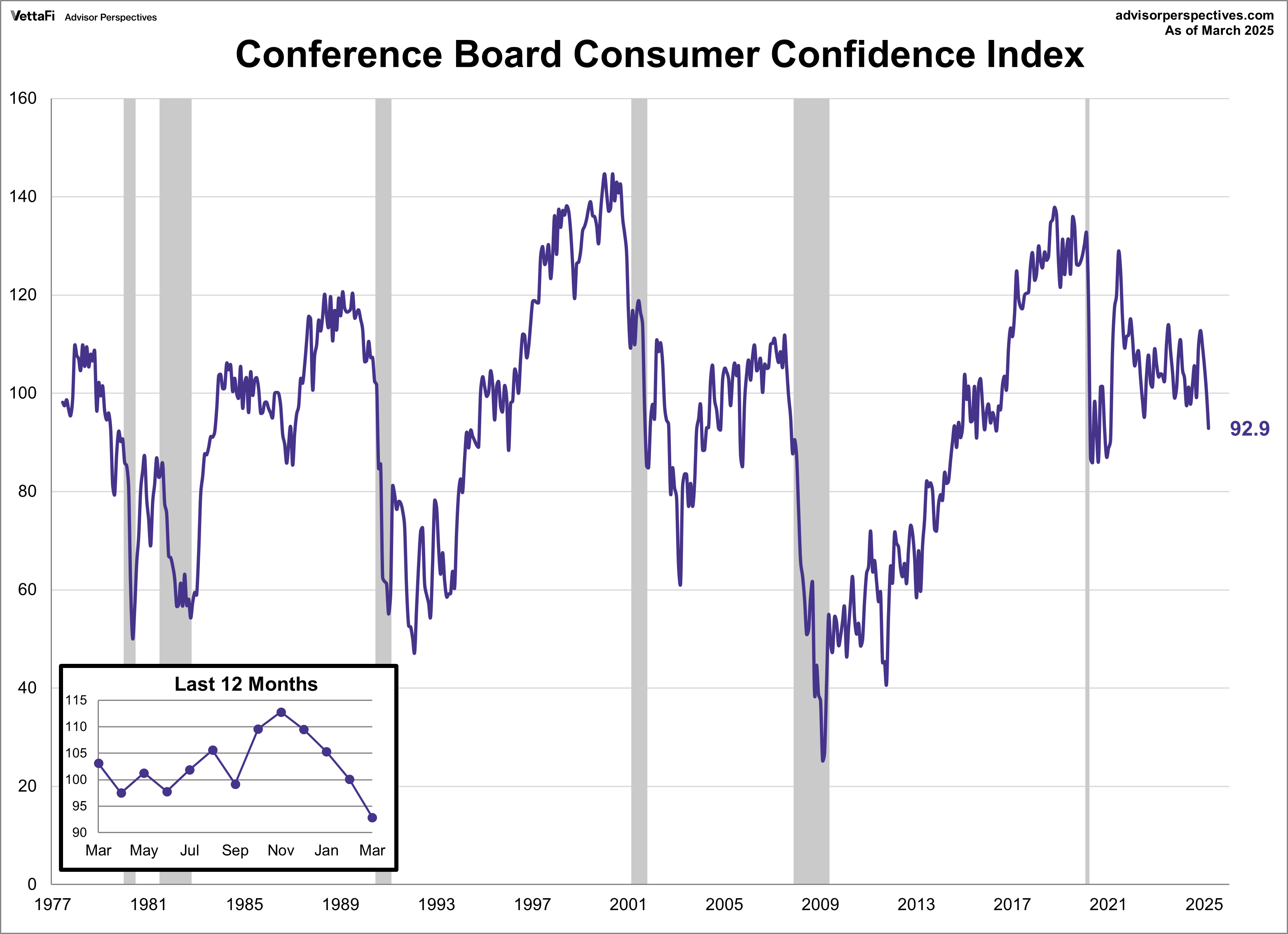

Conference Board Consumer Confidence Index

The Conference Board Consumer Confidence Index experienced a significant decline in March, falling for the fourth consecutive month to a four-year low of 92.9. This 7.2-point drop — the largest since August 2021 — missed the expected 94.2, and represents the longest period of monthly declines since 2012. The index has also moved outside its previously stable 10-point range maintained for the past 3 1/2 years.

The index, based on a monthly survey of consumer attitudes regarding present and future economic conditions, revealed worsening sentiment across four of its five components. The Future Expectations index saw the most dramatic decline, reaching a 12-year low. Consumers are increasingly pessimistic about future business prospects, employment opportunities, and income levels, which had previously remained relatively resilient. Within the Present Situation Index, views on the labor market improved marginally, but perceptions of current business conditions deteriorated. Inflation remains a key concern, with 12-month inflation expectations rising to 6.2% in March, fueled by high prices for essential goods and the impact of tariffs.

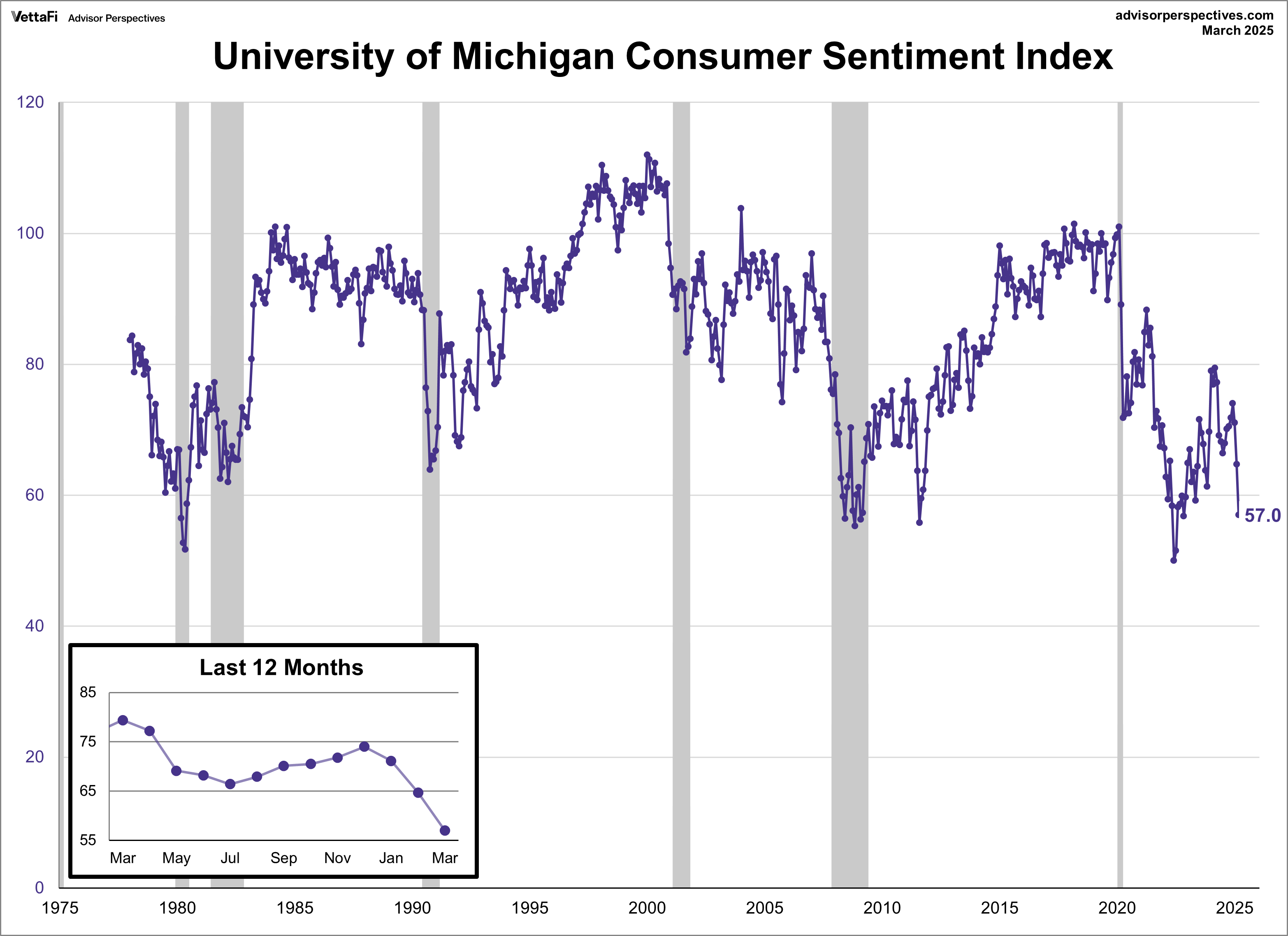

University of Michigan Consumer Sentiment Index

Consumer sentiment declined for the third straight month, as consumers continue to express concerns surrounding economic policy. The Michigan Consumer Sentiment Index fell 7.7 points to 57.0 this month, its lowest level since November 2022. This represents an 11.9% decline from February’s final reading and a 28.2% drop from one year ago, the largest annual decline in nearly three years.

The current conditions index remained somewhat stable, while the expectations index experienced its sharpest one-month decline since 2012, falling to a 32-month low. Consumers across all demographics and political affiliations expressed worries about the potential impact of ongoing economic policy developments. Specifically, the number of consumers expecting unemployment to rise in the next year hit its highest level since 2009.

Inflation expectations continued to rise for both the near and long term. Year-ahead expectations rose for a fourth straight month to 5.0%, the highest level since November 2022, while five-year expectations jumped to 4.1%, the highest since 1993.

The Consumer Discretionary Select Sector SPDR ETF (XLY) is tied to consumer confidence.

Gross Domestic Product

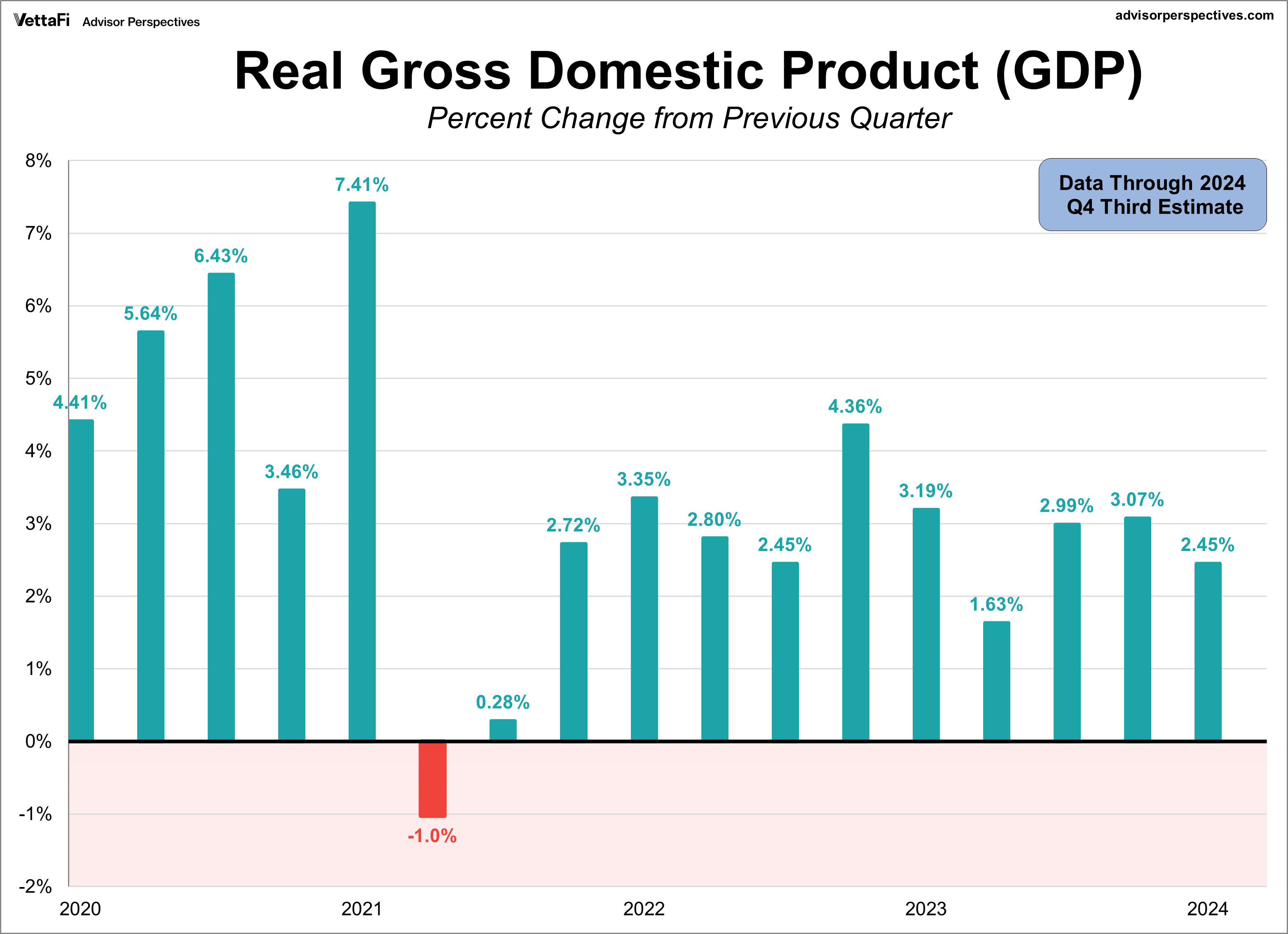

The U.S. economy ended 2024 on a positive, hitting its 11th straight quarter of expansion. According to the third estimate, real GDP — the inflation-adjusted measure of all goods and services produced in the U.S. — expanded at an annual rate of 2.4% in Q4. Although this reflects a slowdown from Q3's 3.1% growth, it was faster than previously estimated.

In Q4, three of the four components made positive contributions to real GDP. Consumer spending continued to be the primary driver behind last quarter’s expansion although, it was downwardly revised at each estimate. Government spending also helped drive growth at the end of 2024, while a decline in business investment partially offset these gains. Lastly, net exports made much larger positive contributions than previously reported to round out the year.

The big question is if economic growth will be sustained in Q1 of this year. As explained earlier in the article, consumer confidence has taken a hit in the first three months of 2025, which could lead to lower spending and ultimately drag down economic growth.

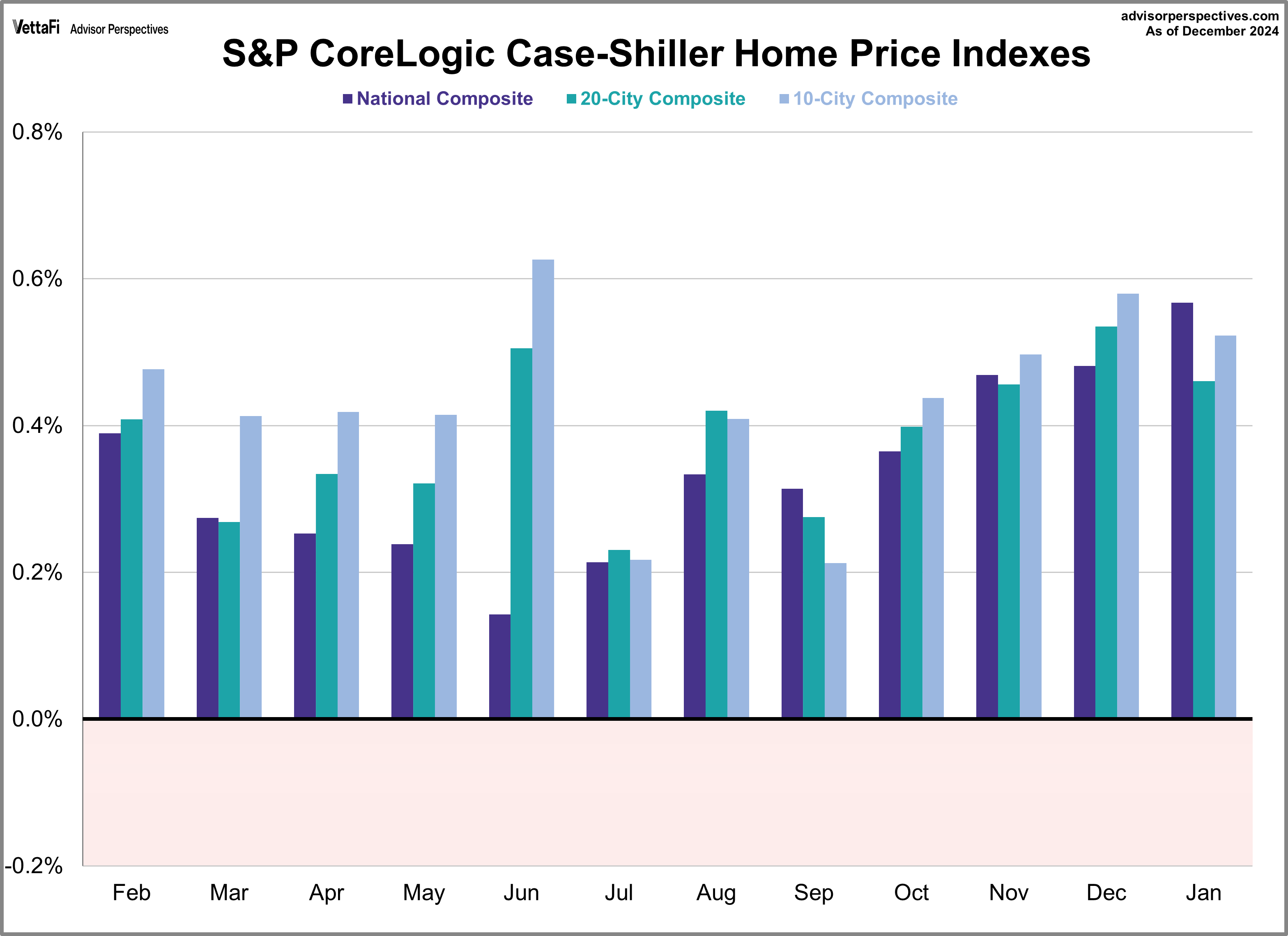

S&P CoreLogic Case-Shiller Home Price Index

The S&P CoreLogic Case-Shiller Home Price Indices, used to benchmark U.S. housing prices, showed continued growth in January. The National Home Price Index had its 24th consecutive monthly increase and its 19th straight record high. It rose 0.3% from December and 4.1% year-over-year, marking the largest monthly gain since October 2023. Both the 20-city and 10-city indexes also hit new all-time highs. The 20-city index increased by 0.5% from December and 4.7% annually. The 10-city index also rose 0.5% month-over-month and 5.4% year-over-year. All three indexes experienced their largest annual gain since August. This is due to elevated mortgage rates and high home prices creating affordability challenges, which ultimately resulted in decreased market activity in the back half of 2024.

The home price index could impact the Shares Residential and Multisector Real Estate ETF (REZ).

Market Reactions

The S&P 500 fell 1.5% from the previous week, marking its fifth weekly loss in the past six weeks. As a result, the SPDR S&P 500 ETF Trust (SPY) fell 1.5% last week. Meanwhile, the S&P Equal Weight Index was down 0.7% from the previous week, and the Invesco S&P 500® Equal Weight ETF (RSP) fell 1.2%.

The 10-year Treasury yield finished the week at 4.27%, while the two-year note finished at 3.89%.

Market expectations for rate cuts have shifted. The CME FedWatch Tool shows three 25 basis point cuts for 2025 coming at the June, July, and October meetings, with two additional 25 basis point cuts expected in 2026.

Economic Data in the Week Ahead

The labor market takes center stage this week, with the highly anticipated March jobs report as the marquee event on Friday. This report, alongside the JOLTS release and ADP's private payroll data, will provide critical insights into the labor market’s health. Additionally, S&P Global and the Institute for Supply Management will release March's Manufacturing and Services PMI readings, offering a glimpse into the economic activity of both sectors.

For more news, information, and strategy, visit the Innovative ETFs Channel.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Read more commentaries by VettaFi