Investors have been obsessed with when the Fed will cut and how many rate cuts there will be this year and over the entire cycle.

In this PIMCO Perspectives, we examine how the return of elevated bond yields comes at an opportune time to consider shifting out of cash.

Hong Kong's prospects are closely linked to the outlook for China.

A recap of the important drivers, along with our views on how things will play out over the rest of the year.

Stocks, bonds, currencies and commodities have made significant moves in the past few months. Find out what factors to consider when deploying or redeploying capital from Franklin Templeton Institute’s Stephen Dover.

We think the intersection of hope and fear offers opportunity across asset classes and market segments. Tapping into it, however, requires in-depth research and a discerning eye. Waiting for a clarion bell to ring before deploying capital might leave investors a step behind.

Over the last five years, financial markets grappled with two generational upheavals—the Covid pandemic and the subsequent inflation surge post the Russia-Ukraine conflict.

Rather than wait for interest rate cuts, some companies are opting to simply offload debt, which could be a boon for corporate bonds.

The tendency of high earners to spend their money rather than looking to build up their net worth is known as the wealth paradox.

Investors often forget that nothing in the financial markets is permanent. Regardless of the hype or castigation, what’s hot eventually becomes cold and what’s cold eventually becomes hot. While we remain very skeptical of today’s market’s heroes, we think the range of investment opportunities is historically broad, historically attractive, and a once-in-a-generation opportunity.

At the Berkshire Hathaway Annual Meeting we marked what we believe is the end of an era both for Berkshire and for the S&P 500 Index.

It seems that every few years, the term “stagflation” gets floated around to describe the current and/or prospective U.S. macro landscape.

So much happened in the spring of 2020 that it’s easy to forget we were on track for a recession just before COVID hit. QI Research founder Danielle DiMartino Booth mentioned this during her presentation with Lacy Hunt at our Strategic Investment Conference.

It can be easy to overthink the markets and it is human nature to try to out-guess, out-maneuver, or out-smart the average, but perhaps we can step back and simplify what seems to be occurring.

Shifting dynamics among global economies and markets present a range of opportunities for multi-asset portfolios.

Are the Next Top 10 best performing S&P 500 stocks in 2023 good investments now in 2024?

Franklin Templeton Fixed Income CIO Sonal Desai discusses why persistently loose fiscal policy, relentless price pressures and resilient economic growth may cause a problem for the US Federal Reserve—and explains the implications for bond yields.

VettaFi looks at the expected growth in US LNG export capacity and how midstream/MLPs benefit.

The TCW Group announced that two of its mutual funds have been converted into ETFs, offering focuses on growth and artificial intelligence.

As of last week, the total return of the S&P 500 was even with 3-month Treasury bill returns since the valuation peak of January 2022, more than two years ago. In our view, investors continue to “grasp at the suds of yesterday’s bubble,” ignoring extreme valuations, lopsided bullish sentiment, emerging pressure on profit margins, economic conditions at the border of recession...

Over the last two weeks, the bullish sentiment index has reversed from extreme greed to fear. The composite net bullish sentiment index, comprised of professional and retail investors, fell from 38.15 to 9.9 in two weeks.

Europe's mild recession is over, with growth expected to continue. Valuations for eurozone stocks remain attractive, offering the potential for further price appreciation.

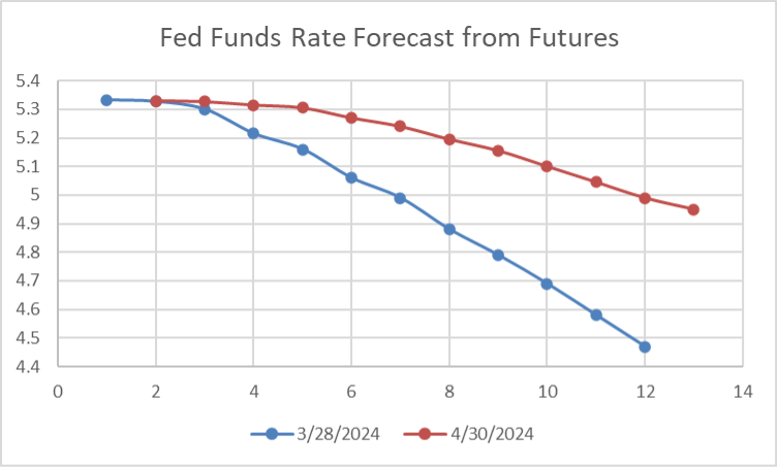

From the end of March until the end of April, the market had a serious rethink about the path of monetary policy for the rest of 2024.

Are the top 10 best performing S&P 500 stocks in 2023 good investments now in 2024?

If the financial markets have a religion, we think we know what it is: a deep and abiding faith in the ability of an omniscient Federal Reserve to ride to the rescue if and when the economic weather turns bad.

The FOMC has enough factors to consider without adding politics to the mix.

An AI bubble may be simmering in the background, so for investors still looking for AI ETFs, it may be worth taking a discerning look around.

While much remains uncertain regarding rates, inflation, and the economy, quality stock investing proves a boon in any market environment.

Bonds investors now balance the potential risks and rewards of taking on longer duration exposures in the current environment.

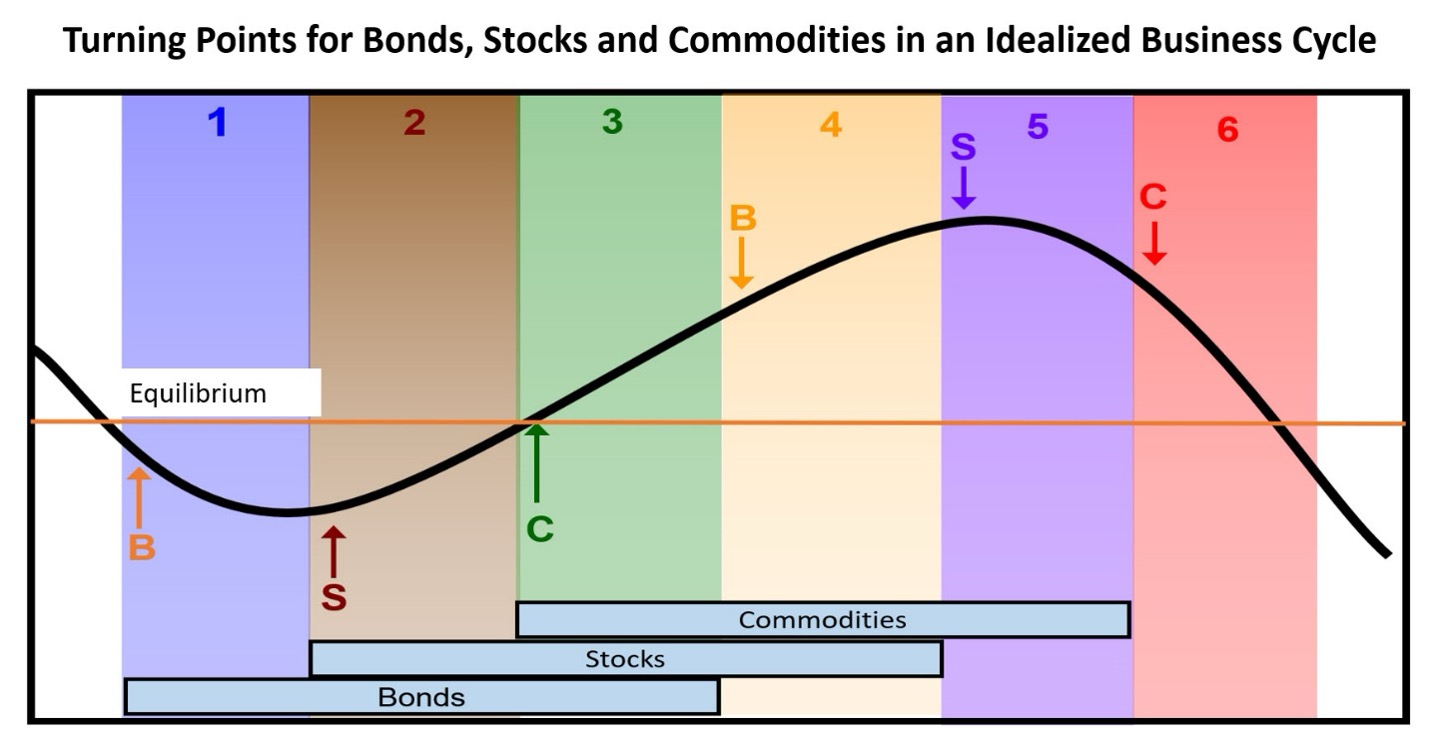

The article explores why the Federal Reserve might face pressure to raise interest rates rather than lower them in 2024, contrary to conventional expectations. It delves into the current phase of the business cycle, particularly focusing on the bullish trend for commodities and its implications for inflation.

The markets rightly experienced a significant relief last week. Stay up to date on last week’s Fed meeting with the latest commentary from Professor Siegel.

Despite the reacceleration of inflation and enduring labor market strength, the Fed remains focused on downside risks.

If you’re not sure what direct indexing means, you’re not alone. Even after the recent growth, direct indexing remains relatively unknown. As our compliance team never fails to remind us, you can’t invest directly in an index. So what exactly is direct indexing?

The stronger U.S. dollar is benefiting America, but creating troubles in other geographies.

Recent media coverage about how best to construct and manage portfolios has many wondering whether institutional investors are facing a paradigm shift right now.

Although there were no huge surprises coming out of the recent Fed meeting, it may have provided hints on what the FOMC is thinking about future monetary policy changes. Franklin Templeton Institute analyzes the Fed’s statement and press conference.

We try not to react to just one data point because, as we have always said, “a data point doesn’t a trend make.” Furthermore, we don’t know if this is just a one-time event or if it is the start of something more.

Among all economic indicators, some of the most closely watched are those surrounding the labor market. They provide insight into the health of the economy. But they also impact individuals’ lives and play a central role in government policy decisions.

Behavioral traits and cognitive biases are anathemas to portfolio management as they impair our ability to remain emotionally disconnected from our money. As history all too clearly shows, investors always do the “opposite” of what they should when it comes to investing their own money.

Among the 11 global industry classification standard (GICS) sectors, tech is not the best performer since the start of 2024. Not even close, nor is it the worst offender. Technology remains the largest sector exposure in a variety of domestic equity benchmarks. That cements its status as a must-watch group.

How momentum and election cycles may shift the impact and timing of seasonal trends.

There are attractive investment opportunities in private credit against a backdrop of a U.S. economy that continues to outpace the eurozone and the U.K.

With continued economic growth and elevated inflation levels, the Fed keeps delaying interest-rate cuts. The Franklin Templeton Investment Solutions team provides a historical analysis to make sense of the Fed rate cycle and what it implies for multi-asset investors.

As non-profit investors set their investment and spending policies, it is important to consider their organizational circumstances during a market shock.

I’m entering my annual post-SIC decompression period. I say that only half-jokingly. The last two weeks were my version of a dive deep into the sea, where you see shocking things and endure crushing pressure. The weeks of preparation are fun, but the sheer volume of information creates its own kind of pressure. You don’t just shift back into normal life after that.

We saw a dovish slant to Powell’s remarks at yesterday’s press conference, with no rate hikes in sight.

The current macroenvironment could spell opportunity for active bond funds as bond yields may have peaked.

We’ve just come through the first quarter of 2024 – and what a quarter it was! Hard on the heels of a robust end to 2023, the S&P 500 Index rose 11% in the first quarter of this year. This is the first time since 2012 that it’s had back-to-back double-digit quarterly returns.

While S&P 500 index-based ETFs were down 4% in April, they remained positive for the year. We believe as more institutional and retail investors turn to ETFs, these products will further swell in size.

I had the opportunity this week to speak at the London AIM Summit, where presenters and attendees were cautiously optimistic about the economy.