SpaceX’s blockbuster bond sale is weakening so quickly in the secondary market that traders say they can’t recall another recent deal that widened this sharply.

SpaceX is seeking to raise between $20 billion and $25 billion from a debut bond offering on Tuesday, after attracting about $30 billion of investor orders even before the sales process had formally begun, according to people with knowledge of the matter. At that size, the deal would rank among the biggest of the year, according to Bloomberg-compiled data.

Credit heavyweights like DoubleLine Capital LP and Oaktree Capital Management are buying debt now that can perform well if the artificial intelligence boom turns into a credit bust.

A private credit fund jointly managed by Future Standard and KKR & Co. sold $900 million of junk bonds on Monday, according to people familiar with the matter, in a rare high-yield offering by a publicly traded credit fund.

Meta Platforms Inc. is looking to sell between $20 billion and $25 billion of investment-grade bonds, according to people with knowledge of the transaction, as the Facebook parent boosts spending on infrastructure for the artificial intelligence boom.

Selling pressure for leveraged buyout loans has been high all year, amid fears that artificial intelligence will damage or even bankrupt the software companies that account for a fair chunk of the market.

Wall Street is gearing up to lend massive amounts of money to the biggest players in artificial intelligence — and simultaneously trying to figure out how to protect itself from any bubble that its financing may be helping to inflate.

Global bond sales have soared to a record this year as borrowers take advantage of easy market conditions to fund everything from the boom in artificial intelligence projects to a revival in acquisitions.

Meta Platforms Inc. found record-shattering demand for its bond sale on Thursday even as its shares plunged, in a sign that bond investors are looking past any concerns about its artificial-intelligence spending plans.

Credit traders are increasingly relying on algorithms, decades after they began dominating equity markets, and they have become reliable stand-ins when activity would normally sag. The result has been smoother markets with less volatility and lower trading costs.

Bond investors are accepting the smallest compensation in years in return for taking default risk, as a potent combination of economic optimism and too much cash chasing too few securities skews costs.

A long-feared change to Wall Street’s plumbing is paying off — and it’s freeing up billions.

The best performing US blue-chip bond funds of 2024 are sticking to their winning playbook: investing in debt from riskier blue-chip companies, as well as firms that can handle economic turbulence — and avoiding corporations sensitive to interest-rate risk.

Investors are piling into US leveraged loan ETFs, betting that President-elect Donald Trump’s policies will potentially boost inflation and push the Federal Reserve to keep interest rates higher for longer.

Vanguard Group Inc. sees more opportunities in the lowest rung of investment-grade bonds, even as spreads for triple-B notes reached their tightest since 1998 last week.

Wall Street banks are expected to launch a barrage of bond sales as soon as next week, capitalizing on ultra-low credit spreads and strong demand from investors after they report quarterly results.

US investment-grade corporate bond spreads have narrowed to the lowest level in more than three years, a clear sign of just how bullish credit investors are even as macro and geopolitical risks mount.

Companies and governments around the globe spent the past month streaming into debt markets, seizing on declining interest rates ahead of an uncertain US presidential election that many fear will spur volatility in markets.

The Federal Reserve’s looming rate cuts are fueling a rally in the riskiest corner of the US corporate bond market, but some investors are concerned the party may not last.

Goldman Sachs Group Inc. and Wells Fargo & Co. joined rival JPMorgan Chase & Co. in the tapping the US investment-grade market after reporting second-quarter earnings.

Goldman Sachs Group Inc. and Wells Fargo & Co. are joining rival JPMorgan Chase & Co. in the tapping the US investment-grade bond market after reporting second-quarter earnings.

Money managers including Invesco Ltd. and Loop Capital Asset Management are bullish on regional-bank bonds, wagering that the debt will perform better than the broader market as fears about funding costs settle down.

The six biggest Wall Street banks are expected to slash their corporate bond issuance in 2023 for a second year in a row, offering a bright spot for investors nursing record losses from the debt last year.

Global bonds rebounded in November, adding a record $2.8 trillion in market value, as investors bet that central banks are getting a grip on inflation. But how long the party lasts is another matter.

Banks could be about to deluge the market with more bonds after they post quarterly results, borrowing at a breakneck pace even as other blue-chip companies pull back, and bondholders could suffer in the process.

Tesla Inc., whose status as a stock-market darling has turned it into the world’s most valuable car company, may soon win over some of Wall Street’s slowest moving skeptics: Bond-rating analysts.

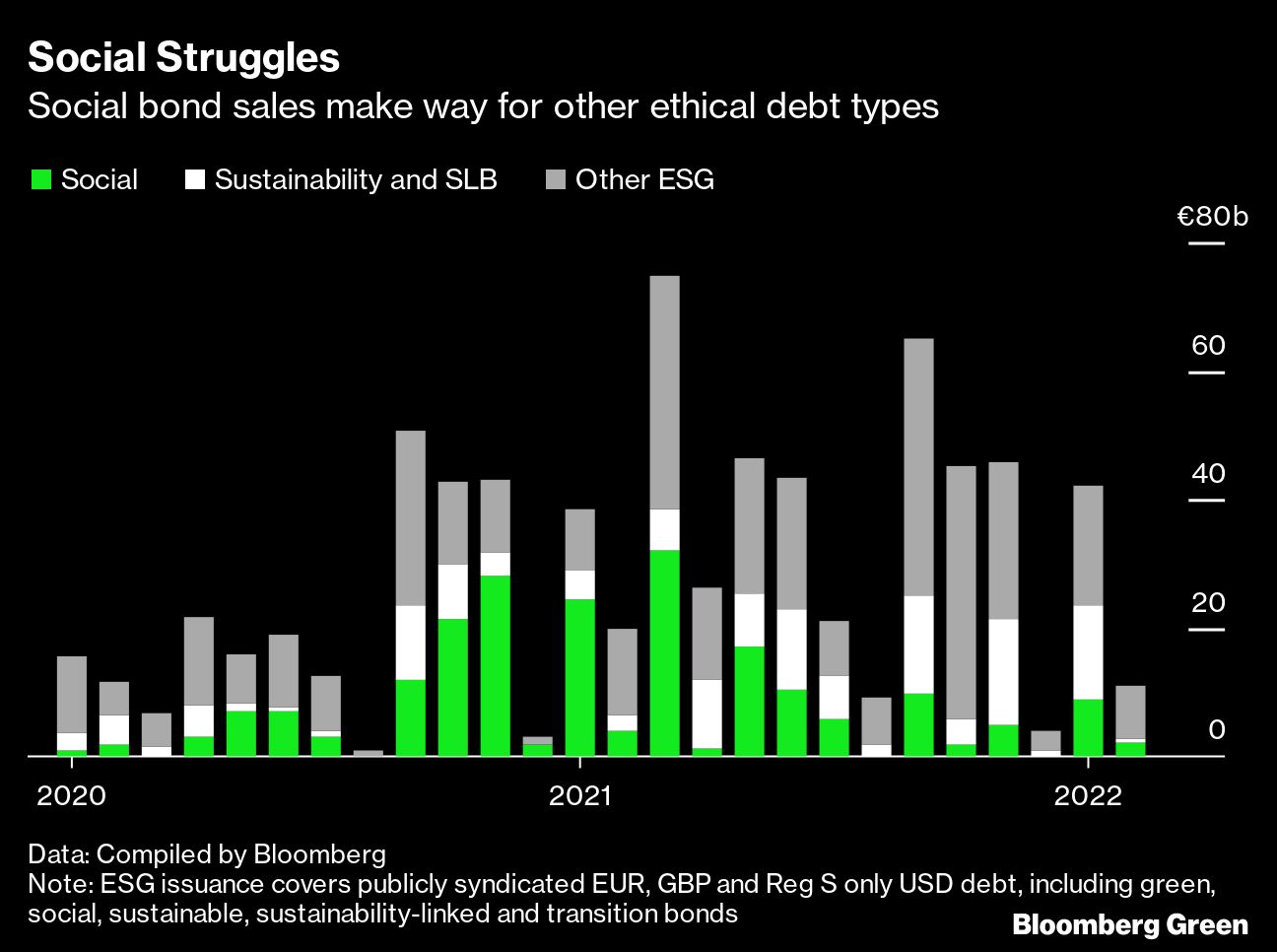

Governments that had propped up Covid-ravaged economies by issuing social bonds are now turning their attention to longer-term climate goals, while companies are keen for increased flexibility when spending proceeds from sales of environmental, social and governance (ESG) debt. That’s crimping the flow of social notes that typically fund specific projects such as job creation or affordable housing.

For all the money that companies and governments are raising in the green-bond market to fund environmental projects globally, there’s still a long way to go to adequately fund the fight against climate change, according to the Climate Bonds Initiative.

Demand is so strong for green bonds, or debt that funds environmentally friendly projects, that investors are accepting lower yields for securities that are harder to trade, according to Barclays Plc.

Global issuance of bonds for environmental, social and governance goals look set to hit $1 trillion for the first time ever this year. That’s more than double what was sold in all of 2020 as more borrowers are pushed to sell ethical debt by investors.

U.S. President Joe Biden’s pension bailout might do more than just support troubled retirement plans. It could also spur tens of billions of dollars in demand for corporate bonds with the lowest investment-grade ratings, according to Citigroup Inc.

The Bloomberg Barclays U.S. Green Bond Index is down 2.5% so far this year -- far less than the 5.1% drop seen in the investment-grade, corporate debt benchmark.

The latest crash in oil prices is threatening to push $140 billion of investment-grade energy debt over the edge into junk.